Chapter 6 Tree-based Methods

The final topic in this section of the course is tree-based methods, i.e. decision trees10 and their extensions. We will cover classification and regression trees, random forests, and gradient boosted trees. Although chapter 8 of James et al. (2013) contains a concise summary of these methods, the interested reader is rather referred to section 9.2 of Hastie et al. (2009) for trees and chapter 15 for random forests, and section 16.4 of Murphy (2013) for boosting.

Classification and regression trees – often abbreviated as CART or just referred to as decision trees collectively – are simple, non-parametric classification/regression methods that utilise a tree structure to model the relationships among the features and the potential outcomes. Although decision trees are conceptually very simple, they can be quite powerful, especially when ensembled. They are built using a heuristic called recursive binary partitioning (divide and conquer) that partitions the feature space into a set of (hyper) rectangles. The prediction following the partitioning depends on whether the response is quantitative on qualitative, hence we will again consider regression and classification problems separately, starting with the former.

6.1 Regression trees

Let \(Y\) denote a continuous outcome variable and let \(X_1, X_2, \ldots, X_p\) be a set of predictors/features, of which we have \(n\) observations. The regression tree algorithm entails repeatedly splitting the p-dimensional feature space into distinct, non-overlapping regions, with the splits orthogonal to the axes.

Suppose that we partition the feature space into \(M\) regions, \(R_1 , R_2, \ldots, R_M\). Then for each region we model the response as a constant, \(c_m\):

\[\begin{equation} f(\boldsymbol{x}) = \sum_{m=1}^Mc_mI(\boldsymbol{x} \in R_m). \tag{6.1} \end{equation}\]As with other regression models, our goal is still to minimise

\[\begin{equation} RSS = \sum_{m=1}^{M}\sum_{i:x_i\in R_m}\left[y_i - \hat{f}(\boldsymbol{x} _i)\right]^2. \tag{6.2} \end{equation}\]Therefore, the best \(\hat{c}_m\) to minimise this criterion is simply the average of the \(y_i\) in each region \(R_j\):

\[\begin{equation} \hat{c}_m = \text{ave}(y_i|\boldsymbol{x}_i \in R_m) \tag{6.3} \end{equation}\]Exhaustively searching over every possible combination of regions is computationally infeasible. Therefore, we use a top-down, greedy algorithm called recursive binary splitting:

First, select the predictor \(X_j\) and split point \(s\) such that the regions \(R_1(j, s) = \{X|X_j < s\}\) and \(R_2(j, s) = \{X|X_j \geq s\}\) lead to the greatest possible reduction in RSS. That is, we consider all predictors \(X_1, \ldots, X_p\), and all possible values of the split point \(s\) for each of the predictors, and then choose the predictor and split point such that Equation (6.2) is minimised.

Next, identify the predictor and split point that best splits one of the previously identified regions, such that there are now three regions.

Continue splitting the regions until a stopping criterion is reached. For instance, we may continue until no region contains more than 5 observations, or when the proportional reduction in \(RSS\) is less than some threshold.

Once the regions \(R_1 , R_2, \ldots, R_M\) have been created, we predict the response for a given test observation using the mean of the training observations in the region to which that test observation belongs.

As a brief side note, the model from Equation (6.1) can also be written in the form

\[f(\boldsymbol{x}) = \sum_{m=1}^Mc_mI(\boldsymbol{x} \in R_m) = \sum_{m=1}^Mc_m \phi(\boldsymbol{x}; \boldsymbol{v}_m),\] where \(\boldsymbol{v}_m\) encodes the choice of variable to split on \((X_j)\) and the split point value \((s)\) on the path from the start (root) to the \(m\)th region (leaf). When viewed as such, a CART model is just an adaptive basis function model (alluded to in the previous chapter), where the basis functions define the regions, and the weights specify the response value in each region (Murphy, 2013, p. 544).

One of the advantages of a decision tree is its visual representation which makes for easy interpretation. This is best illustrating via an example.

6.1.1 Example 6 – California housing

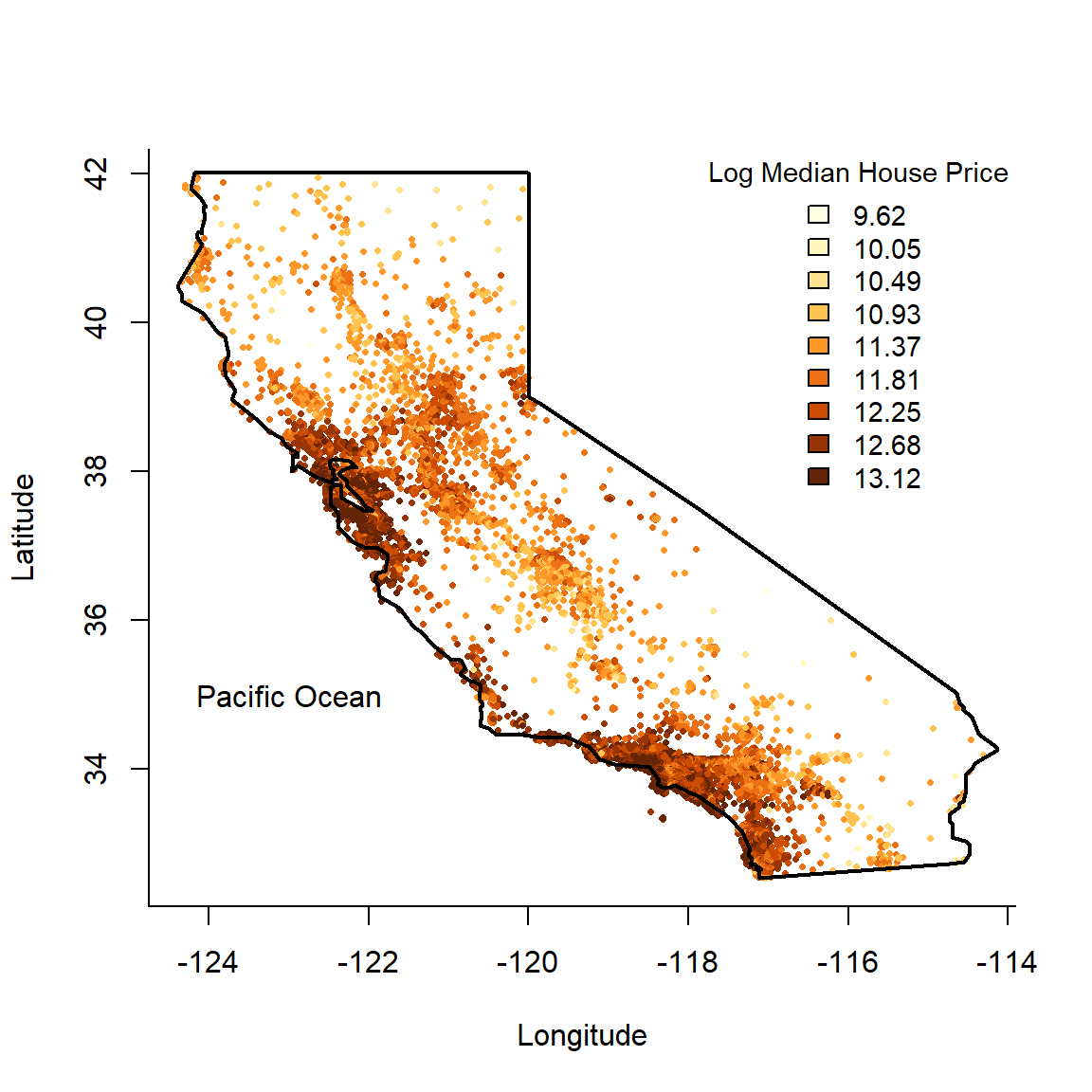

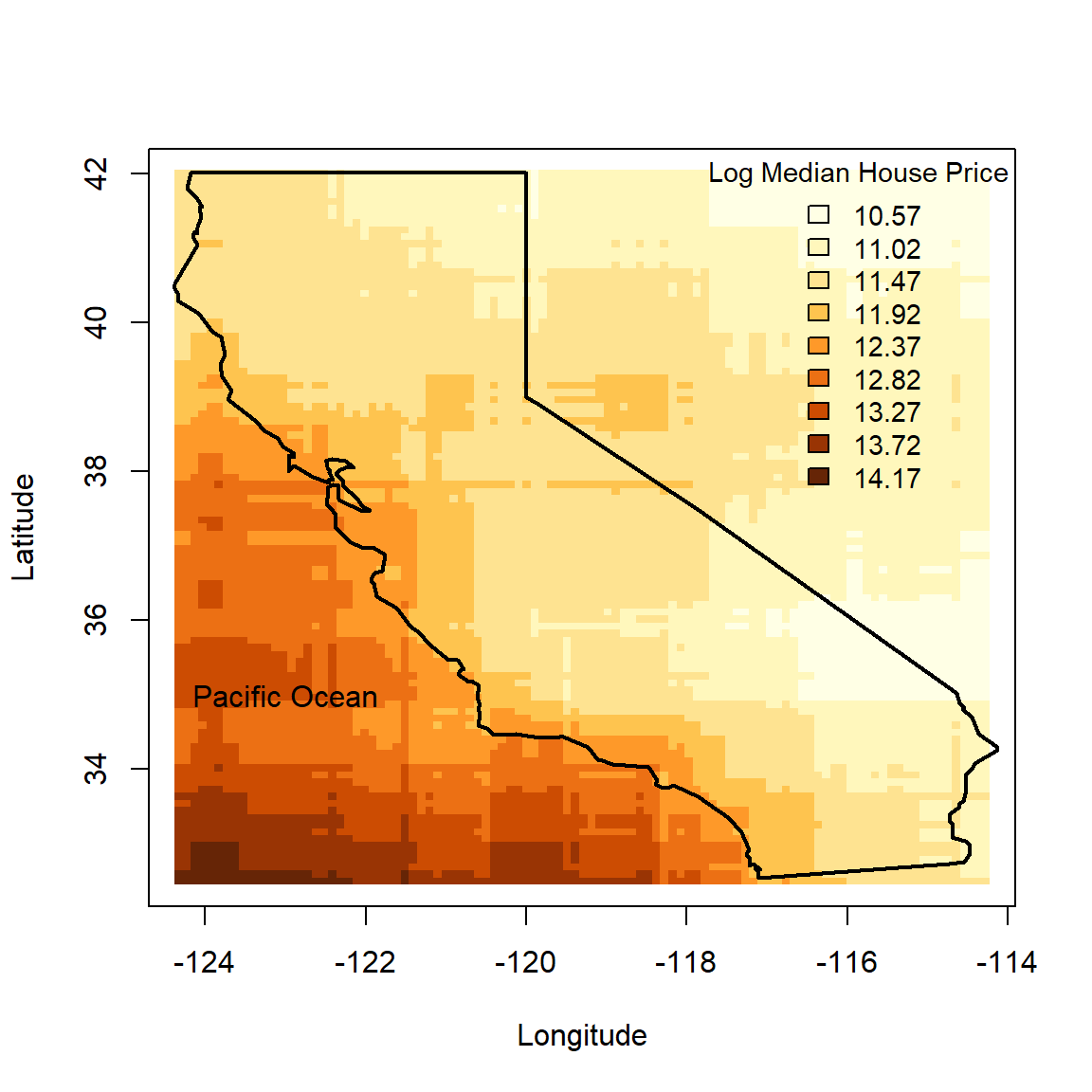

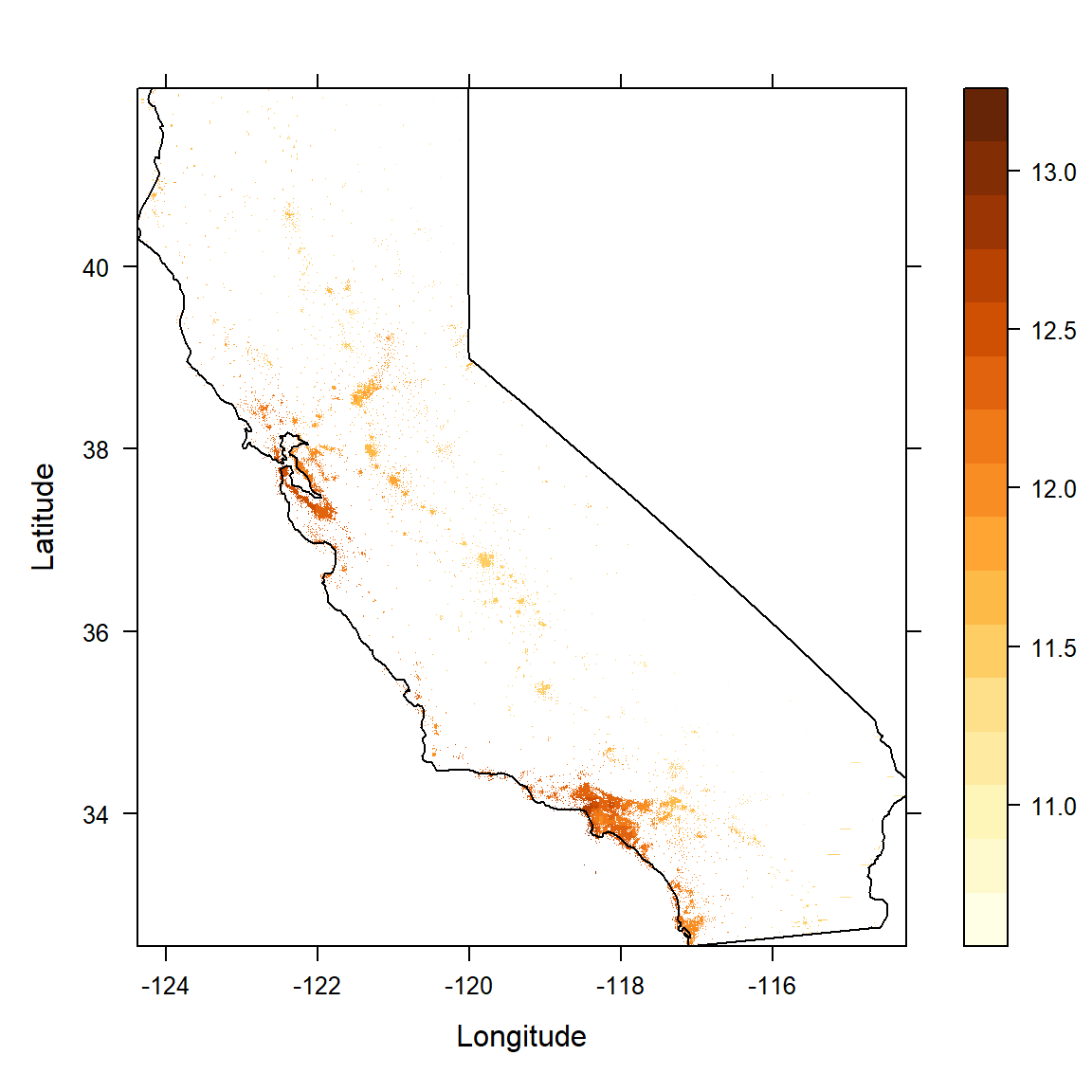

In this example we consider a well-known dataset from the 1990 California census, which contains aggregated data for 20 640 neighbourhoods. The variables include information like the neighbourhood’s median house age, the median income, total number of bedrooms and bathrooms, number of households, population, and the location, as can be seen here:

library(DT)

calif <- read.csv('data/calif.csv')

datatable(calif, options = list(scrollX = T, pageLength = 6))

For now, we will only use the spatial information (latitude and longitude) to model the target variable: (log of) median house price.

We begin by plotting a map of the data – a 2-dimensional feature space – using a colour scale to indicate the target variable.

library(maps)

library(RColorBrewer) # For colourblind friendly palettes

# Replace with log

calif$HousePrice <- log(calif$HousePrice)

# Make custom colour scale

n_breaks <- 9

my_cols <- brewer.pal(n_breaks, 'YlOrBr')[cut(calif$HousePrice, breaks = n_breaks)]

# Plot the data

plot(calif$Longitude, calif$Latitude, pch = 16, cex = 0.5, bty = 'L',

xlab = 'Longitude', ylab = 'Latitude', col = my_cols)

legend(x = 'topright', bty = 'n', title = 'Log Median House Price', cex = 0.9,

legend = round(seq(min(calif$HousePrice), max(calif$HousePrice), length.out = n_breaks), 2),

fill = brewer.pal(n_breaks, 'YlOrBr'))

# Add the state border

par(new = TRUE)

map('state', 'california', add = T, lwd = 2) |> invisible()

text(-123, 35, 'Pacific Ocean')

Figure 6.1: Californian median neighbourhood house prices (logscale) in 1990.

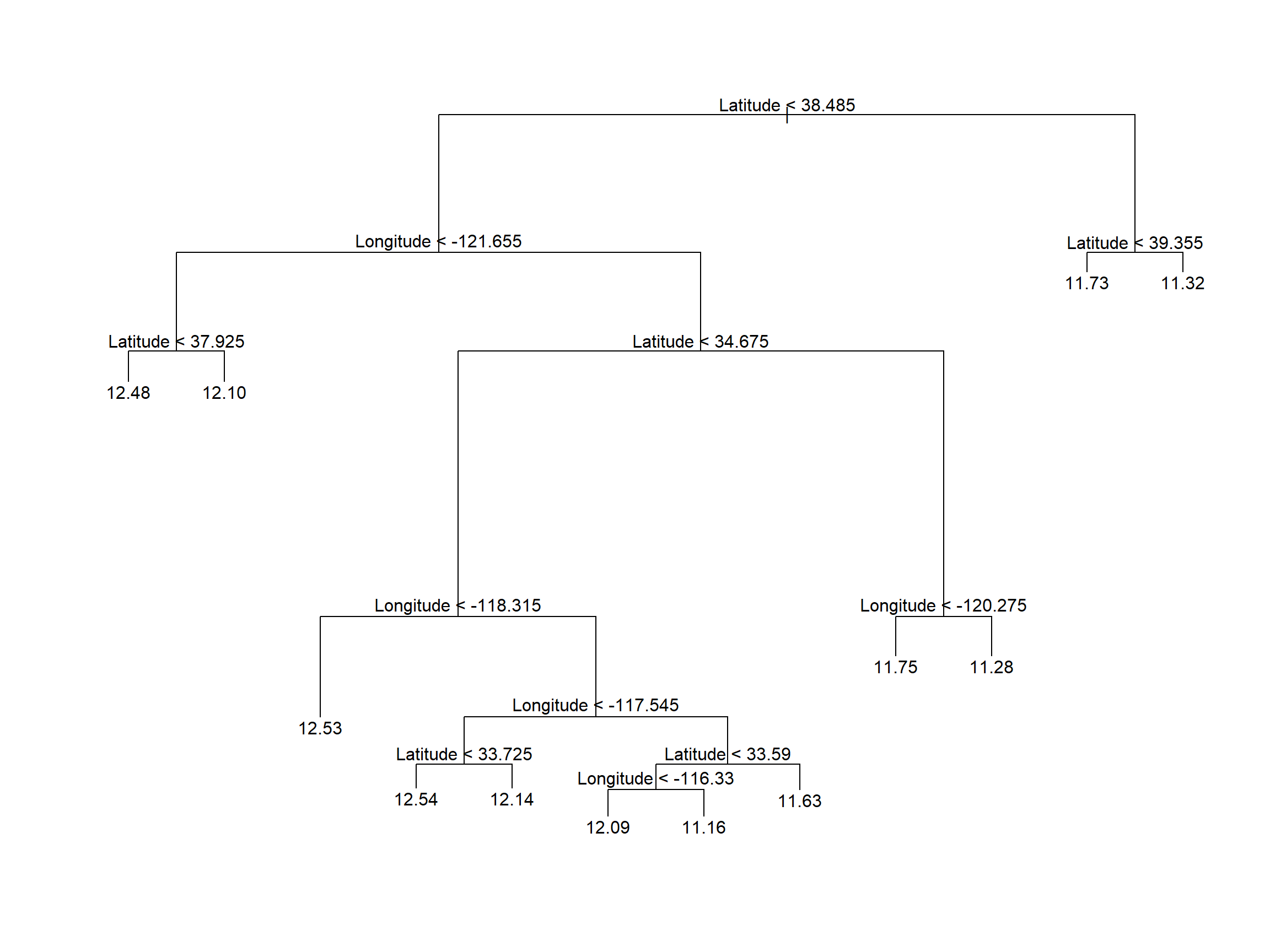

We can now proceed to partition the feature space using recursive binary splitting, resulting in a regression tree. There are many packages in R that implement decision trees. We will be using one of the more basic ones: tree. For now we are not going to split into training and testing; for illustrative purposes we shall use the entire dataset.

Using the default stopping criteria, we fit the following decision tree shown below in Figure 6.2

library(tree)

#Easy as one, two, tree

calif_tree <- tree(HousePrice ~ Latitude + Longitude, data = calif)

# Plot the tree

plot(calif_tree)

text(calif_tree)

Figure 6.2: Vanilla regression tree fitted to the Cailfornia dataset

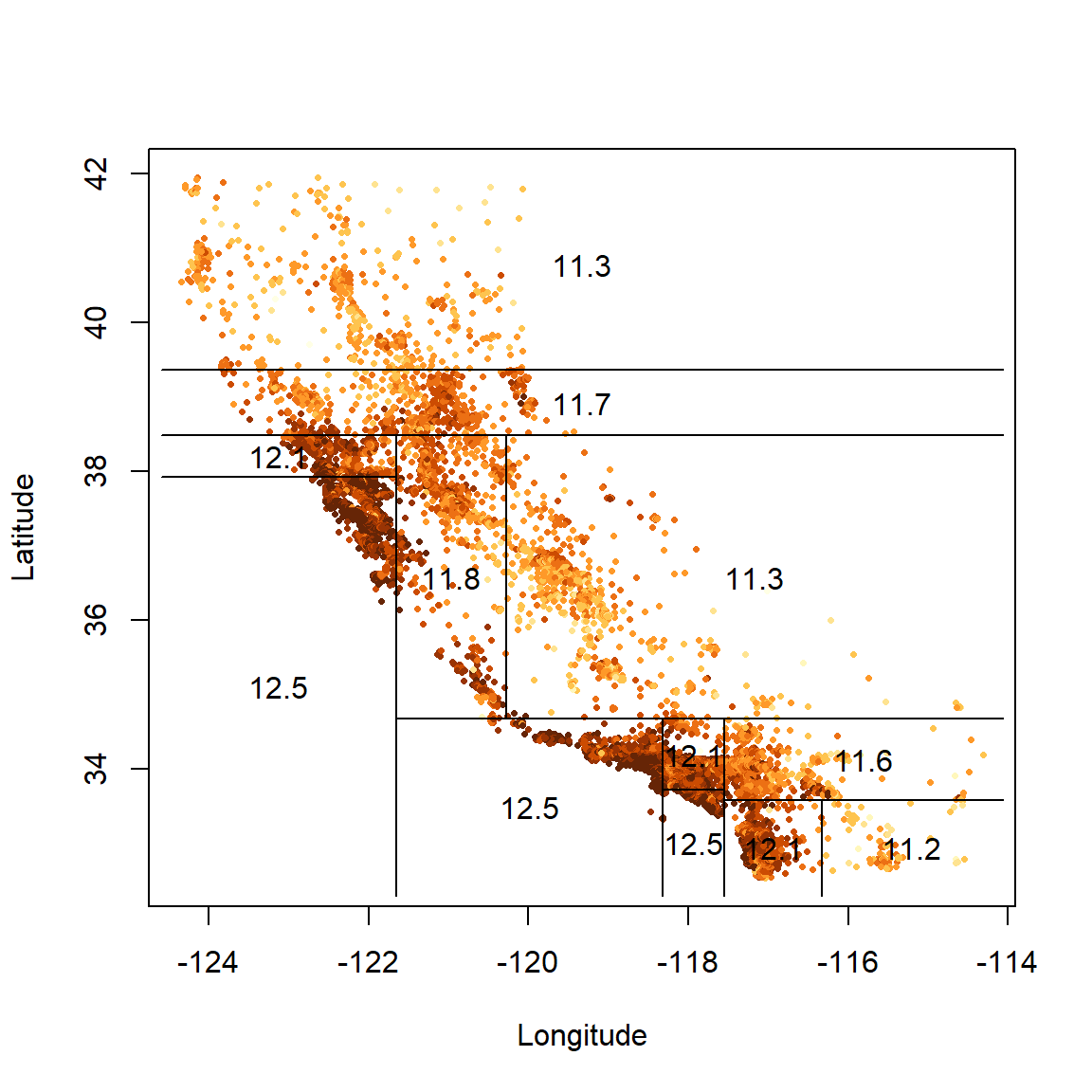

The corresponding feature space is shown below in Figure 6.3.

# Plot the data again

plot(calif$Longitude, calif$Latitude, pch = 16, cex = 0.5,

col = my_cols, xlab = 'Longitude', ylab = 'Latitude', bty = 'o')

# And add the partitioned feature space

partition.tree(calif_tree, ordvars = c('Longitude', 'Latitude'), add = T, lwd = 3)

Figure 6.3: Partitioned feature space for vanilla regression tree fitted to the Cailfornia dataset

The labels in Figure 6.2 indicate both the splitting variable and the split point. All data points below the split point for that variable go to the left of that branch or, equivalently, are left/below the resulting line in the partitioned feature space.

The final regions correspond to the ends of the tree’s branches, which are indeed referred to as leaves, or terminal nodes. The leaf values are the fitted values for all the data points in that region, which is just the average (Equation (6.3)).

It is easy to see visually that the algorithm attempts to group together pockets of most-similar observations. Again, though, the question arises of when to stop? This returns us to the same consideration we encountered in all previous models, namely that of model complexity.

6.1.2 Cost complexity pruning

A decision tree’s complexity is measured by the number of leaves (which is equal to the number of splits + 1). We could continue splitting until every single observation is in its own region, such that the training \(RSS = 0\) (each \(y_i\) will be equal to its region’s average). However, this would be extreme overfitting, and the model would perform very poorly on unseen data. As with all statistical learning algorithms, we need to determine the ideal level of complexity that captures as much information as possible without overfitting.

One way of controlling complexity is to continue growing the tree only until the decrease in RSS fails to exceed some high threshold. However, this is short-sighted since a split later on might produce an even greater reduction in RSS. A better strategy is therefore to grow a very large tree and then prune it back to obtain a smaller subtree.

Since our goal is to find the subtree with the lowest test error, we can estimate any given subtree’s test error using cross-validation. However, estimating the CV error for every possible subtree is not computationally feasible. Instead we only consider a sequence of trees obtained by pruning the full tree back in a nested manner. This tree pruning technique is known as cost complexity pruning, or weakest link pruning, and is essentially a form of regularisation.

Let \(T_0\) be the full tree and let \(T\subseteq T_0\) be a subtree with \(|T|\) terminal nodes or, equivalently, regions in the feature space. We now penalise the RSS according to \(|T|\):

\[\begin{equation} RSS_{\alpha} = \sum_{m=1}^{|T|}\sum_{i:x_i\in R_m}\left[y_i - \hat{f}(\boldsymbol{x} _i)\right]^2 + \alpha|T|, \tag{6.4} \end{equation}\]where \(\alpha \ge 0\) is a tuning parameter.

When \(\alpha = 0\), \(RSS_{\alpha} = RSS\) and therefore \(T=T_0\). For values of \(\alpha > 0\), we seek the subtree \(T\) that minimises \(RSS_{\alpha}\). As \(\alpha\) increases, subtrees with a large number of leaves are penalised more heavily and a smaller \(T\) will be favoured such that branches are “pruned” off. This happens in a nested fashion, such that we can easily obtain subtrees as a function of \(\alpha\).

By choosing \(\alpha\), we are effectively selecting a subtree; that is, a more parsimonious model that does not overfit the sample data. We want the subtree (and hence \(\alpha\) value) that has the lowest test error and therefore has the best predictive performance on unseen data. Therefore, we will once again use CV to determine this \(\alpha\)/subtree.

To illustrate this, we return to the California dataset, this time using all the predictors.

# First fit larger tree by relaxing stopping criteria

# ?tree.control

# minsize: will only consider split if at least so many observations in node

# mincut: will only split if both child nodes then have at least so many

# mindev: will only consider split if within-node deviance is at least this times root RSS

stopcrit <- tree.control(nobs = nrow(calif), mindev = 0.003)

calif_bigtree <- tree(HousePrice ~ . , data = calif, control = stopcrit)

(s <- summary(calif_bigtree))##

## Regression tree:

## tree(formula = HousePrice ~ ., data = calif, control = stopcrit)

## Variables actually used in tree construction:

## [1] "Income" "Latitude" "Longitude" "HouseAge"

## Number of terminal nodes: 25

## Residual mean deviance: 0.1162 = 2396 / 20620

## Distribution of residuals:

## Min. 1st Qu. Median Mean 3rd Qu. Max.

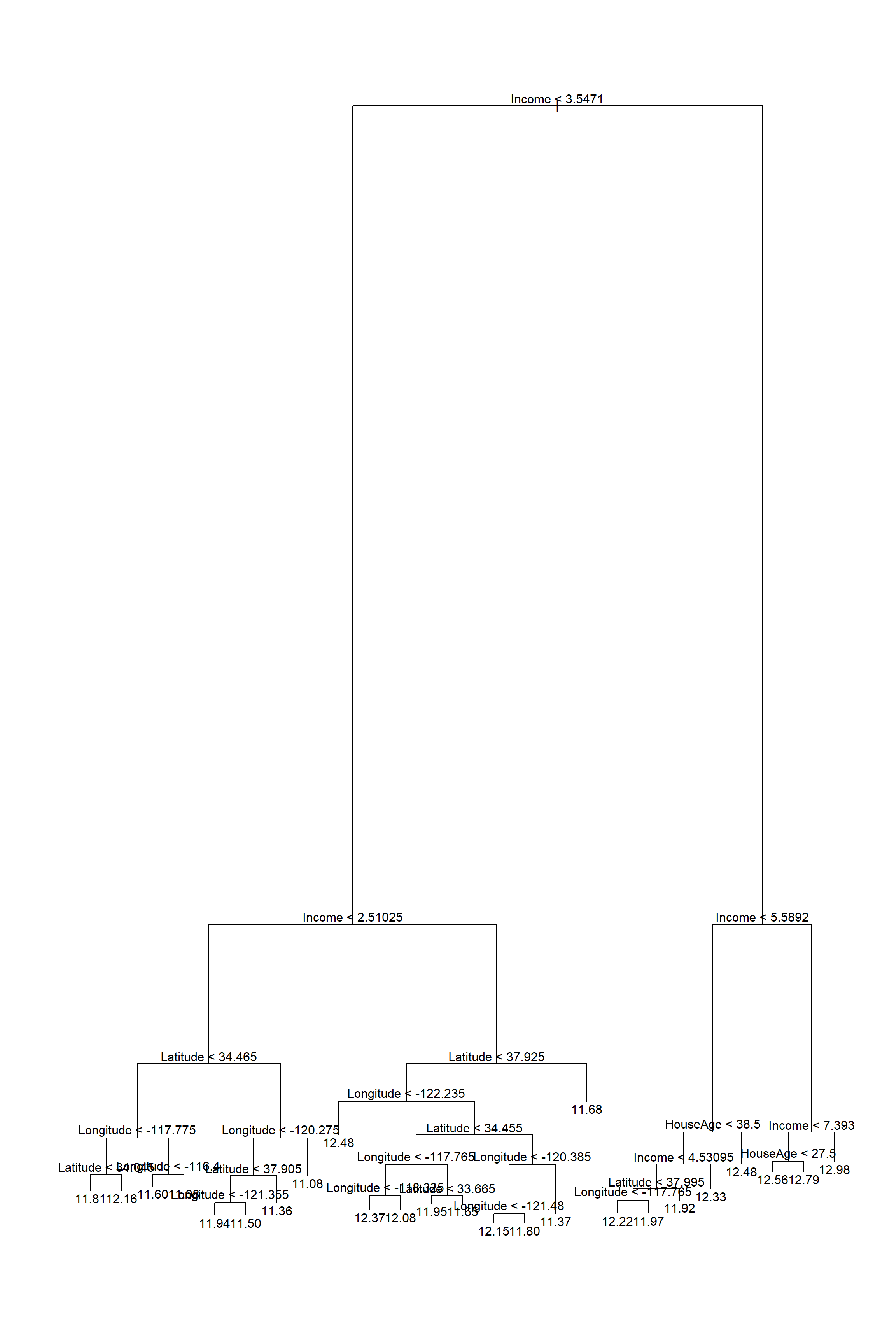

## -2.86000 -0.21050 -0.01136 0.00000 0.19030 2.03900By slightly relaxing the stopping criterion of RSS reduction, we increased the size of the tree to 25. We also see that the only features used to split were income, house age, and latitude and longitude, so the location information was indeed very useful!

Plotting the tree at this size is already quite messy (Figure 6.4), with a lot of unnecessary, indistinguishable information at the bottom.

Figure 6.4: Large regression tree fitted to the Cailfornia dataset

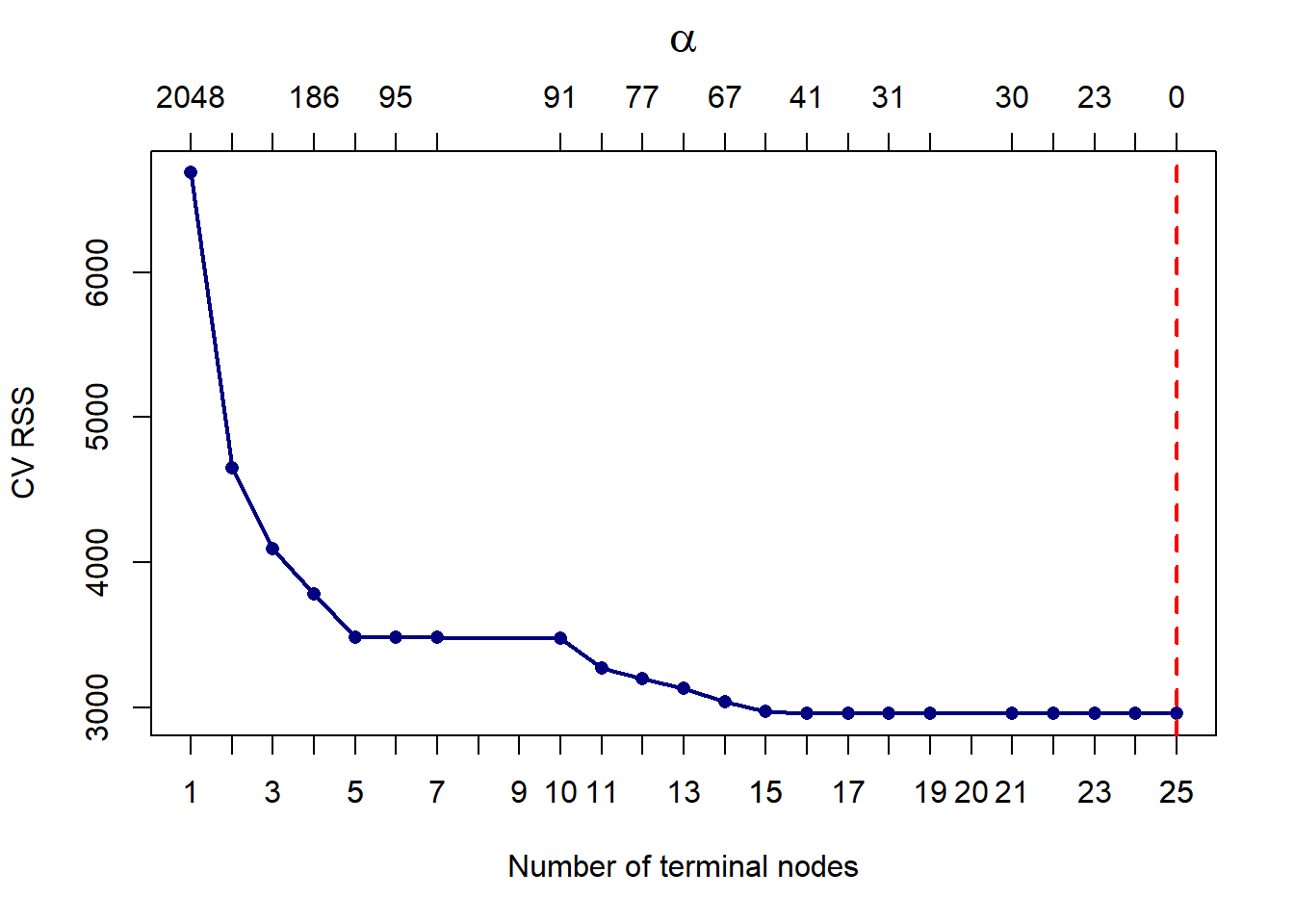

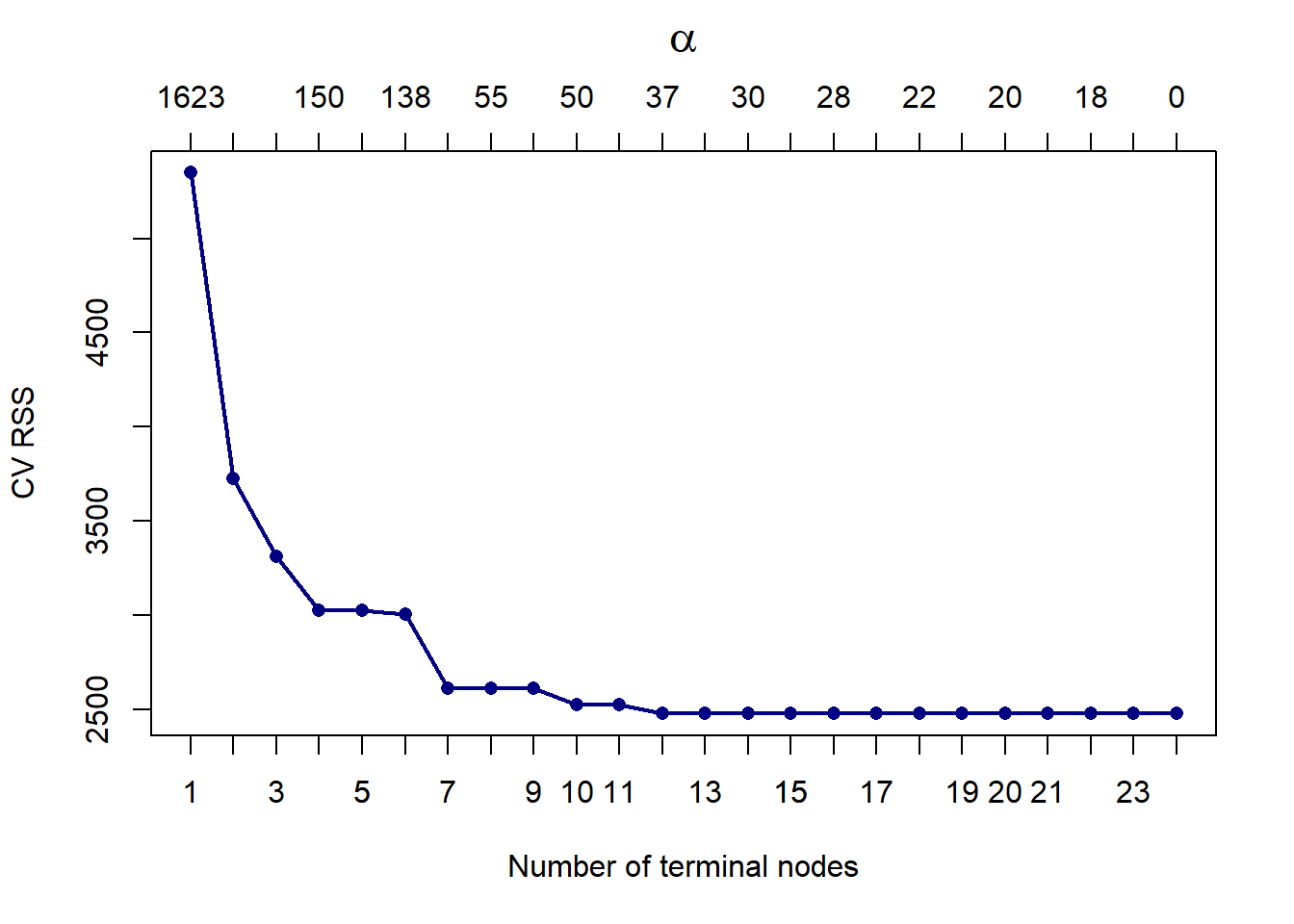

We now apply cost complexity pruning, measuring the CV RSS for each subtree.

set.seed(4026)

calif_cv <- cv.tree(calif_bigtree)

# See str(calif_cv)

# size = number of terminal nodes

# dev = RSS

# k = alpha (tuning parameter that determines tree size)

calif_cv$k[1] <- 0 #First entry was -Inf

# Plot everything

plot(calif_cv$size, calif_cv$dev, type = 'o',

pch = 16, col = 'navy', lwd = 2,

xlab = 'Number of terminal nodes', ylab = 'CV RSS')

axis(side = 1, at = 1:max(calif_cv$size), labels = 1:max(calif_cv$size))

# Add alpha values to the plot:

alpha <- round(calif_cv$k)

axis(3, at = calif_cv$size, lab = alpha)

mtext(expression(alpha), 3, line = 2.5, cex = 1.5)

# Highlight the minimum CV Error

T <- calif_cv$size[which.min(calif_cv$dev)]

abline(v = T, lty = 2, lwd = 2, col = 'red')

Figure 6.5: Cross-validated pruning results on the large tree fitted to the Cailfornia dataset

We can see that the CV error did indeed keep decreasing. To check this, we show that the minimum RSS is indeed observed at 25 terminal nodes:

## [1] 25However, the improvement in results is negligible from about 15 leaves. One could certainly also argue that a tree of size 5 might be preferable, given that it performs comparably to a tree of size 10, and the improvement from that point on is not drastic. In fact, decision trees will rarely be used for prediction purposes, since they will most often be outperformed by other algorithms. Their main value arguably lies in their interpretability, hence we will consider opting for the simpler model.

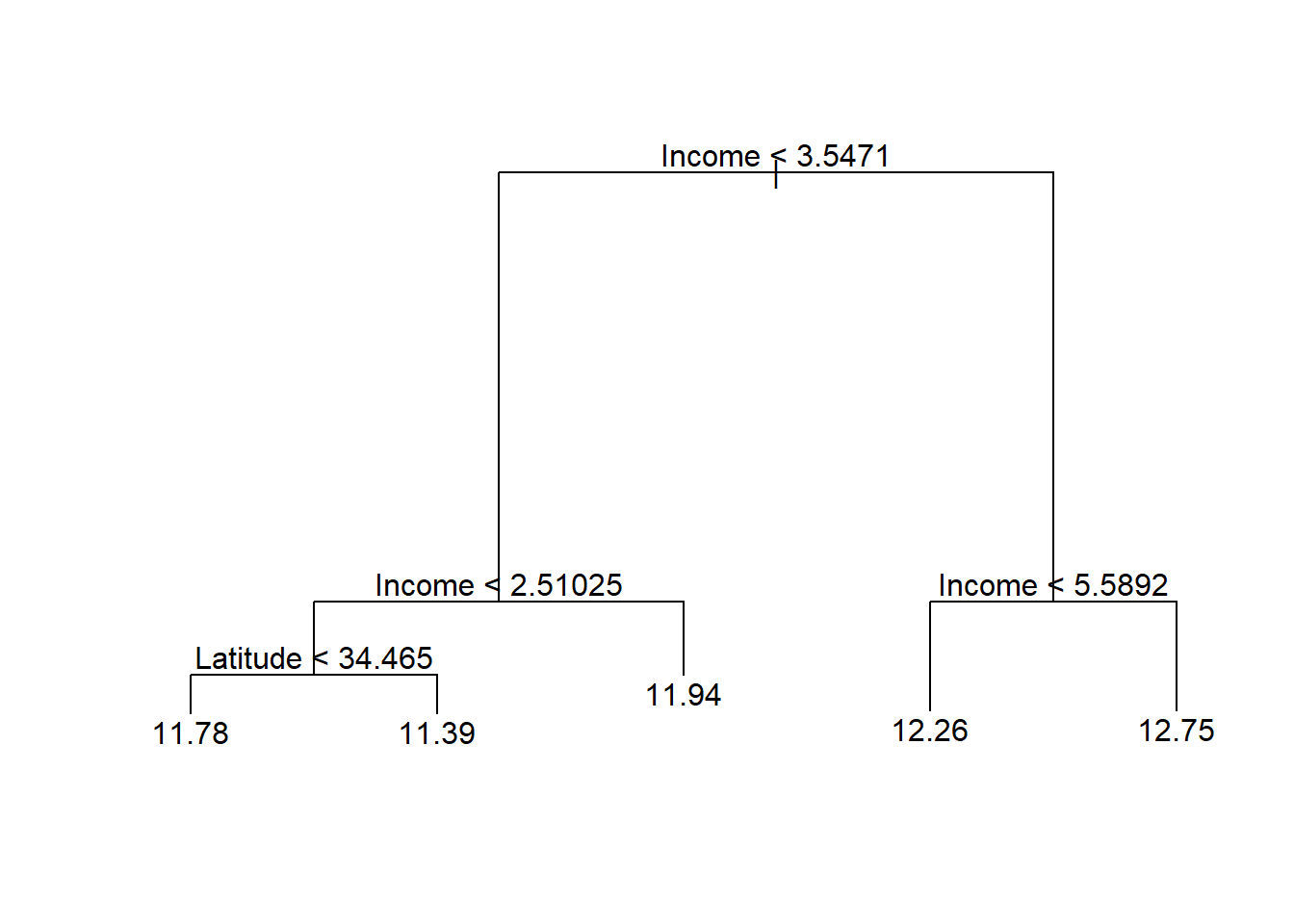

# Prune the tree

calif_pruned5 <- prune.tree(calif_bigtree, best = 5)

plot(calif_pruned5)

text(calif_pruned5)

Figure 6.6: Cailfornia housing regression tree pruned to 5 terminal nodes

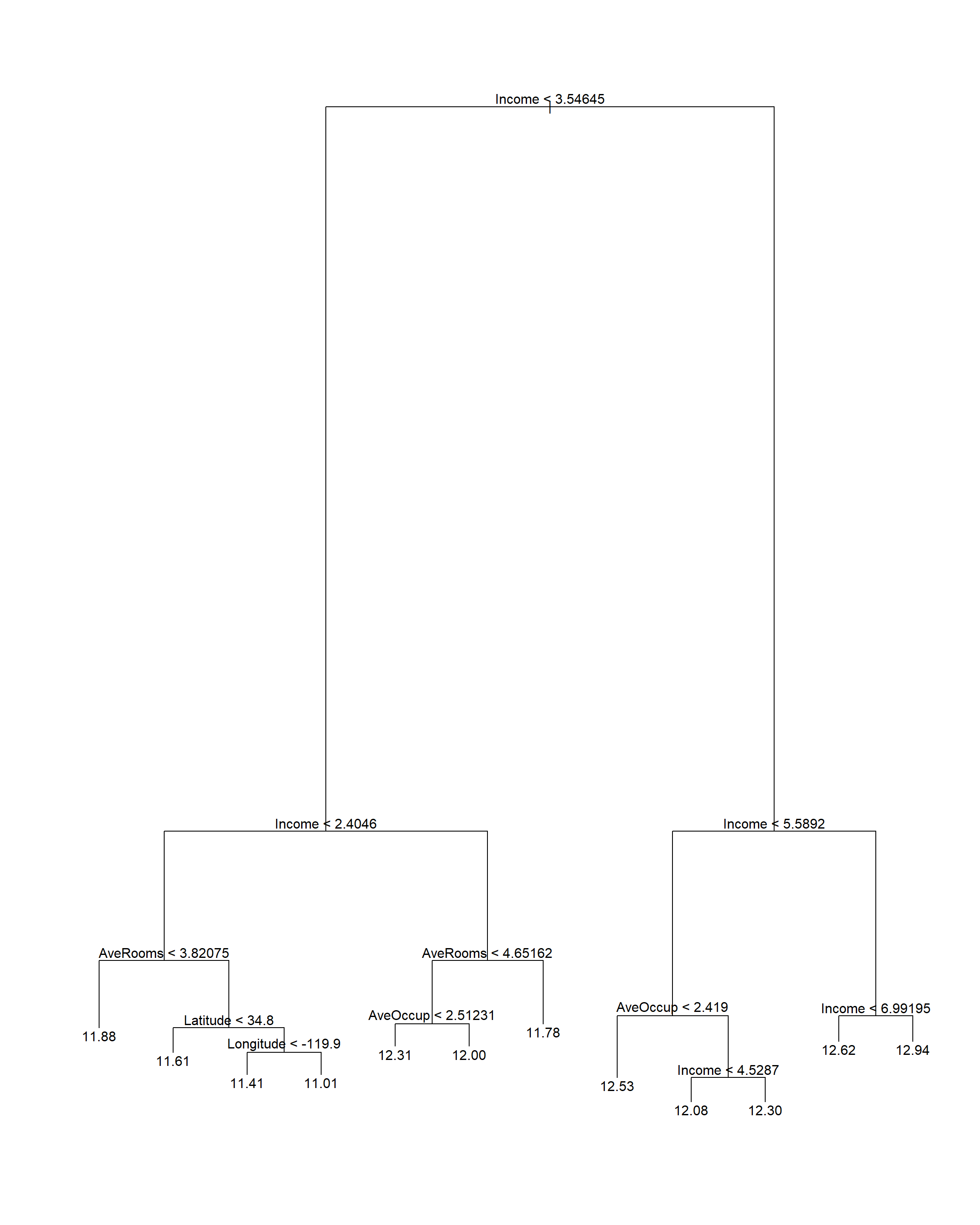

We see that this tree only uses income and latitude as splitting variables, perhaps suggesting that it is too simplistic, especially when compared to the 15-node tree. In Figure 6.7 we see that although the gain in RSS reduction is comparatively limited, the later splits make extensive use of the location information. However, for neighbourhoods with a median income above 3.547, only income and house age were used in subsequent splits, indicating less interaction between income and location in the wealthy areas.

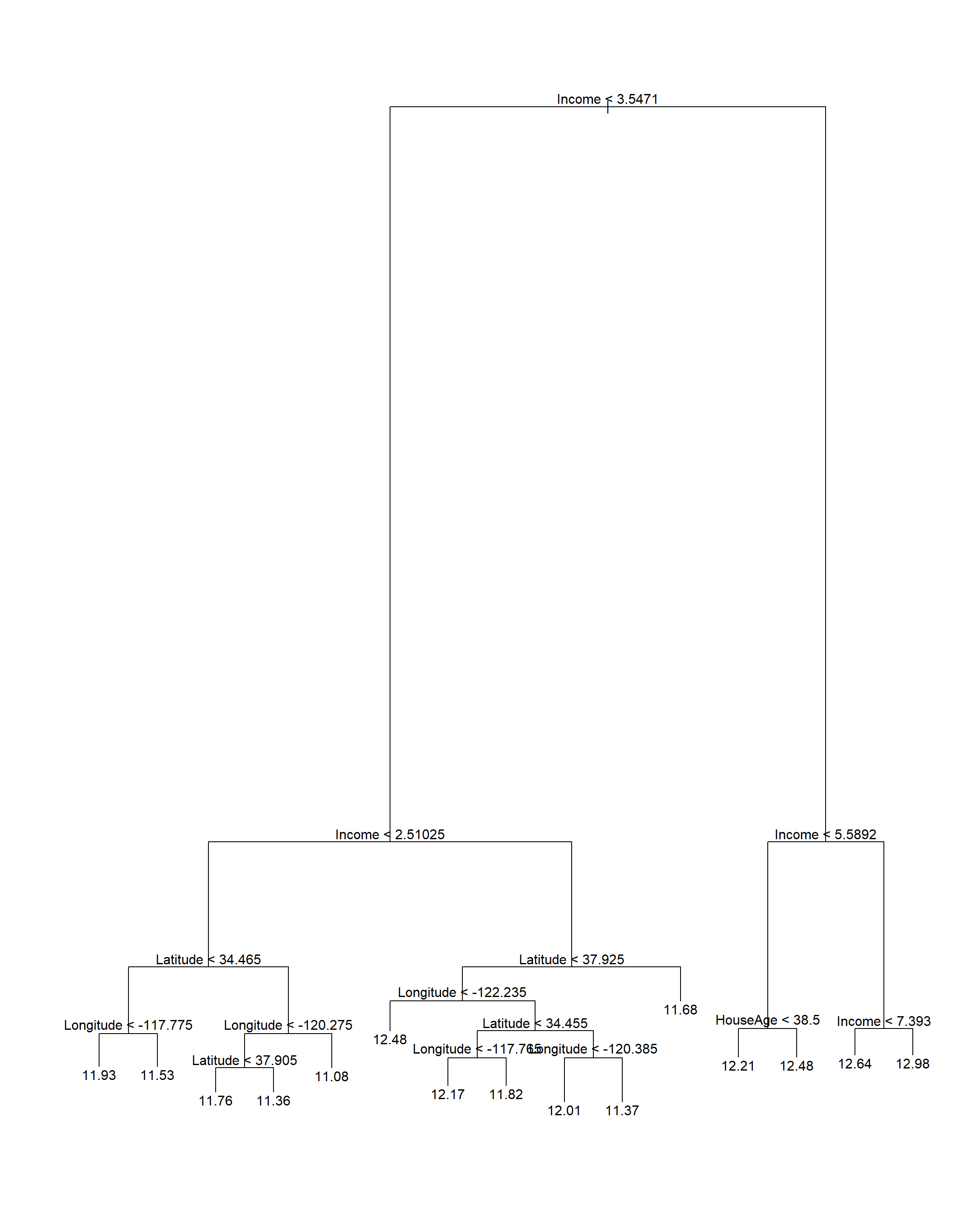

# Prune the tree

calif_pruned15 <- prune.tree(calif_bigtree, best = 15)

plot(calif_pruned15)

text(calif_pruned15)

Figure 6.7: Cailfornia housing regression tree pruned to 15 terminal nodes

This example primarily serves to illustrate the interpretive properties of decision trees. We will explore their sensitivity to sampling variation and their performance on unseen data later once ensembling methods are introduced. First, however, we will see how this method can be used to classify a qualitative response.

6.2 Classification trees

Consider now a categorical response variable \(Y \in \{1, 2, \ldots, K\}\). Just like with regression trees, classification trees split the feature space into \(M\) regions which correspond to the terminal (leaf) nodes of the tree. In lieu of an average to calculate for the observations falling within each region, the predicted value of an observation with \(X \in R_m\) will now be the most commonly occurring class in \(R_m\).

The class proportions in each terminal node provide an indication of the reliability of the prediction:

\[\begin{equation} \hat{p}_{mk} = \frac{1}{N_m} \sum_{i:x_i\in R_m} I(y_i = k), \tag{6.5} \end{equation}\]where \(N_m\) denotes the number of observations in region \(R_m\).

Although classification trees are also grown by recursive binary splitting, RSS cannot be used as splitting criterion. Now, we could grow the tree by choosing the split that minimises the classification error at each step, i.e. minimise the proportion of incorrectly predicted observations. In practice, however, splitting on the reduction in classification error does not produce good trees. We will instead consider the following three splitting criteria, all of which are designed to measure node impurity.

6.2.1 Splitting criteria

We would like the leaf nodes to be as homogeneous or “pure” as possible, with each leaf node ideally containing observations of only one response category. When deciding where to split on a particular dimension, we can use the following measurements to measure the resulting homogeneity.

1. Gini Index

Arguably the simplest way of measuring node impurity is via the Gini index (also referred to as Gini impurity or Gini’s diversity index), which is defined as follows:

\[\begin{equation} G = \sum_{m=1}^{M}\sum_{k=1}^{K} \hat{p}_{mk} (1-\hat{p}_{mk}), \tag{6.6} \end{equation}\]where \(\hat{p}_{mk}\) is the proportion of observations in response category \(k = 1, \ldots, K\) within leaf node \(m = 1, \ldots, M\). At each step during tree growth, we would therefore choose the split that produces the greatest reduction in the Gini index.

For a binary response, for example, \(G_m = 2\hat{p}_m(1 - \hat{p}_m)\). Note that the Gini index is minimised when leaf node \(m\) is homogeneous, i.e. when \(\hat{p}_m = 0\) or \(\hat{p}_m = 1\).

2. Shannon entropy

An alternative way to determine node impurity is to calculate the Shannon entropy of each terminal node, and again sum across all \(M\) leaves:

\[\begin{equation} H = -\sum_{m=1}^{M}\sum_{k=1}^{K}\hat{p}_{mk}\log(\hat{p}_{mk}). \tag{6.7} \end{equation}\]This measure, usually just referred to as entropy, stems from information theory and is equivalent to measuring information gain. Note that \(\log_2\) is also often used in the definition, depending on the context. This yields units of “bits”, whereas the natural logarithm in Equation (6.7) yields “nats”.

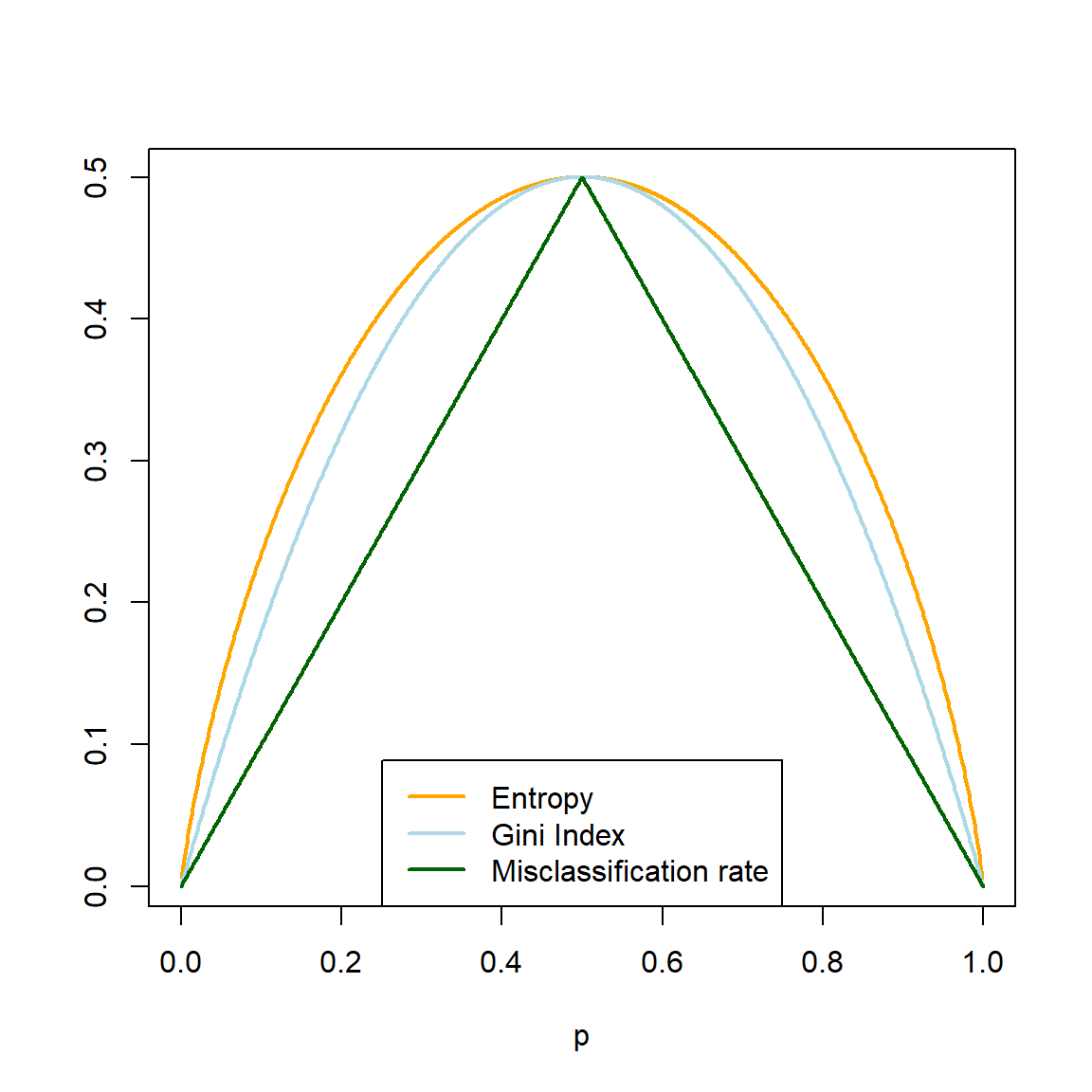

Considering again the binary case, Figure 6.8 shows the similarity between the Gini index and entropy, with the misclassification rate included for reference. Note that the entropy has been scaled to go through the point \((0.5, 0.5)\).

p <- seq(0, 1, 0.001)

Gini <- 2*p*(1-p)

Entropy <- -p*log(p) - (1-p)*log(1-p)

Entropy <- Entropy/max(na.omit(Entropy))*0.5

Misclass <- 0.5 - abs(p - 0.5)

plot(p, Entropy, 'l', lwd = 2, col = 'orange', ylab = '')

lines(p, Gini, 'l', lwd = 2, col = 'lightblue')

lines(p, Misclass, 'l', lwd = 2, col = 'darkgreen')

legend('bottom', c('Entropy', 'Gini Index', 'Misclassification rate'),

col = c('orange', 'lightblue', 'darkgreen'), lty = 1, lwd = 2)

Figure 6.8: Gini index, (scaled) entropy, and classification error as a function of node impurity for a binary response.

As seen in Figure 6.8, the Gini index and entropy are computationally similar. In fact, the tree package in R uses Gini as a possible splitting criterion, but not entropy.

There are several sources on the topic that use ambiguous and, at times, contradictory terminology to refer to Shannon entropy. For example, page 309 of Hastie et al. (2009) refers to the measurement in Equation (6.7) as “cross-entropy” or “deviance”, whilst Murphy (2013) uses the term “entropy”, but also equates it to deviance on page 547.

However, on page 221 of Hastie et al. (2009) we see that the term deviance is also used to refer to the quantity \(2 \times \text{NLL}\) (negative log-likelihood). In fact, it is the NLL that is known as cross-entropy (Bishop, 2006, p. 209). Cross-entropy11 is usually used as a measure of dissimilarity between two probability distributions, typically the predicted class probabilities and the true class probabilities, in which case this loss function is also referred to as “log loss”.

Deviance, which is proportional to NLL, therefore offers a likelihood-based approach to measuring node impurity.

3. Deviance

The deviance is constructed by viewing a classification tree as a probability model. Let \(\boldsymbol{Y}_m\), denoting the set of categorical responses in leaf node \(m\), be a random sample of size \(n_m\) from the multinomial distribution:

\[\begin{equation} p(\boldsymbol{y}_m) = \binom{n_m}{n_{m1} \cdots n_{mK} } \prod_{k=1}^{K} p_{mk}^{n_{mk}}. \tag{6.8} \end{equation}\]The likelihood over all \(M\) leaf nodes is then given by

\[\begin{equation} L = \prod_{m=1}^{M} p(\boldsymbol{y}_m) \propto \prod_{m=1}^{M} \prod_{k=1}^{K} p_{mk}^{n_{mk}}. \tag{6.9} \end{equation}\]Now, the deviance is defined as

\[\begin{equation} D = -2\log(L) = -2 \sum_{m=1}^{M} \sum_{k=1}^{K} n_{mk} \log(p_{mk}). \tag{6.10} \end{equation}\]We want the model that makes the data most probable, i.e. has the highest likelihood. This is equivalent to minimising the deviance. When we grow a classification tree, we therefore choose the split that reduces the deviance by the most at each step. Note that the deviance takes the number of observations in each terminal node into account, unlike the Gini index and entropy.

6.2.2 Link between deviance and RSS

Returning to regression trees for a moment, if we inspect the object created by the tree() function for the California housing data, we note that the RSS is actually referred to as “deviance” in the model output.

##

## Regression tree:

## tree(formula = HousePrice ~ Latitude + Longitude, data = calif)

## Number of terminal nodes: 12

## Residual mean deviance: 0.1662 = 3429 / 20630

## Distribution of residuals:

## Min. 1st Qu. Median Mean 3rd Qu. Max.

## -2.75900 -0.26080 -0.01359 0.00000 0.26310 1.84100## [1] 3428.558To make the link between the deviance of a classification tree and the RSS of a regression tree, suppose that for terminal node \(m\) the continuous response \(\boldsymbol{Y}_m\) is a random sample of size \(n_m\) from \(N(\mu_m, \sigma^2)\), such that the joint distribution of \(\boldsymbol{Y}_m\) is

\[\begin{equation} f(\boldsymbol{y}_m) = \left(\frac{1}{\sigma \sqrt{2\pi}} \right)^{n_m} \exp \left(\frac{-\sum_{i:x_i\in R_m} (y_i - \mu_m)^2}{2\sigma^2} \right). \tag{6.11} \end{equation}\]Since we are effectively modelling the \(\mu_m\), the likelihood of the means over all \(M\) leaf nodes is given by

\[\begin{equation} L(\boldsymbol{\mu}|\boldsymbol{x}) = \prod_{m=1}^{M} f(\boldsymbol{y}_m) \propto \exp \left(-\frac{1}{2}\sum_{m=1}^{M}\sum_{i:x_i\in R_m} (y_i - \mu_m)^2 \right), \tag{6.12} \end{equation}\]such that the deviance can be expressed as

\[\begin{equation} D = -2\log(L) \propto \sum_{m=1}^{M}\sum_{i:x_i\in R_m} (y_i - \mu_m)^2 = RSS. \tag{6.13} \end{equation}\]Since the deviance is directly proportional to the RSS in this setting, minimising the one is equivalent to minimising the other.

Let us turn our attention back to classification trees and consider managing their complexity.

6.2.3 Cost complexity pruning

Just like with regression trees, we must prune a fully grown classification tree to avoid overfitting. However, as with the splitting rules, we cannot use the \(RSS_{\alpha}\) criterion for pruning when the response is categorical. Similar to regression trees though, we will again minimise a specified cost complexity criterion, penalised according to the size of the tree, \(|T|\):

\[\begin{equation} C_{\alpha}(T) = C(T) + \alpha|T|, \tag{6.14} \end{equation}\]where \(C(T)\) represents a chosen cost function. Although we could use any of the aforementioned criteria, if prediction accuracy of the final pruned tree is the goal, then \(C(T)\) should be taken as the misclassification rate of tree \(T\).

The following section illustrates the application to a binary classification problem.

6.2.4 Example 7 – Titanic

The famous Titanic dataset contains information on 891 passengers that were aboard the Titanic on its one and only trans-Atlantic journey. The goal is to predict survival (yes/no) based on the predictors shown in the following table:

titanic <- read.csv('data/titanic.csv', stringsAsFactors = T)

titanic$Pclass <- as.factor(titanic$Pclass) #Class coded as integer, should be factor

datatable(titanic, options = list(scrollX = T, pageLength = 6))

Most of the features are self-explanatory. SibSp refers to the passenger’s number of siblings plus spouses on board; Parch to their number of parents and children; and Embarked to their port of embarkation12.

To start with, we will first fit a classification tree using Gini index as splitting criterion.

titanic_tree_gini <- tree(Survived ~ ., data = titanic, split = 'gini')

plot(titanic_tree_gini)

text(titanic_tree_gini, pretty = 0)

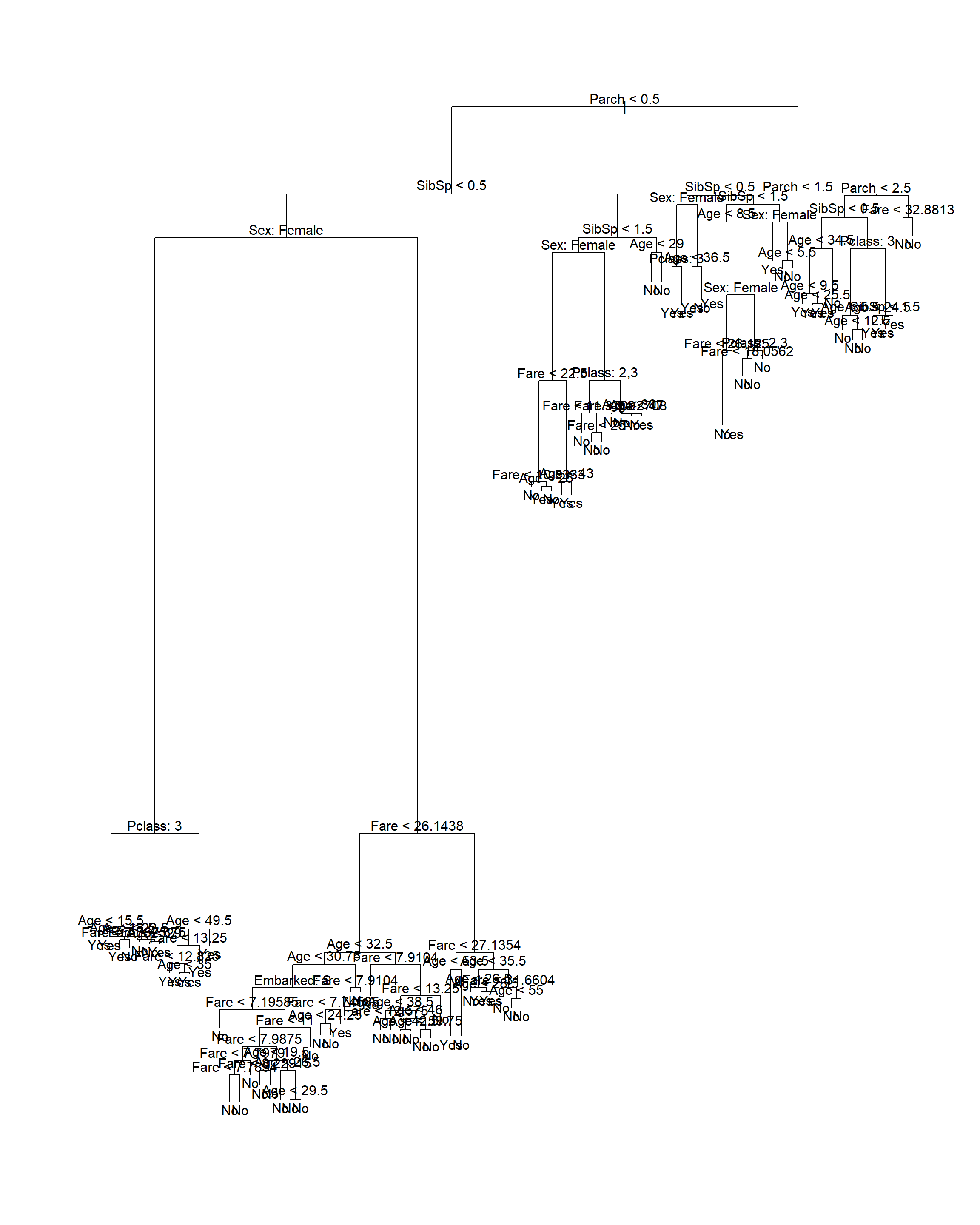

Figure 6.9: Classification tree fitted to the Titanic dataset using Gini index as splitting criterion

This yields a rather large tree, where the most useful feature (sex) is only used after a few prior splits. Compare this to the tree resulting from using deviance as splitting criterion (the default in the tree package), shown in Figure 6.10.

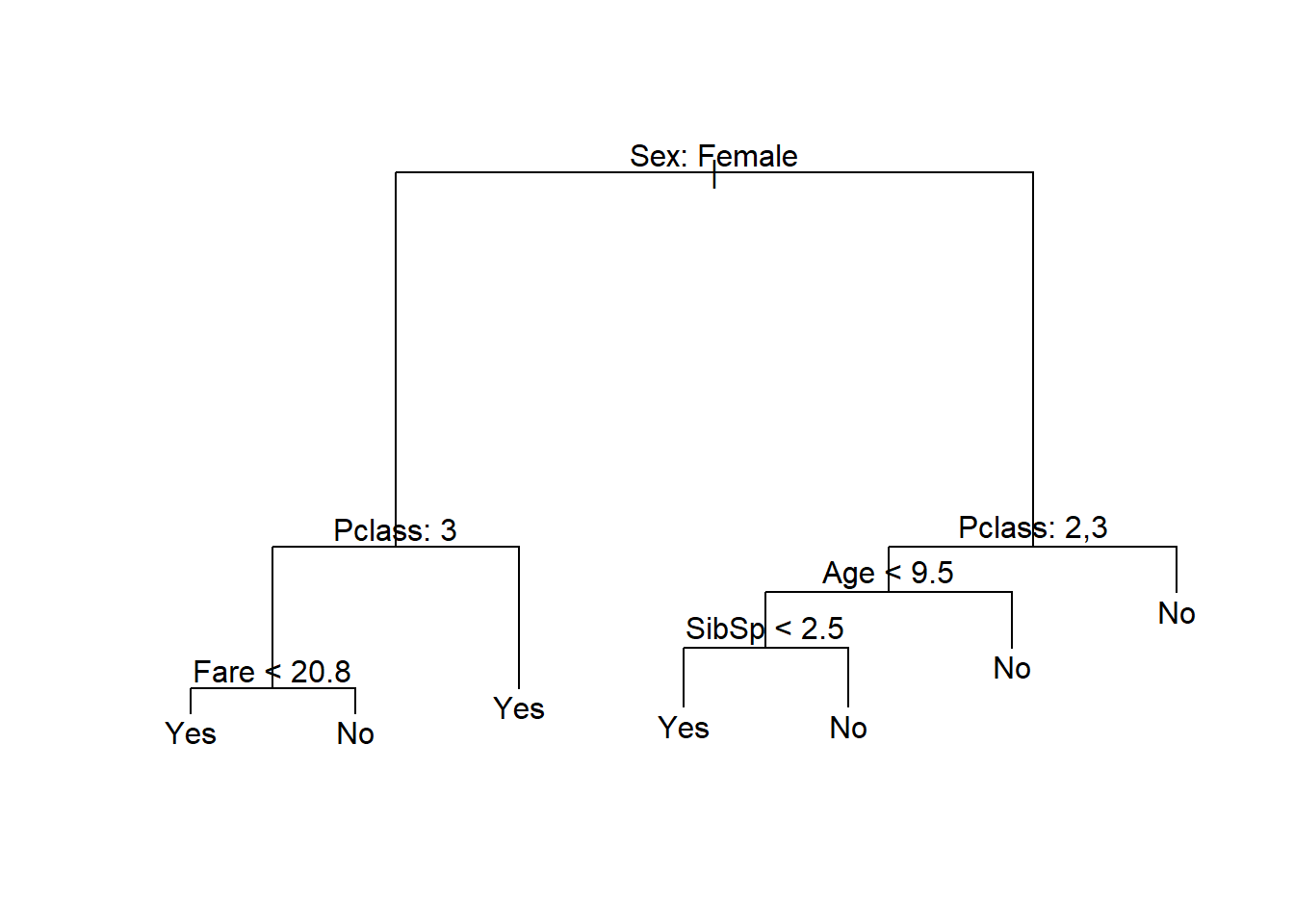

titanic_tree <- tree(Survived ~ ., data = titanic)

plot(titanic_tree)

text(titanic_tree, pretty = 0)

Figure 6.10: Classification tree fitted to the Titanic dataset using deviance as splitting criterion

This presents a similar picture to what one would expect given the emergency protocol of “women and children first”, although age was only an important factor for 2nd and 3rd class male passengers. We can extract any information for any of the nodes from the fitted object, or add different labels to the terminal nodes (see ?text.tree).

As a brief detour, let us show that the deviance measurement provided by the model’s summary indeed matches the definition set out in Equation (6.10). We will use the frame object contained in the model object to calculate the total deviance of the tree shown in Figure 6.10.

f <- titanic_tree$frame #We need the n's and the probs

n_m <- f$n[f$var == '<leaf>'] #This is total n per leaf, not per class!

p_n <- f$yprob[,1][f$var == '<leaf>'] #Pr(no) for all leaf nodes

p_y <- f$yprob[,2][f$var == '<leaf>'] #Pr(yes) for all leaf nodes

nlp <- (n_m*p_n)*log(p_n)+(n_m*p_y)*log(p_y) #\sum_k (n_k log(p_k)) for all leaves

nlp[is.nan(nlp)] <- 0 #Need to deal with log(0)

(D <- -2*sum(nlp)) #Deviance## [1] 563.8652Comparing this to the total deviance reported, we see that it indeed matches:

## [1] 563.8652Note that although the deviance splitting criterion is used in software implementation as was shown here, none of the aforementioned sources explicitly define this criterion in the relevant sections on classification trees.

Another way of exploring the fitted tree – more as an exploration tool as opposed to one for reporting – is to simply print the object:

## node), split, n, deviance, yval, (yprob)

## * denotes terminal node

##

## 1) root 714 964.500 No ( 0.59384 0.40616 )

## 2) Sex: Female 261 290.800 Yes ( 0.24521 0.75479 )

## 4) Pclass: 3 102 140.800 No ( 0.53922 0.46078 )

## 8) Fare < 20.8 79 108.500 Yes ( 0.44304 0.55696 ) *

## 9) Fare > 20.8 23 17.810 No ( 0.86957 0.13043 ) *

## 5) Pclass: 1,2 159 69.170 Yes ( 0.05660 0.94340 ) *

## 3) Sex: Male 453 459.900 No ( 0.79470 0.20530 )

## 6) Pclass: 2,3 352 298.300 No ( 0.84943 0.15057 )

## 12) Age < 9.5 30 41.050 Yes ( 0.43333 0.56667 )

## 24) SibSp < 2.5 16 0.000 Yes ( 0.00000 1.00000 ) *

## 25) SibSp > 2.5 14 7.205 No ( 0.92857 0.07143 ) *

## 13) Age > 9.5 322 225.600 No ( 0.88820 0.11180 ) *

## 7) Pclass: 1 101 135.600 No ( 0.60396 0.39604 ) *Here we can see the path containing male passengers of class 2 or 3, age \(\leq\) 9, and siblings \(\leq\) 2 had a total of 16 passengers…all of whom survived! The best way to gauge whether this is indeed a pattern in the data (as opposed to a seemingly significant pocket of random variation), is to use cross-validation to estimate out-of-sample performance for pruned trees of different sizes.

In the code below we see that one must specify the pruning cost complexity function, which we will set to the misclassification rate.

# First, grow a slightly larger tree

titanic_bigtree <- tree(Survived ~ ., data = titanic,

control = tree.control(nobs = nrow(na.omit(titanic)),

mindev = 0.005))

# Then prune it down

set.seed(28)

titanic_cv <- cv.tree(titanic_bigtree, FUN = prune.misclass) #Use classification error rate for pruning

# Make the CV plot

plot(titanic_cv$size, titanic_cv$dev, type = 'o',

pch = 16, col = 'navy', lwd = 2,

xlab = 'Number of terminal nodes', ylab='CV error')

titanic_cv$k[1] <- 0 #Don't want no -Inf

alpha <- round(titanic_cv$k,1)

axis(3, at = titanic_cv$size, lab = alpha, cex.axis = 0.8)

mtext(expression(alpha), 3, line = 2.5, cex = 1.2)

axis(side = 1, at = 1:max(titanic_cv$size))

T <- titanic_cv$size[which.min(titanic_cv$dev)] #The minimum CV Error

abline(v = T, lty = 2, lwd = 2, col = 'red')

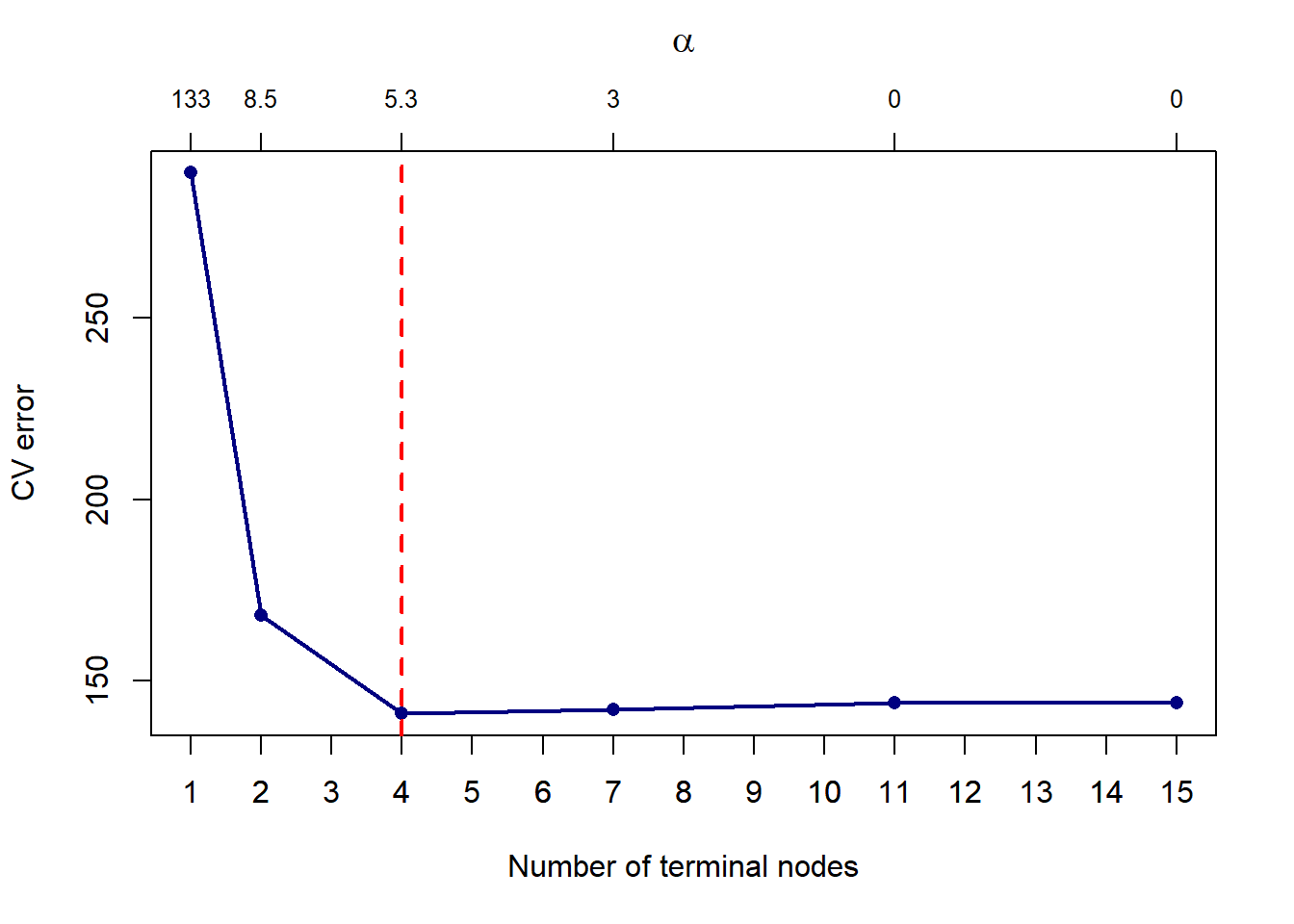

Figure 6.11: Cross-validated pruning results on a classification tree fitted to the Titanic dataset

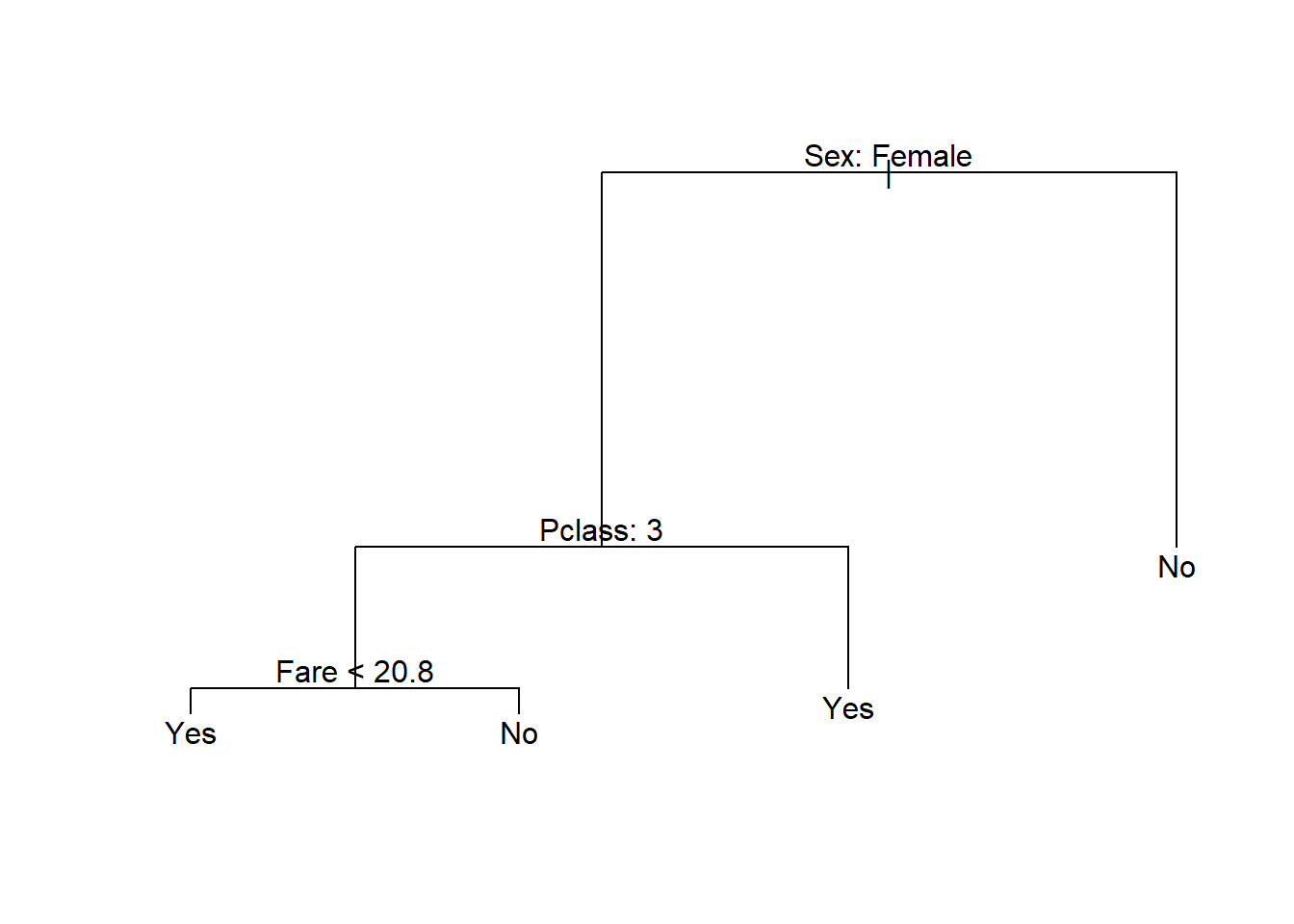

For the specific seed set above, we see that a more parsimonious model with 4 leaves yields a lower CV error, which in Figure 6.11 is given as the number of misclassifications on the y-axis. Note that different seeds will yield different result. Next we prune the tree down to 4 leaves and plot the result.

titanic_pruned <- prune.misclass(titanic_bigtree, best = T)

plot(titanic_pruned)

text(titanic_pruned, pretty = 0)

Figure 6.12: Pruned classification tree fitted to the Titanic dataset

From the resulting tree, all males would be classified as not surviving, together with female passengers in class 3 who’s fare was more than 20.8. We will once again not focus on prediction for single trees now, although we will include this as a benchmark when considering random forests and boosted trees.

In this example we saw that classification trees handle categorical predictors with ease, without the need to code dummy variables. Another benefit of this approach is that we can just as easily model target variables with multiple classes, as illustrated in the following example.

6.2.5 Example 8 – Iris

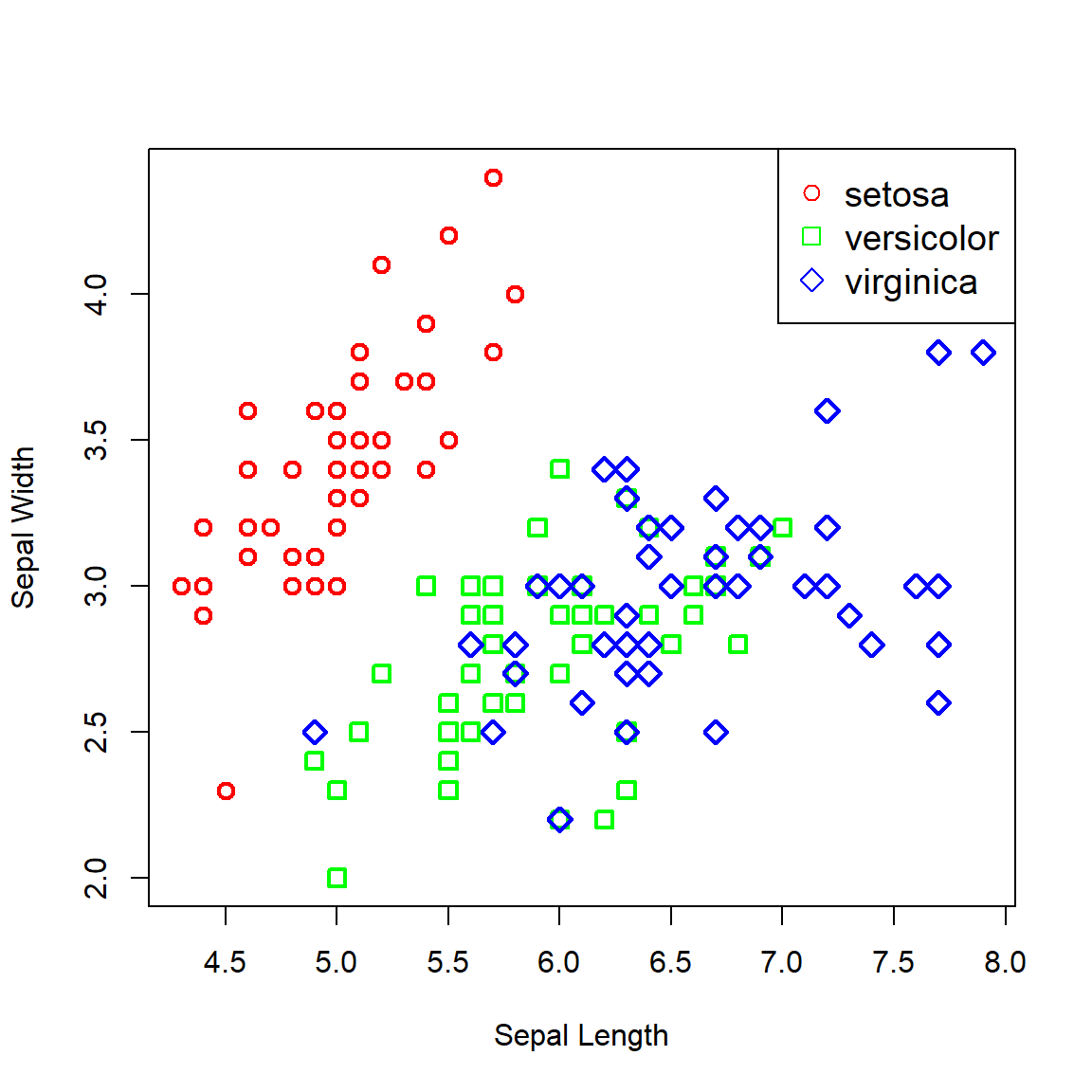

Another famous dataset, Iris contains data on 50 flowers from each of 3 species of iris. The measurements are on 4 features: sepal width, sepal length, petal width, and petal length. For the sake of illustrating the decision boundaries in two dimensions, we will only consider the sepal width and length. First, let’s plot the data:

# Load data

data('iris')

# Create index of species

ind <- as.numeric(iris$Species)

# Plot

plot(Sepal.Width ~ Sepal.Length, iris, xlab = 'Sepal Length', ylab = 'Sepal Width',

col = c('red', 'green', 'blue')[ind],

pch = c(1, 0, 5)[ind], lwd = 2, cex = 1.2)

legend(x = 'topright', legend = levels(iris$Species),

pch = c(1, 0, 5), col = c('red', 'green', 'blue'), cex = 1.2)

Figure 6.13: Iris data plotted across sepal width and length.

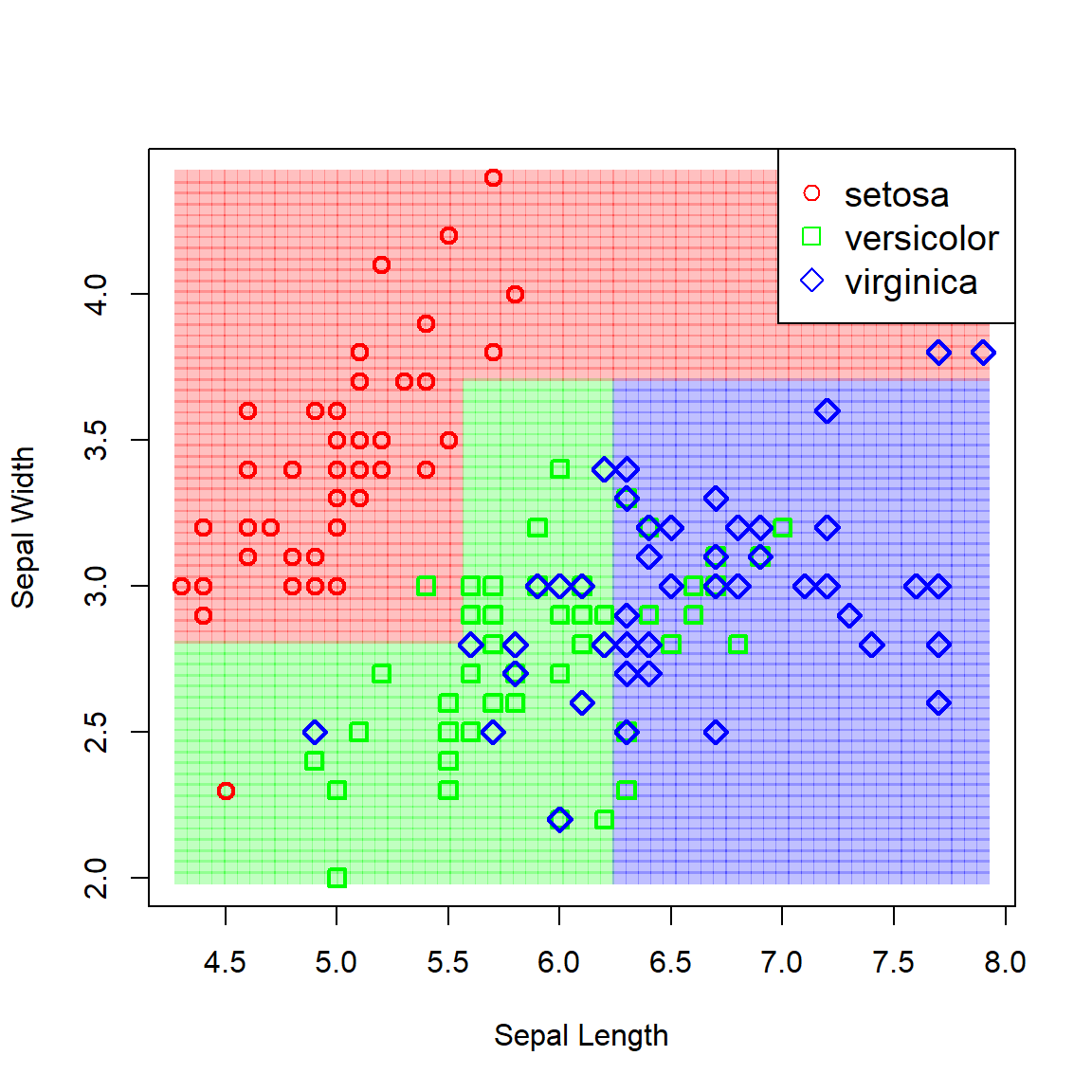

Now let’s fit a vanilla classification tree to the data and view the resulting partitioned feature space.

# Vanilla tree

iris_tree <- tree(Species ~ Sepal.Width + Sepal.Length, iris)

# Grid for predicting

x <- seq(min(iris$Sepal.Length), max(iris$Sepal.Length), length.out = 65)

y <- seq(min(iris$Sepal.Width), max(iris$Sepal.Width), length.out = 65)

fgrid <- expand.grid(Sepal.Length = x, Sepal.Width = y)

# Predict over entire space

iris_pred <- predict(iris_tree, fgrid, type = 'class')

ind_pred <- as.numeric(iris_pred)

# Custom colours

r <- rgb(255, 0, 0, maxColorValue = 255, alpha = 255*0.25)

g <- rgb(0, 255, 0, maxColorValue = 255, alpha = 255*0.25)

b <- rgb(0, 0, 255, maxColorValue = 255, alpha = 255*0.25)

# Plot the predicted classes

plot(fgrid$Sepal.Width ~ fgrid$Sepal.Length,

col = c(r, g, b)[ind_pred],

pch = 15, xlab = 'Sepal Length', ylab = 'Sepal Width')

# And add the data

points(Sepal.Width ~ Sepal.Length, iris,

col = c('red', 'green', 'blue')[ind],

pch = c(1, 0, 5)[ind], lwd = 2, cex = 1.2)

legend(x = 'topright', legend = levels(iris$Species),

pch = c(1, 0, 5), col = c('red', 'green', 'blue'), cex = 1.2)

Figure 6.14: Partitioned feature space resulting from a vanilla classification tree fitted to the iris data.

Although these boundaries capture the underlying pattern seemingly well, we might well ask whether non-orthogonal boundaries would not have been more appropriate – either linear or non-linear. This raises the question of which approach/model is “best”.

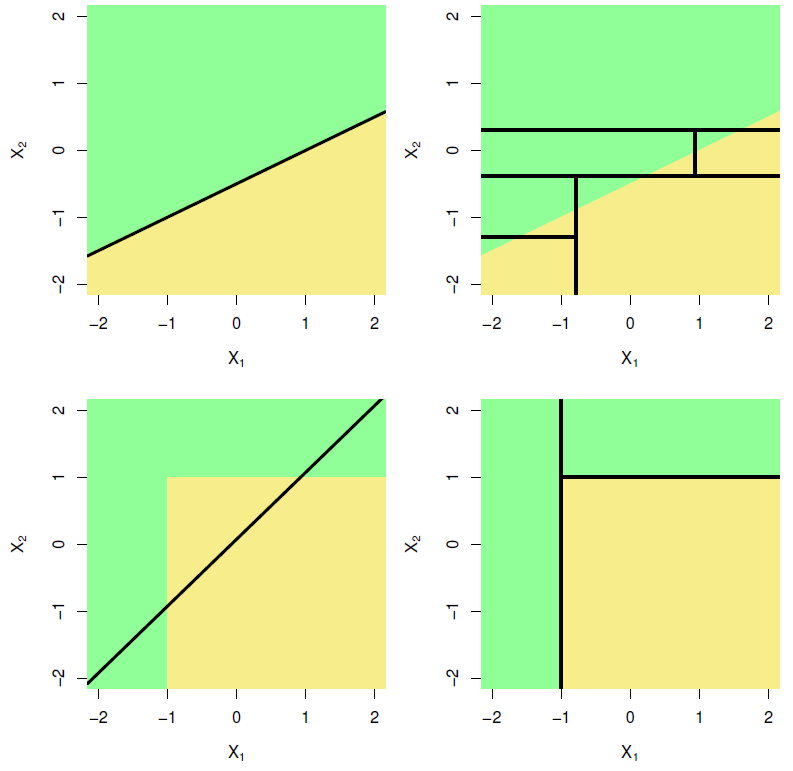

The answer is that it depends on the problem. For some cases, a particular method might work well, whilst it is entirely inappropriate for others. Figure 6.15, taken from James et al. (2013), shows two hypothetical binary classification scenarios – one where a logistic regression will yield perfect separation whilst the classification tree struggles (top), and one where a classification tree requires only two splits to perfectly capture the decision boundaries, whilst logistic regression performs poorly.

Figure 6.15: Top row: A hypothetical binary classification scenario in which logistic regression would outperform a decision tree. Bottom row: A different scenario in which the decision tree would outperform logistic regression. Source: James et al. (2013), p. 339.

Decision trees have some definite advantages:

They are very easy to explain and interpret – easier than linear regression!

Residual assumptions and multicollinearity are moot.

It mirrors human decision making.

Easily handle qualitative predictors without the need to create dummy variables.

However, one major drawback is that their predictive accuracy is generally (for most problems) not as good as most other regression and classification approaches. We will now consider two ways of improving on their predictive accuracy, namely random forests and boosting.

6.3 Bagging and random forests

The primary reason for the weak performance of decision trees on out-of-sample data is that they suffer from high sampling variability, especially on higher dimensional data. In other words, if we were to take different samples from the same population and fit trees to each sample, the results could look quite different, as seen in the following example.

For illustration purposes, consider the Sonar dataset contained in the mlbench package. The task is to determine whether sets of 60 sonar signals pertain to a metal cylinder/mine (M) or a roughly cylindrical rock (R). For every random 70/30 data split we fit a vanilla regression tree and track both the fitted tree and the resulting test classification accuracy.

library(mlbench)

library(maptree) #Better tree plotting

data(Sonar)

accs <- c()

par(mfrow=c(1,2))

set.seed(4026)

for (i in 1:100){

# Split and fit

train <- sample(1:nrow(Sonar), 0.7*nrow(Sonar))

my_tree <- tree(formula = Class ~ ., data = Sonar, subset = train)

# Predict and evaluate

yhat <- predict(my_tree, Sonar[-train,], type = 'class')

y <- Sonar[-train, 'Class']

accs <- c(accs, sum(diag(table(y, yhat)))/length(y)*100)

# Plots

draw.tree(my_tree, cex = 0.5)

plot(1:i, accs, type = 'o', pch = 16, xlab = '', ylab = 'Classification accuracy (%)',

xlim = c(1, 100), ylim = c(50, 100))

}

Figure 6.16: Different trees and test accuracies resulting from different train/test splits on the Sonar dataset

Figure 6.16 shows how the fitted model and its testing accuracy can vary extensively across different random samples, with a classification accuracy range of 30.2% in these 100 samples. Although we can manage the complexity – and, therefore, the sampling variance – to some extent through pruning, bagging and random forests offer a much more effective approach.

6.3.1 Bagging

Before defining a random forest, we first need to explain the bagging procedure (we will shortly see that a bagged tree model is a special case of a random forest). Bootstrap aggregation, or bagging, is a general purpose procedure for reducing the variance of a statistical learning method by averaging over multiple predictions.

To illustrate the concept of variance reduction, consider a set of \(n\) independent observations \(X_1, \ldots, X_n\) each with variance \(\sigma^2\). It is well known that \(\text{var}\left({\bar{X}}\right) = \frac{\sigma^2}{n}\), i.e. averaging over multiple variables reduces the variance.

If we had \(B\) training sets, we could build a statistical model on each one and average the predictions on the test set:

\[\hat{y}_{\text{ave}} = \frac{1}{B} \sum_{b=1}^B \hat{y}_b\]

The average prediction \(\hat{y}_{\text{ave}}\) will therefore have a lower sampling variance than the prediction \(\hat{y}_b\) for any single training set.

However, we of course only have one sample in practice. This is where bootstrap sampling is useful: we can construct multiple bootstrap samples by repeated sampling with replacement from the training set, then grow \(B\) unpruned trees on each of these samples. For a continuous response variable we simply average the \(B\) predictions from the regression trees for each observation, whilst for categorical responses we take a majority vote, i.e. the overall prediction for an observation is the most commonly occurring category among the \(B\) predictions.

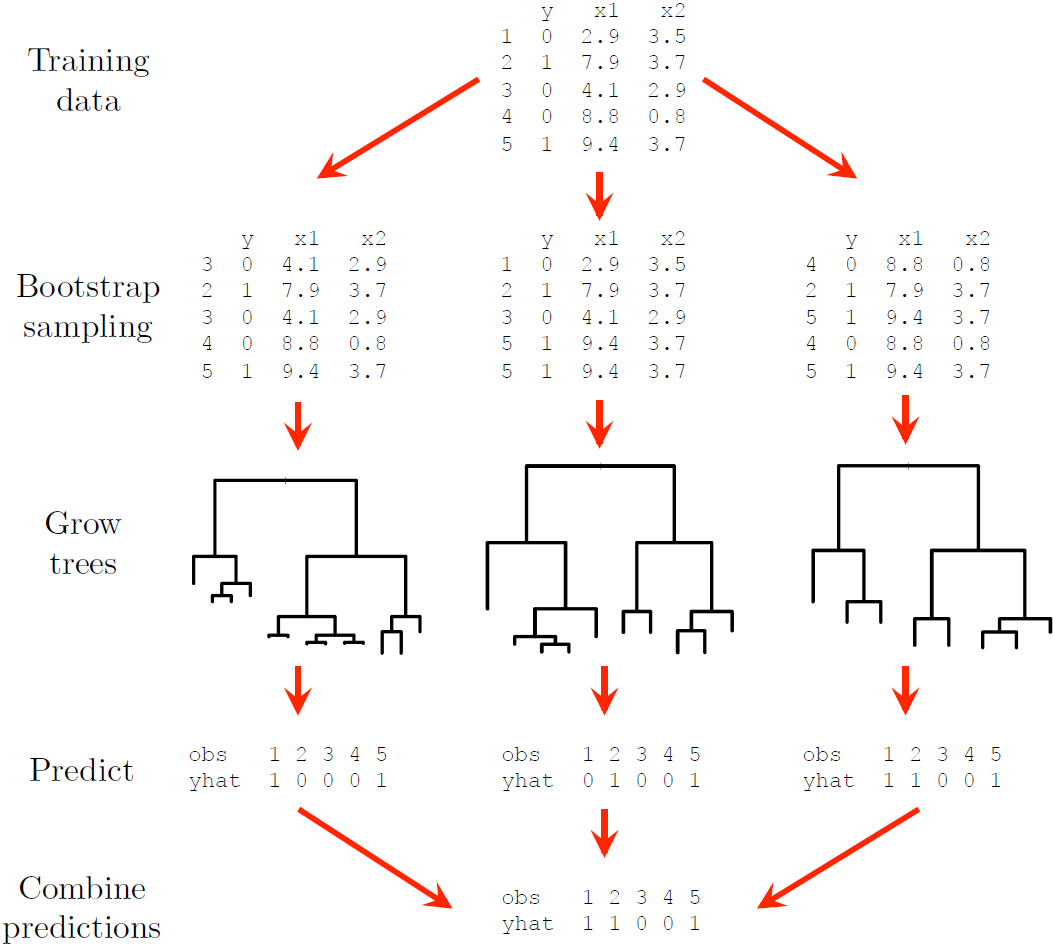

Figure 6.17 illustrates the process for a simple binary classification example with 5 observations and 3 trees. The default number of trees in most R packages is 500, which generally tends to be enough for the error to stabilise, depending on the size of the data. One can add more trees at extra computational cost, although note that since we are only reducing the prediction variability, a large value of \(B\) will not lead to overfitting.

Figure 6.17: A dummy example illustrating the bagging procedure.

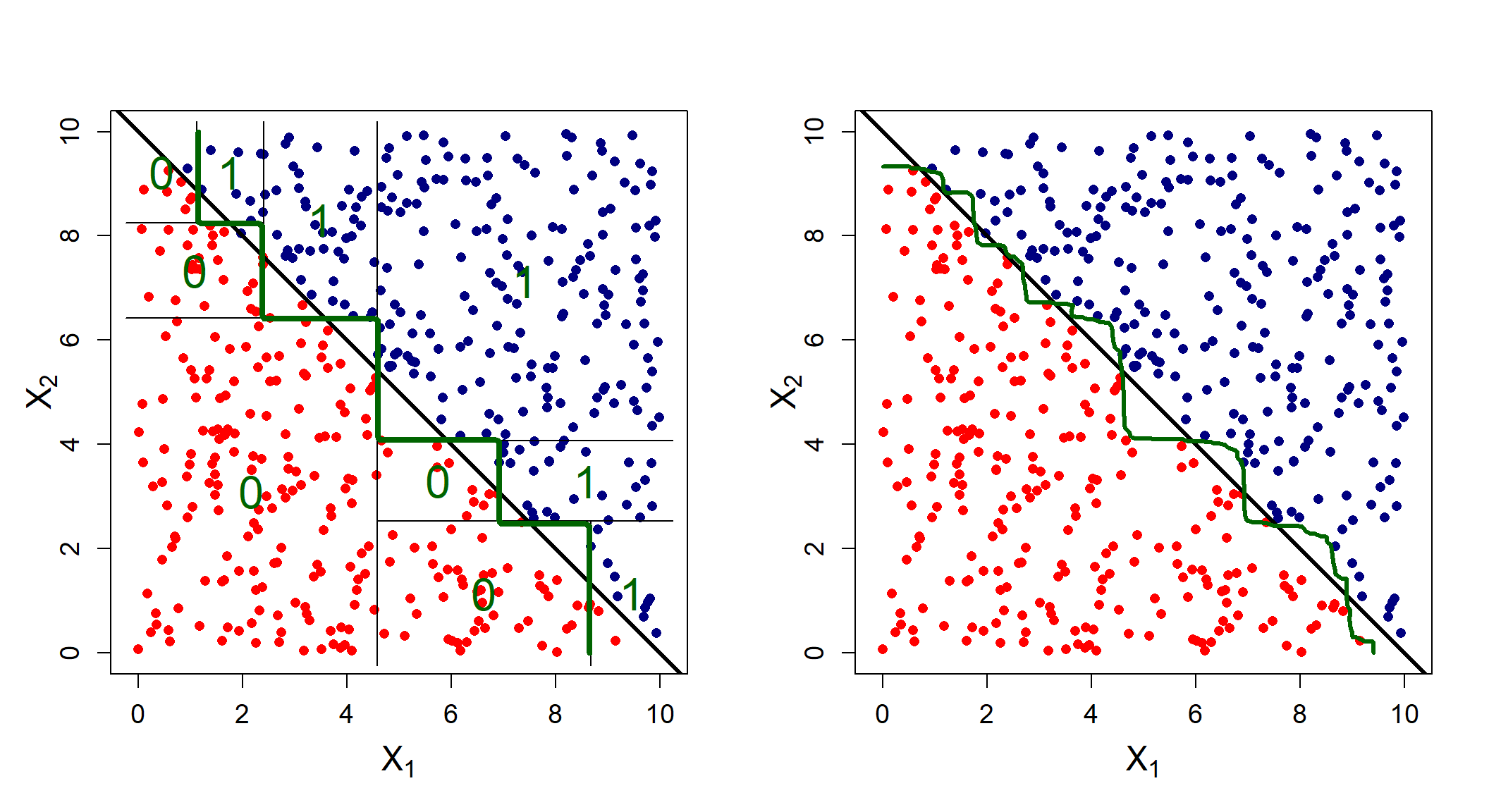

The benefit of the bagging procedure above a single tree is easily measured by out-of-sample performance, which in essence means that this procedure does better at capturing the true underlying relationship, \(f\). This is seen by investigating the decision boundaries, as shown for simulated linearly separable data in Figure 6.18.

library(randomForest)

par(mfrow = c(1, 2))

# Simulate random points

set.seed(123)

x1 <- runif(500, 0, 10)

x2 <- runif(500, 0, 10)

y <- as.factor(ifelse(x2 <= 10 - x1, 0, 1)) # With a linear decision boundary

# Tree first

mytree <- tree(y ~ x1 + x2, split = 'gini')

# Checked separately that 10 nodes is a good size (verify with cv.tree)

pruned_tree <- prune.tree(mytree, best = 10, method = 'misclass')

plot(x1, x2, col = ifelse(y == 0, 'red', 'navy'), pch = 16, xlim = c(0, 10), ylim = c(0, 10),

xlab = expression(X[1]), ylab = '', cex.axis = 1.2, cex.lab = 1.5, asp = 1)

title(ylab = expression(X[2]), line = 1.8, cex.lab = 1.5) #ylab was being cut off

# Boundaries

abline(10, -1, lwd=3)

partition.tree(pruned_tree, add = T, lwd = 6, col = 'darkgreen', cex = 2)

x <- seq(0, 10, length = 100)

fgrid <- expand.grid(x1 = x, x2 = x)

yhat <- predict(pruned_tree, fgrid)[, 2]

contour(x, x, matrix(yhat, 100, 100), add = T,

levels = 0.5, drawlabels = F, lwd = 4, col = 'darkgreen')

# Now bagged model (special case of random forest with m = p)

mybag <- randomForest(y ~ x1 + x2, mtry = 2)

# Plot

plot(x1, x2, col = ifelse(y == 0, 'red', 'navy'), pch = 16, xlim = c(0, 10), ylim = c(0, 10),

xlab = expression(X[1]), ylab = '', cex.axis = 1.2, cex.lab = 1.5, asp = 1)

title(ylab = expression(X[2]), line = 1.8, cex.lab = 1.5) #ylab was being cut off

# Boundaries

abline(10, -1, lwd=3)

yhat <- predict(mybag, fgrid, type = 'prob')[, 2]

contour(x, x, matrix(yhat, 100, 100), add = T,

levels = 0.5, drawlabels = F, lwd = 3, col = 'darkgreen')

Figure 6.18: Estimated (green) vs actual (black) decision boundaries for a single tree (left) compared to a vanilla bagged model (right).

Here we see that the bagged model better approximates the decision boundary. Of course, one would rather fit a linear logistic regression to such a problem, but what about scenarios where the decision boundary is especially non-linear?

library(randomForest)

library(plotrix) #For drawing the circle

par(mfrow = c(1, 2))

# Simulate random points

set.seed(123)

x1 <- runif(1000, 0, 10)

x2 <- runif(1000, 0, 10)

circ <- (x1 - 5)^2 + (x2 - 5)^2

y <- as.factor(ifelse(circ <= 3^2, 0, 1))

# Tree first

mytree <- tree(y ~ x1 + x2)

# Checked separately that 5 nodes is a good size (verify with cv.tree)

pruned_tree <- prune.tree(mytree, best = 5, method = 'misclass')

plot(x1, x2, col = ifelse(y == 0, 'red', 'navy'), pch = 16, xlim = c(0, 10), ylim = c(0, 10),

xlab = expression(X[1]), ylab = '', cex.axis = 1.2, cex.lab = 1.5, asp = 1)

title(ylab = expression(X[2]), line = 1.8, cex.lab = 1.5) #ylab was being cut off

# Boundaries

draw.circle(5, 5, 3, nv = 100, border = 'black', col = NA, lwd = 4)

partition.tree(pruned_tree, add = T, lwd = 6, col = 'darkgreen', cex = 2)

x <- seq(0, 10, length = 150)

fgrid <- expand.grid(x1 = x, x2 = x)

yhat <- predict(pruned_tree, fgrid)[, 2]

contour(x, x, matrix(yhat, 150, 150), add = T,

levels = 0.5, drawlabels = F, lwd = 4, col = 'darkgreen')

# Now bagged model (special case of random forest with m = p)

mybag <- randomForest(y ~ x1 + x2, mtry = 2)

# Plot

plot(x1, x2, col = ifelse(y == 0, 'red', 'navy'), pch = 16, xlim = c(0, 10), ylim = c(0, 10),

xlab = expression(X[1]), ylab = '', cex.axis = 1.2, cex.lab = 1.5, asp = 1)

title(ylab = expression(X[2]), line = 1.8, cex.lab = 1.5) #ylab was being cut off

# Boundaries

draw.circle(5, 5, 3, nv = 100, border = 'black', col = NA, lwd = 4)

yhat <- predict(mybag, fgrid, type = 'prob')[, 2]

contour(x, x, matrix(yhat, 150, 150), add = T,

levels = 0.5, drawlabels = F, lwd = 3, col = 'darkgreen')

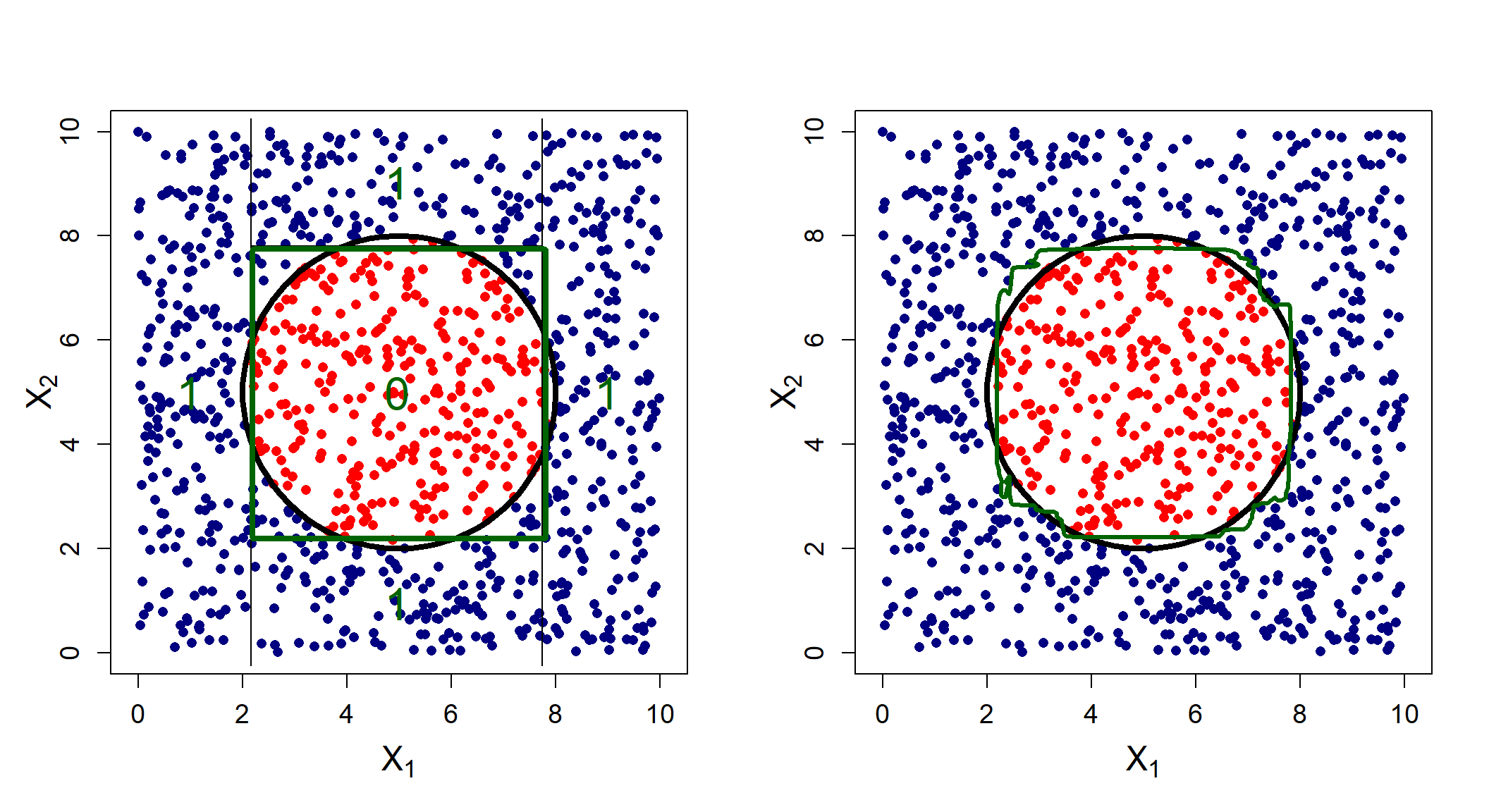

Figure 6.19: Estimated (green) vs actual (black) decision boundaries for a single tree (left) compared to a vanilla bagged model (right).

Figure 6.19 again shows that although the tree does roughly capture the overall pattern, its orthogonal splits struggle to capture the circular boundary, whereas the bagged model adjusts appropriately to some extent.

6.3.2 Out-of-bag error estimation

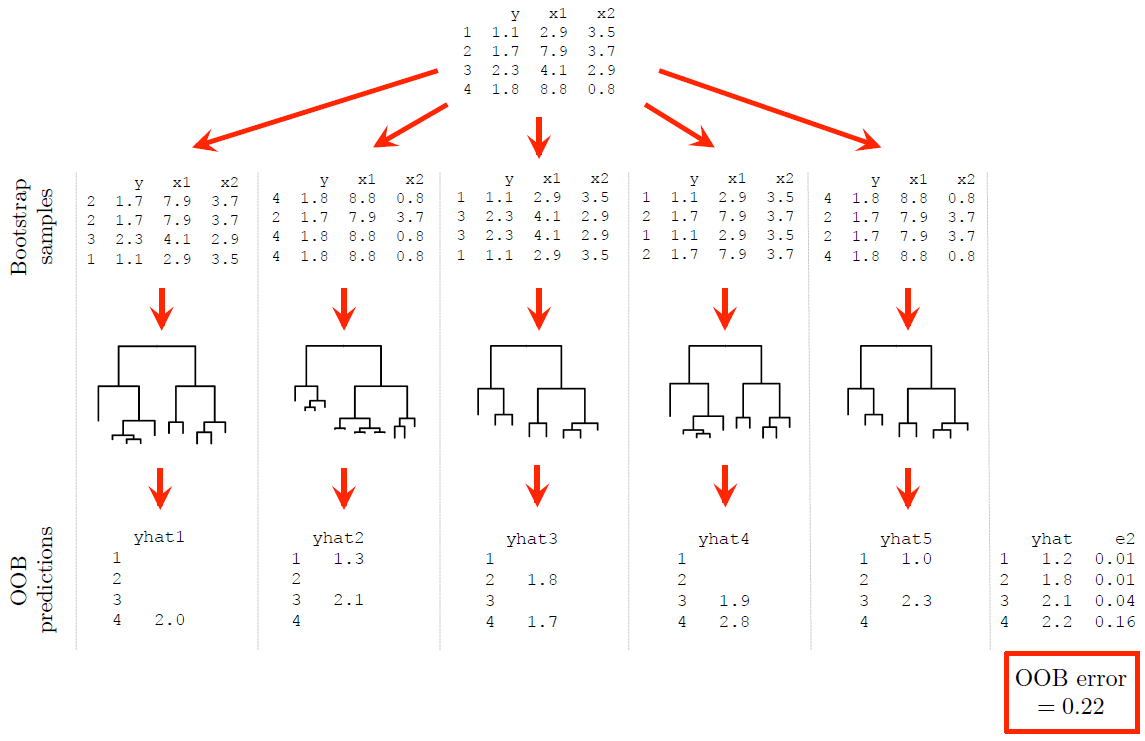

One convenient upshot of this approach is the built-in capability of estimating the test error without the need for cross-validation. This is due to the fact that each bagged tree only uses approximately 2/3 of the observations on average \(\left(\frac{e-1}{e}\text{, to be exact}\right)\). The remaining ~1/3 observations \(\left(\frac{1}{e}\right)\) not used to grow a bagged tree are called out-of-bag (OOB) observations.

To obtain an estimate of the test error, we simply predict the response for observation \(i\) using each of the bagged trees for which that observation was OOB. This will yield approximately \(\frac{B}{3}\) predictions per observation, which are then combined into a single prediction per observation by either computing the OOB RSS (regression trees) or OOB classification error (classification trees). Since this error rate is based on out-of-sample observations, it serves as an estimate of the test error, just like cross-validation errors.

Figure 6.20 again illustrates the process for a simple regression example (note that some rounding was applied for ease of presentation).

Figure 6.20: A dummy example illustrating out-of-bag (OOB) error estimation.

6.3.3 Variable importance

When we bag a large number of trees, we lose some of the interpretation qualities of decision trees since it is no longer possible to represent the model with a single tree. We can, however, measure the variable importance for each predictor.

The two most commonly reported measures are impurity-based importance and permutation importance. Although they often lead to similar rankings, they quantify importance in fundamentally different ways.

Impurity-based importance (Mean Decrease in Impurity)

Each split in a regression tree reduces the residual sum of squares (RSS). In a random forest, we can aggregate the total reduction in RSS attributable to a predictor across all trees and all splits. The importance of variable \(X_j\) is therefore

\[ \text{VI}_j = \sum_{\text{trees}} \sum_{\text{splits on } X_j} \Delta \text{RSS}. \]

This measures how much the variable contributes to reducing training error during tree construction. The advantage of this approach is that it is computationally inexpensive, since the reductions are already calculated when the trees are grown. However, it is known to be biased in favour of continuous variables or predictors with many possible split points, since these have more opportunities to achieve large impurity reductions.

Permutation importance (Mean Decrease in Accuracy)

Permutation importance measures the increase in prediction error when the values of a predictor are randomly permuted. After the model has been fitted, we:

- Compute the baseline prediction error.

- Randomly shuffle the values of \(X_j\) in the validation (or out-of-bag) data.

- Recompute the prediction error.

- Attribute the increase in error to the importance of \(X_j\).

Formally, if \(\text{Err}\) denotes the prediction error, then

\[ \text{VI}_j = \text{Err}_{\text{perm}(X_j)} - \text{Err}_{\text{original}}. \]

This measure is directly tied to predictive performance and quantifies how much model performance deteriorates when the information contained in \(X_j\) is removed. Its main drawback is that it is computationally more expensive and can be unstable in the presence of highly correlated predictors, since other variables may partially compensate for the permuted feature.

In practice, both measures aim to quantify the contribution of each predictor, but they reflect different aspects of the model: impurity-based importance reflects the internal mechanics of tree construction, whereas permutation importance reflects the impact of a variable on predictive performance.

Now that we have motivated for bagged trees and explored some of their uses, we will make one tweak to the algorithm, thereby defining random forests.

6.3.4 Random forests

We have established that bagging reduces the sampling variability of predictions by averaging over many trees. However, if the trees are highly correlated, this improvement will be limited.

Consider again a set of random variables \(X_1, \ldots, X_n\) with common variance \(\sigma^2\), but this time suppose they are not independent, such that there is some non-zero correlation. We have that

\[\text{var}\left({\bar{X}}\right) = \frac{\sigma^2}{n} + \frac{2\sigma^2}{n^2} \sum_{i\ne j} \rho_{ij}.\] Therefore, the stronger the correlation, the greater the variance of the average. Random forests provide an improvement over bagged trees by making a small change that decorrelates the trees.

Suppose that there is one very strong predictor in a dataset – most of the bagged trees will use this predictor. Consequently, the bagged trees will look quite similar to each other and their predictions will therefore be highly correlated. As with bagging, a random forest is constructed by growing \(B\) decision trees on \(B\) bootstrapped samples. However, each time a split is considered, a random sample of \(m < p\) predictors are chosen as split candidates such that, on average, \(\frac{p-m}{p}\) of the splits will not even consider the strong predictor.

This has the effect of decorrelating the trees, causing the average predictions to be less variable between samples, thereby further reducing the variance component of the total error. In the R package randomForest (amongst others) the default is \(m = \lfloor \sqrt{p} \rfloor\) for classification trees and \(m = \lfloor p/3 \rfloor\) for regression trees.

Note that bagging is a special case of a random forest with \(m = p\). As with bagging, we can estimate the testing error by means of the OOB errors and we can also report the importance of each predictor across all splits across all trees in the forest. We will explore the application by returning to the earlier examples for both regression and classification.

6.3.5 Example 6 – California housing (continued)

After applying an 80/20 data split into training and testing sets, we will start by using the randomForest package to fit both a vanilla random forest and a bagged model to the California housing dataset, both using 250 trees. We will also keep track of the training times13.

# Train/test split

set.seed(4026)

train <- sample(1:nrow(calif), 0.8*nrow(calif))

# Bagging

bag_250_time <- system.time(

calif_bag <- randomForest(HousePrice ~ ., data = calif, subset = train,

mtry = ncol(calif) - 1, #Use all features (minus response)

ntree = 250,

importance = T, #Keep track of importance (faster without)

#do.trace = 25, #Can keep track of progress if we want

na.action = na.exclude)

)

# Random Forest

rf_250_time <- system.time(

calif_rf <- randomForest(HousePrice ~ ., data = calif, subset = train,

ntree = 250,

importance = T,

na.action = na.exclude)

)From the model object we can extract much information on the fit (see calif_rf$...). For example, we can see that the random forest’s trees contained on average 10985 terminal nodes! We can also look at the percentage of variation in \(Y\) captured by the model, i.e. the coefficient of determination (\(R^2\)), by just printing the model object:

##

## Call:

## randomForest(formula = HousePrice ~ ., data = calif, mtry = ncol(calif) - 1, ntree = 250, importance = T, subset = train, na.action = na.exclude)

## Type of random forest: regression

## Number of trees: 250

## No. of variables tried at each split: 8

##

## Mean of squared residuals: 0.05236698

## % Var explained: 83.83##

## Call:

## randomForest(formula = HousePrice ~ ., data = calif, ntree = 250, importance = T, subset = train, na.action = na.exclude)

## Type of random forest: regression

## Number of trees: 250

## No. of variables tried at each split: 2

##

## Mean of squared residuals: 0.05985603

## % Var explained: 81.52Verifying this calculation manually (just for the random forest model):

y_calif <- calif[train, ]$HousePrice

yhat_calif_rf <- calif_rf$predicted

# Calculate SSR = 1 - SSE/SST

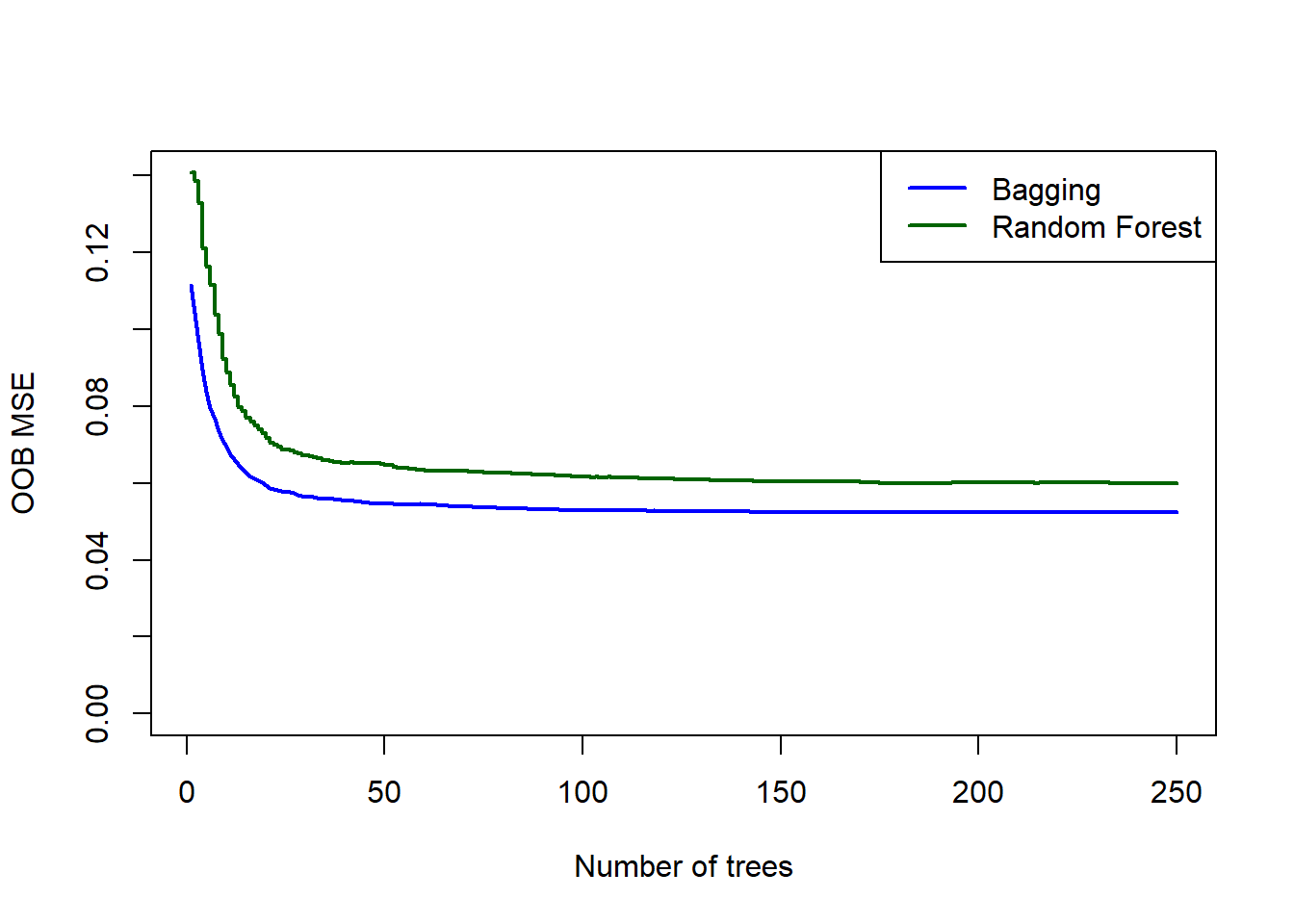

round((1 - sum((y_calif - yhat_calif_rf)^2)/sum((y_calif - mean(y_calif))^2))*100, 2)## [1] 81.52Interestingly, we see that the bagged model has the higher \(R^2\). Comparing their OOB error plots, we see that the bagged model also yields better (lower) errors:

plot(calif_bag$mse, type = 'l', xlab = 'Number of trees', ylab = 'OOB MSE',

col = 'blue', lwd = 2, ylim = c(0, max(calif_rf$mse)))

lines(calif_rf$mse, col = 'darkgreen', lwd = 2, type = 's')

legend('topright', legend = c('Bagging', 'Random Forest'),

col = c('blue', 'darkgreen'), lwd = 2)

Figure 6.21: OOB errors for the bagged tree and random forest (default m) fitted to the California housing dataset.

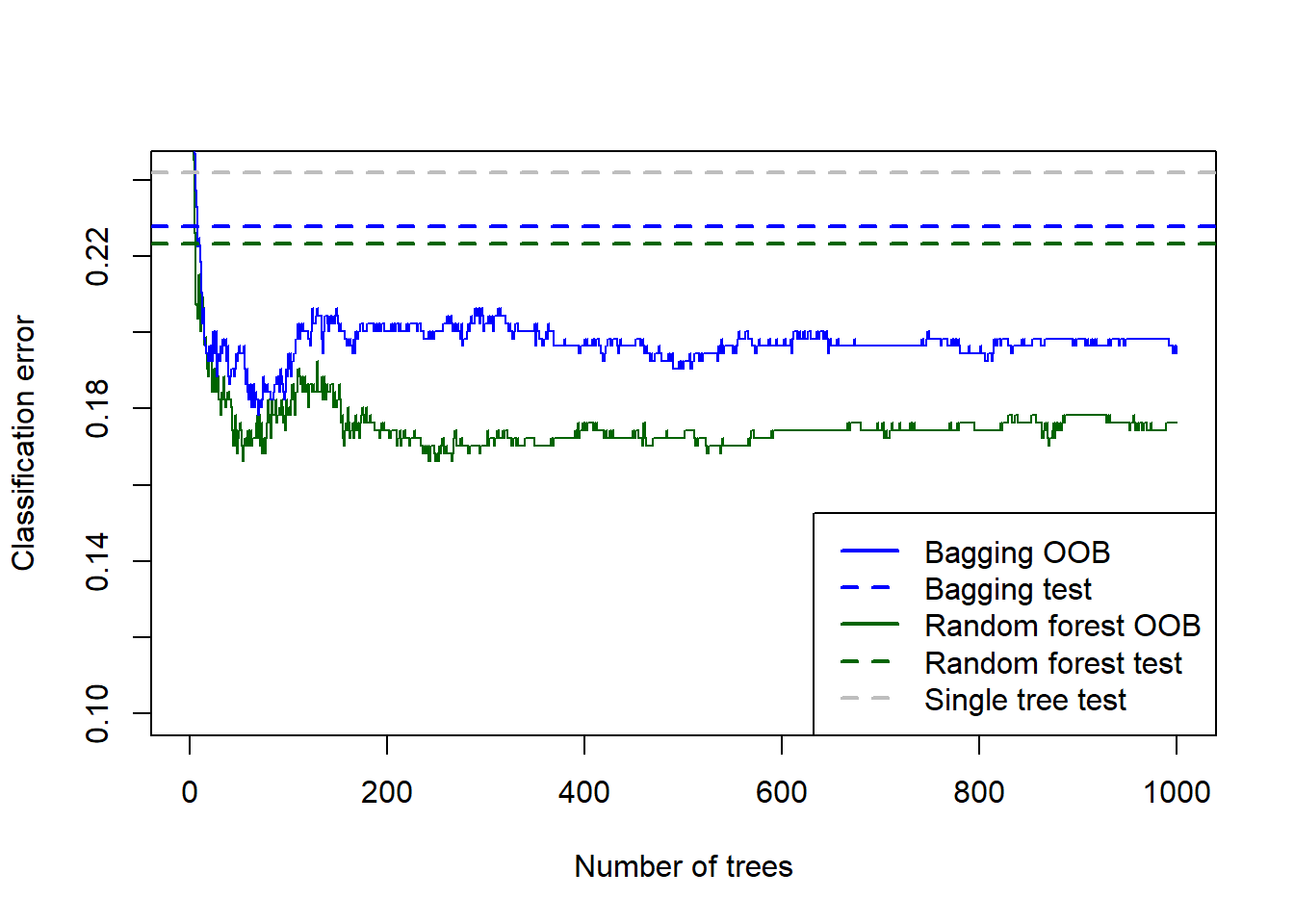

Based on this, if we had to choose a model between these two, we would pick the bagged model. We will, however, apply both to the test set to compare the OOB estimates to the observed test errors. For comparison, let us add the test error for a single pruned tree as well.

# Quick single tree

stopcrit <- tree.control(nobs = length(train), mindev = 0.002)

calif_tree_overfit <- tree(HousePrice ~ ., data = calif[-train, ], control = stopcrit)

set.seed(4026)

calif_cv <- cv.tree(calif_tree_overfit)

T <- calif_cv$size[which.min(calif_cv$dev)]

calif_pruned <- prune.tree(calif_tree_overfit, best = T)

# Predictions

calif_bag_pred <- predict(calif_bag, newdata = calif[-train, ])

calif_rf_pred <- predict(calif_rf, newdata = calif[-train, ])

calif_tree_pred <- predict(calif_pruned, newdata = calif[-train, ])

# Prediction accuracy

y_calif_test <- calif[-train, 1]

calif_bag_mse <- mean((y_calif_test - calif_bag_pred)^2)

calif_rf_mse <- mean((y_calif_test - calif_rf_pred)^2)

calif_tree_mse <- mean((y_calif_test - calif_tree_pred)^2)

# Plot MSEs

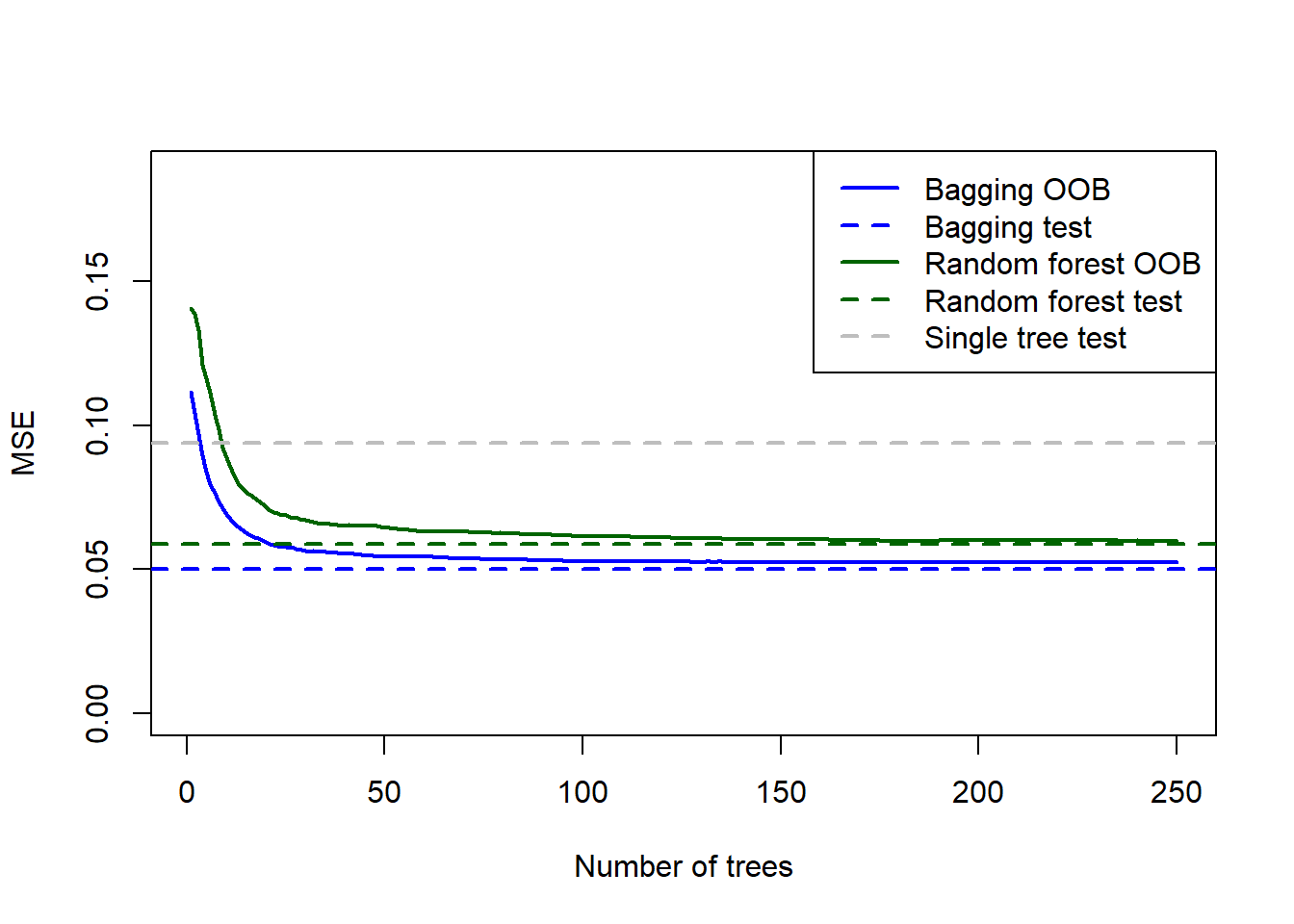

plot(calif_bag$mse, type = 'l', xlab = 'Number of trees', ylab = 'MSE',

col = 'blue', lwd = 2, ylim = c(0, calif_tree_mse*2))

lines(calif_rf$mse, col = 'darkgreen', lwd = 2)

abline(h = calif_bag_mse, col = 'blue', lty = 2, lwd = 2)

abline(h = calif_rf_mse, col = 'darkgreen', lty = 2, lwd = 2)

abline(h = calif_tree_mse, col = 'grey', lty = 2, lwd = 2)

legend('topright', legend = c('Bagging OOB', 'Bagging test', 'Random forest OOB', 'Random forest test', 'Single tree test'),

col = c('blue', 'blue', 'darkgreen', 'darkgreen', 'grey'), lwd = 2, lty = c('solid', 'dashed', 'solid', 'dashed', 'dashed'))

Figure 6.22: Testing errors for the bagged tree, random forest (default m), and single tree fitted to the California housing dataset, added to the OOB plots.

As expected, the model with \(m=8\) performed better on the test set. It is also interesting to note that for both models, the OOB error slightly overestimated the testing error. The bagged model’s test MSE of 0.05 is approximately half of the pruned regression tree test MSE (0.09).

Looking at the training times (in seconds), we see that it executed fairly quickly, even for this moderately-sized dataset:

## user system elapsed

## 111.49 0.27 111.99## user system elapsed

## 61.30 0.30 61.74The ranger package offers inter alia built-in parallelisation across cores to improve runtimes significantly. Fitting the bagged model using this package:

library(ranger)

ranger_time <- system.time(

ranger_bag <- ranger(formula = HousePrice ~ .,

data = calif[train, ],

num.trees = 250,

mtry = ncol(calif) - 1)

)We observe a significantly faster runtime:

## user system elapsed

## 19.77 0.53 1.69The model object also has some neat output to explore. For example, let’s investigate the 100th tree in the forest:

## nodeID leftChild rightChild splitvarID splitvarName splitval terminal prediction

## 1 0 1 2 0 Income 3.84240 FALSE NA

## 2 1 3 4 0 Income 2.45985 FALSE NA

## 3 2 5 6 0 Income 5.77605 FALSE NA

## 4 3 7 8 6 Latitude 34.44500 FALSE NA

## 5 4 9 10 6 Latitude 38.48500 FALSE NA

## 6 5 11 12 1 HouseAge 38.50000 FALSE NANote, however, that since the trees are fitted in parallel we cannot keep track of OOB MSE as the number of trees increase; we can only extract the final OOB MSE.

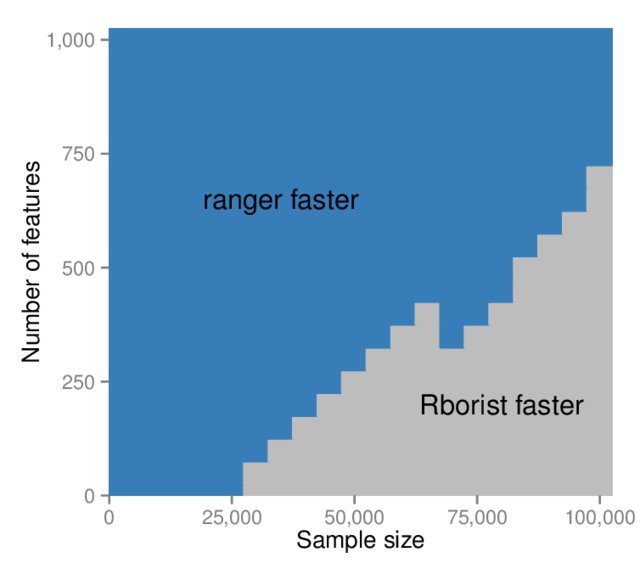

Another option for faster random forest implementation is Rborist. Wright & Ziegler (2017) compares the two packages across a range of combinations of observations and features. The result is neatly summarised in Figure 6.23, taken from that paper.

Figure 6.23: Runtime comparison of ranger with Rborist (classification, 1000 trees per run). Source: Wright & Ziegler (2017).

We see that for the California dataset, ranger will still be faster. We can now leverage the speed of this package to answer an important question, namely which value of \(m\) is best for this example. In the analyses above we only used \(m = p = 8\) and \(m = \lfloor p/3 \rfloor = 2\), but perhaps another value would yield better results. To determine this, we will use caret to perform a hyperparameter grid search (using ranger) across all possible values of \(m\). We can also control the tree depth, therefore we will try different size trees as well. We will again use 250 trees.

library(caret)

set.seed(1)

# Create combinations of hyperparameters

# see getModelInfo()$ranger$parameters

calif_rf_grid <- expand.grid(mtry = 2:(ncol(calif) - 1),

splitrule = 'variance', #Must specify. This is RSS for regression

min.node.size = c(1, 5, 20)) #Default for regression is 5. Controls tree size

ctrl <- trainControl(method = 'oob', verboseIter = F) #Can set to T to track progress

# Use ranger to run all these models

calif_rf_gridsearch <- train(HousePrice ~ .,

data = calif,

subset = train,

method = 'ranger',

num.trees = 250,

importance = 'impurity',

#verbose = T,

trControl = ctrl,

tuneGrid = calif_rf_grid) #Here is the gridThe hyperparameter combination that yielded the best OOB result is as follows:

## Ranger result

##

## Call:

## ranger::ranger(dependent.variable.name = ".outcome", data = x, mtry = min(param$mtry, ncol(x)), min.node.size = param$min.node.size, splitrule = as.character(param$splitrule), write.forest = TRUE, probability = classProbs, ...)

##

## Type: Regression

## Number of trees: 250

## Sample size: 16512

## Number of independent variables: 8

## Mtry: 7

## Target node size: 5

## Variable importance mode: impurity

## Splitrule: variance

## OOB prediction error (MSE): 0.05215617

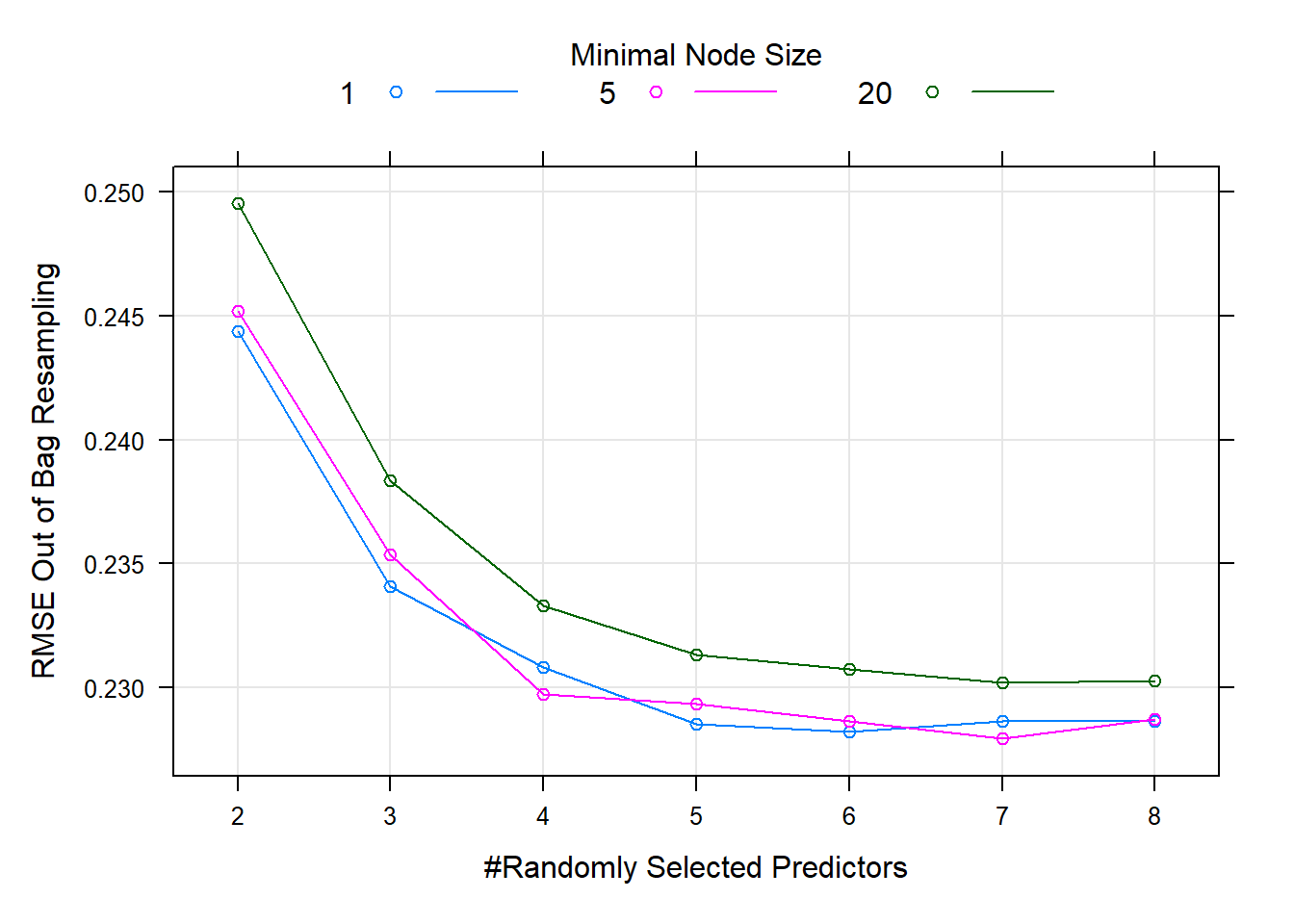

## R squared (OOB): 0.8389851According to this process, the best random forest model was one with \(m =\) 7 and terminal nodes of size 5. A particularly useful feature of caret’s train() function is the trivially easy plotting of the hyperparameter tuning results, allowing one to see not only which combination was best, but also how it compared to others, as well as the effect of changing certain hyperparameters. This is shown in Figure 6.24.

Figure 6.24: Hyperparameter combinations results for a random forest fitted to the California housing dataset.

There does not seem to be much difference between using entirely overfitted trees (minimal node size = 1) and ones with a minimal node size of 5, but increasing the node size to 20 (reducing the trees’ size) yielded worse performance for all values of \(m\). Although there is not much in it, we will now use the model that yielded the lowest OOB error to predict on the test set.

calif_rfgrid_pred <- predict(calif_rf_gridsearch, newdata = calif[-train,])

mean((y_calif_test - calif_rfgrid_pred)^2)## [1] 0.05024634Comparing this to the \(m=8\) model from earlier, we see a miniscule improvement on its test MSE of 0.0502557, although the difference is negligible. To reiterate: in practice, one would only use the test set to get one final prediction after selecting a model based on CV/OOB errors. This test set comparison was merely for illustration.

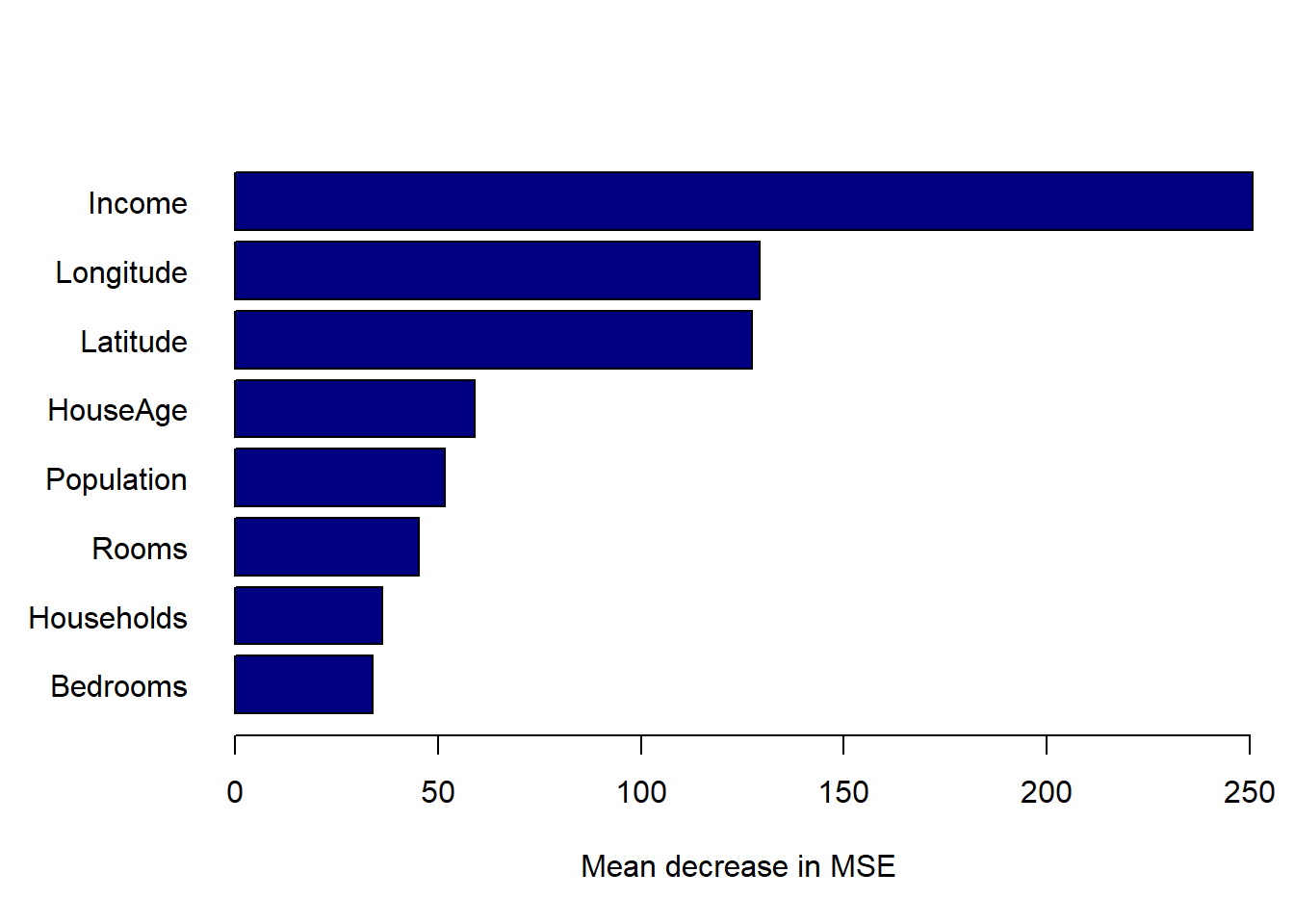

Finally, let’s look at the variable importance plot. Although most packages contain their own built-in variable importance plotting functions, it is most convenient to use packages designed specifically for this purpose, like vip, to ensure standard presentation across different model classes. Note we measured impurity-based variable importance during training, which we can extract from the model object. We can use vi_permute() to calculate permutation importance (see an example of this later), or we can retrain the model and keep track of perumtation importance this time. Given the speed of ranger, we will do the latter here.

library(vip)

library(ggplot2)

library(patchwork) #Easy way to combine ggplots

calif_rf_besthp <- calif_rf_gridsearch$bestTune

calif_rf_perm <- ranger(

HousePrice ~ .,

data = calif[train, ],

num.trees = 250,

mtry = calif_rf_besthp$mtry,

min.node.size = calif_rf_besthp$min.node.size,

splitrule = calif_rf_besthp$splitrule,

importance = 'permutation',

seed = 123

)

crf_imp_p <- vip(calif_rf_gridsearch) +

labs(

title = 'Impurity Variable Importance',

x = 'Increase in Prediction Error',

y = NULL

) +

theme_minimal()

crf_per_p <- vip(calif_rf_perm) +

labs(

title = 'Permutation Variable Importance',

x = 'Decrease in Splitting Criterion',

y = NULL

) +

theme_minimal()

crf_per_p + crf_imp_p

Figure 6.25: Variable importance plots for the tuned random forest fitted to the California housing dataset.

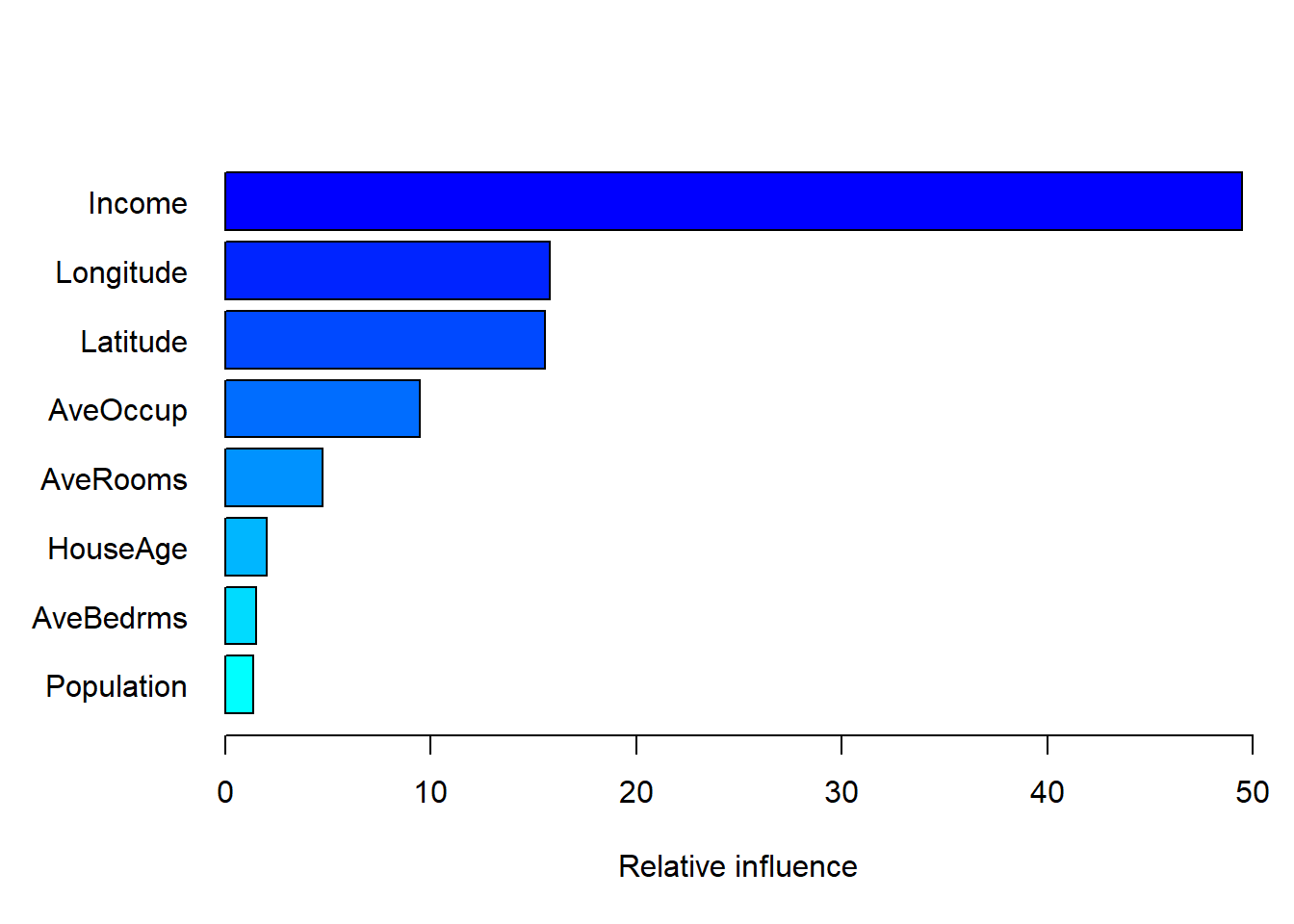

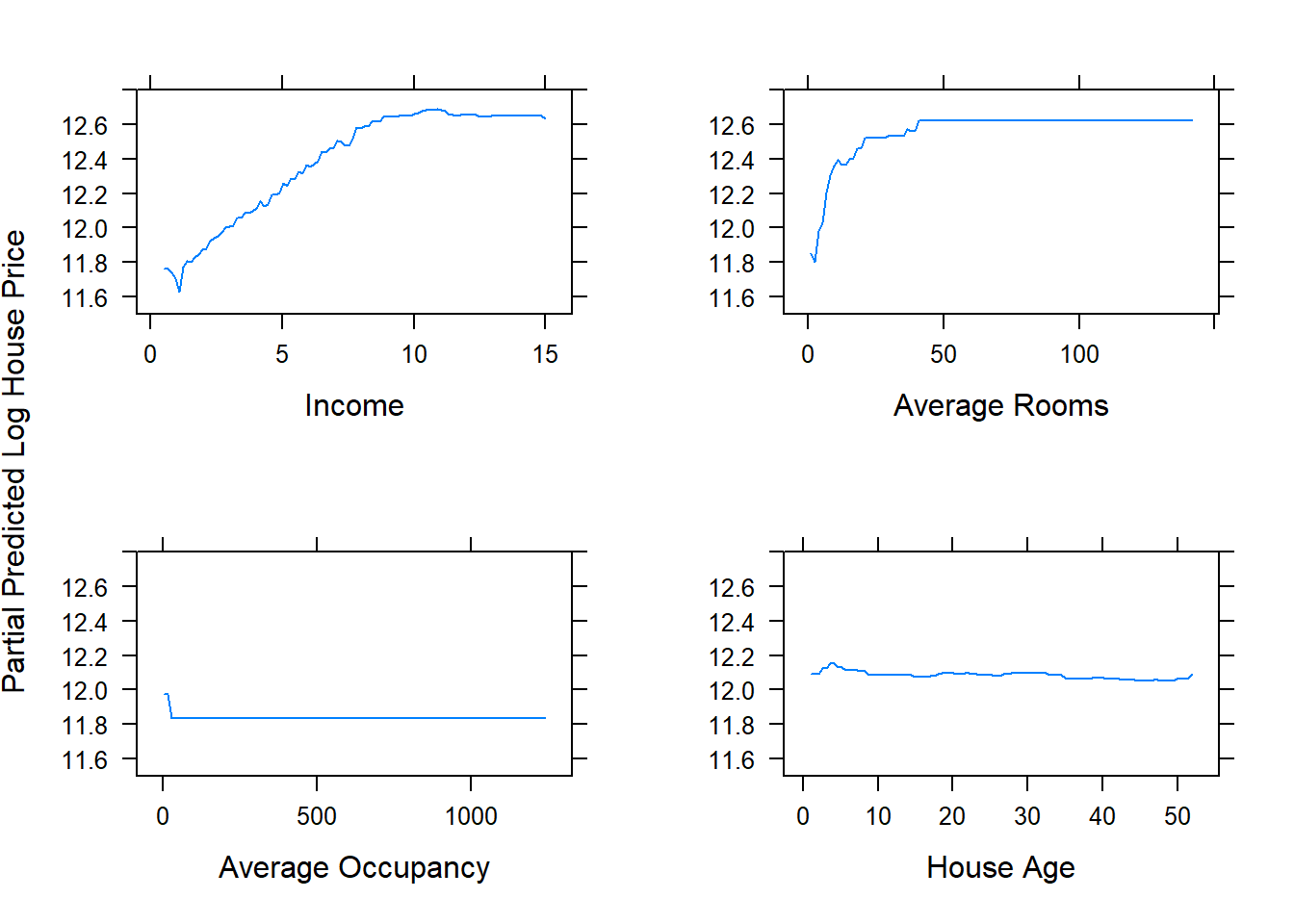

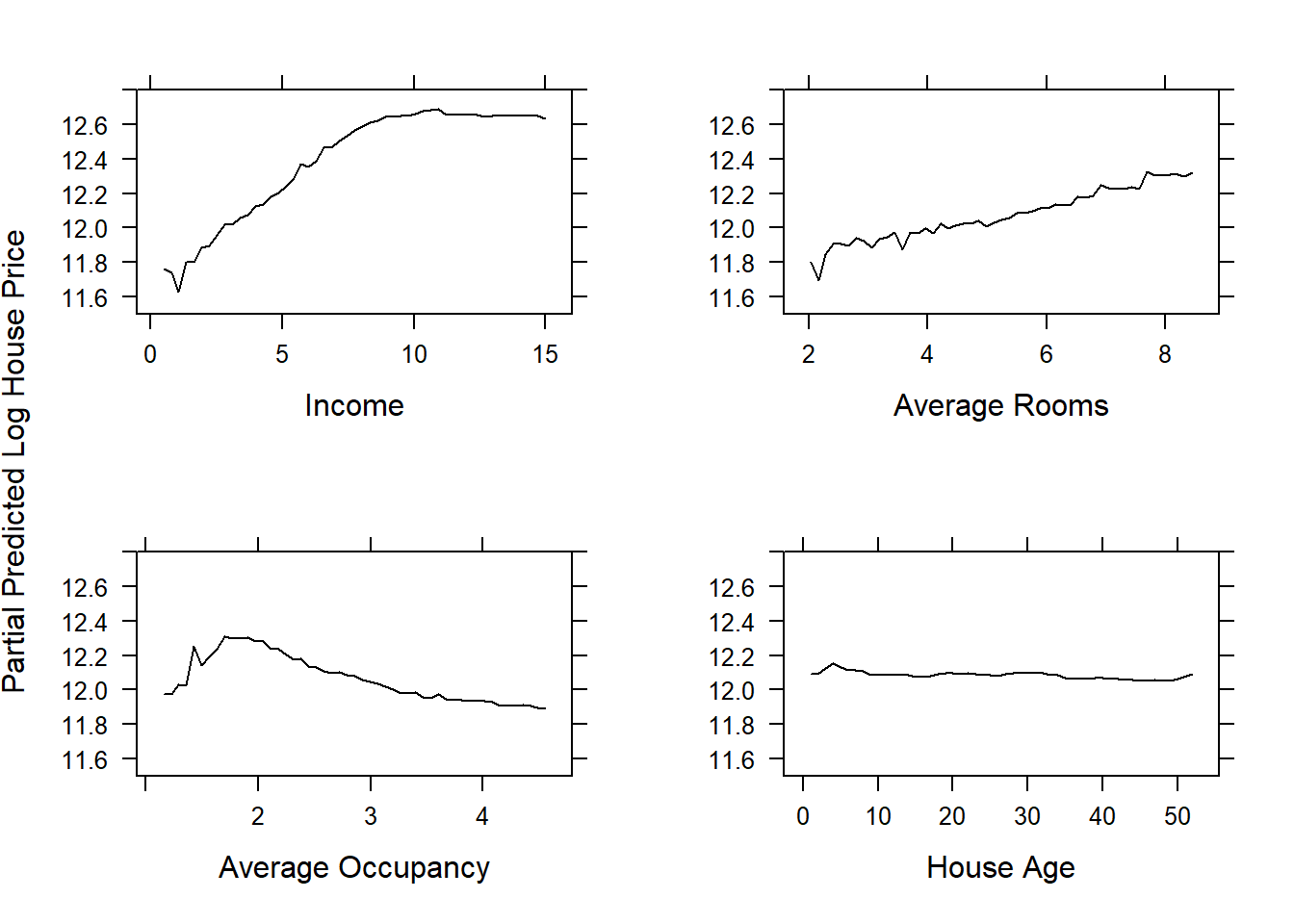

As expected, we see that median neighbourhood income yielded the greatest average reduction in RSS, during training followed by the location information. However, during permutation, removing only one of the location variables at a time did not have a major effect on prediction performance, presumably because much of the predictive power was still contained in the other location variable.

We can now apply the same procedure to the Titanic dataset.

6.3.6 Example 8 – Titanic (continued)

In practice one might want to jump straight to the hyperparameter tuning (after doing the necessary exploration and cleaning, of course). However, since we are still exploring and comparing these methods, we will again first see how the bagged model compares to the vanilla random forest, with a single pruned tree again added for reference. This step also helps to determine whether the number of trees is sufficient.

Since the Titanic dataset is much smaller than the California data, we will use a 70/30 split to be more certain of our out-of-sample performance.

# Train/test split

titanic <- na.omit(titanic)

set.seed(1)

train <- sample(1:nrow(titanic), 0.7*nrow(titanic))

# Bagging

titanic_bag <- randomForest(Survived ~ ., data = titanic, subset = train,

mtry = ncol(titanic) - 1,

ntree = 1000)

# Random Forest

titanic_rf <- randomForest(Survived ~ ., data = titanic, subset = train,

ntree = 1000)

# Quick single tree

stopcrit <- tree.control(nobs = length(train), mindev = 0.005)

titanic_tree_overfit <- tree(Survived ~ ., data = titanic, subset = train, control = stopcrit)

titanic_cv <- cv.tree(titanic_tree_overfit)

T <- titanic_cv$size[which.min(titanic_cv$dev)]

titanic_pruned <- prune.tree(titanic_tree_overfit, best = T)

# Predictions

titanic_bag_pred <- predict(titanic_bag, newdata = titanic[-train, ])

titanic_rf_pred <- predict(titanic_rf, newdata = titanic[-train, ])

titanic_tree_pred <- predict(titanic_pruned, newdata = titanic[-train, ], type = 'class')

# Prediction accuracy

y_titanic_test <- titanic[-train, 1]

titanic_bag_mis <- mean(y_titanic_test != titanic_bag_pred)

titanic_rf_mis <- mean(y_titanic_test != titanic_rf_pred)

titanic_tree_mis <- mean(y_titanic_test != titanic_tree_pred)

# Plot errors

plot(titanic_rf$err.rate[, 'OOB'], xlab = 'Number of trees', ylab = 'Classification error',

type = 's', col = 'darkgreen', ylim = c(0.1, titanic_tree_mis))

lines(titanic_bag$err.rate[, 'OOB'], col = 'blue', type = 's')

abline(h = titanic_bag_mis, col = 'blue', lty = 2, lwd = 2)

abline(h = titanic_rf_mis, col = 'darkgreen', lty = 2, lwd = 2)

abline(h = titanic_tree_mis, col = 'grey', lty = 2, lwd = 2)

legend('bottomright', legend = c('Bagging OOB', 'Bagging test', 'Random forest OOB', 'Random forest test', 'Single tree test'),

col = c('blue', 'blue', 'darkgreen', 'darkgreen', 'grey'), lwd = 2, lty = c('solid', 'dashed', 'solid', 'dashed', 'dashed'))

Figure 6.26: Testing errors for the bagged tree, random forest (default m), and single tree fitted to the Titanic dataset, added to the OOB error plots.

For this dataset – which is again considerably smaller than the California problem – we see that the OOB errors underestimated the testing errors. Although the default random forest was superior, we would again like to check all possible values of \(m\). We will also try two different splitting criteria: Gini index and Hellinger distance. See Aler et al. (2020) for information on the latter.

set.seed(2)

# Create combinations of hyperparameters

titanic_rf_grid <- expand.grid(mtry = 2:(ncol(titanic) - 1),

splitrule = c('gini', 'hellinger'),

min.node.size = c(1, 5, 10))

ctrl <- trainControl(method = 'oob', verboseIter = F)

# Use ranger to run all these models

titanic_rf_gridsearch <- train(Survived ~ .,

data = titanic,

subset = train,

method = 'ranger',

num.trees = 1000,

importance = 'permutation',

trControl = ctrl,

tuneGrid = titanic_rf_grid

)

plot(titanic_rf_gridsearch)

Figure 6.27: Hyperparameter combinations results for a random forest fitted to the Titanic dataset.

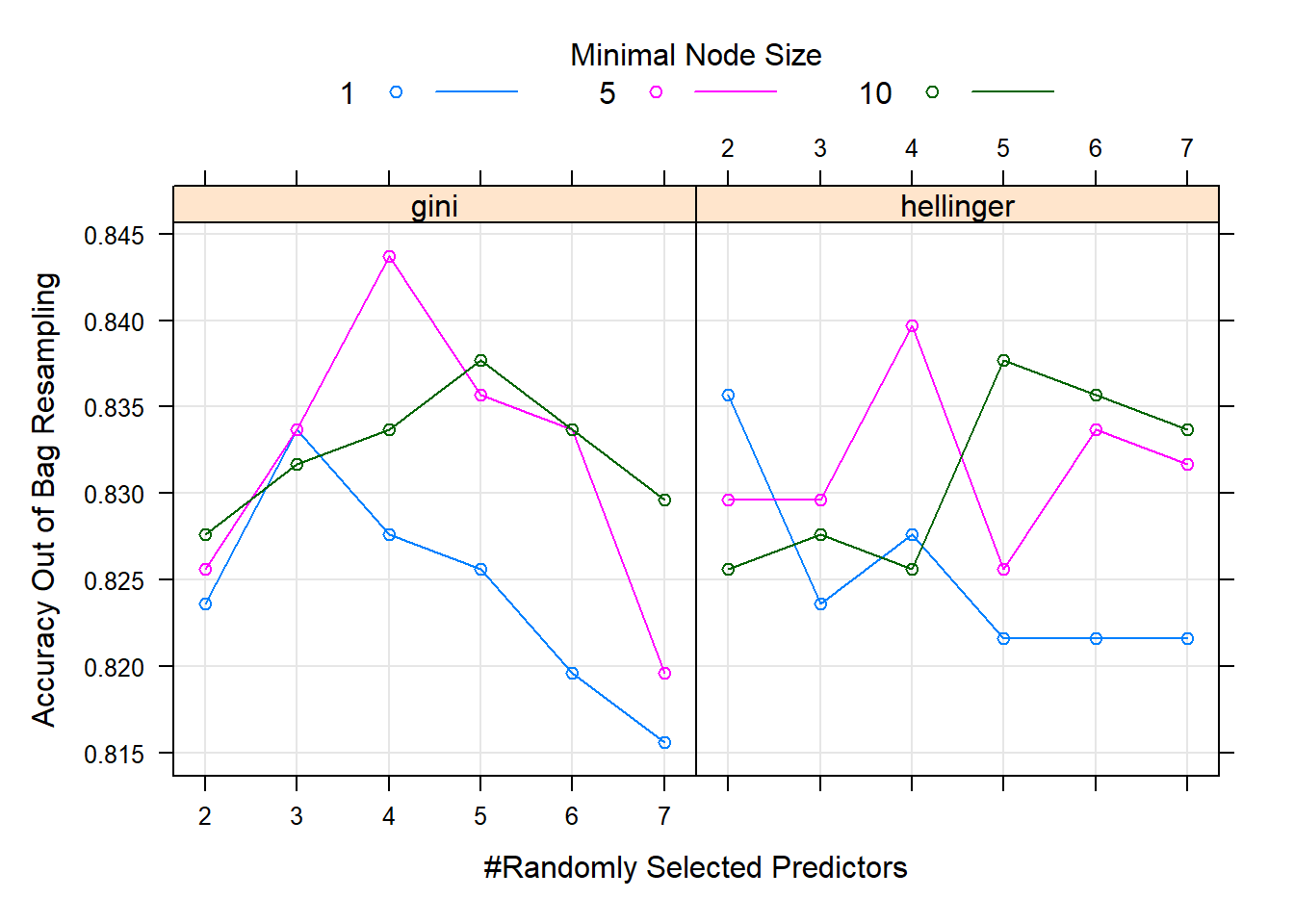

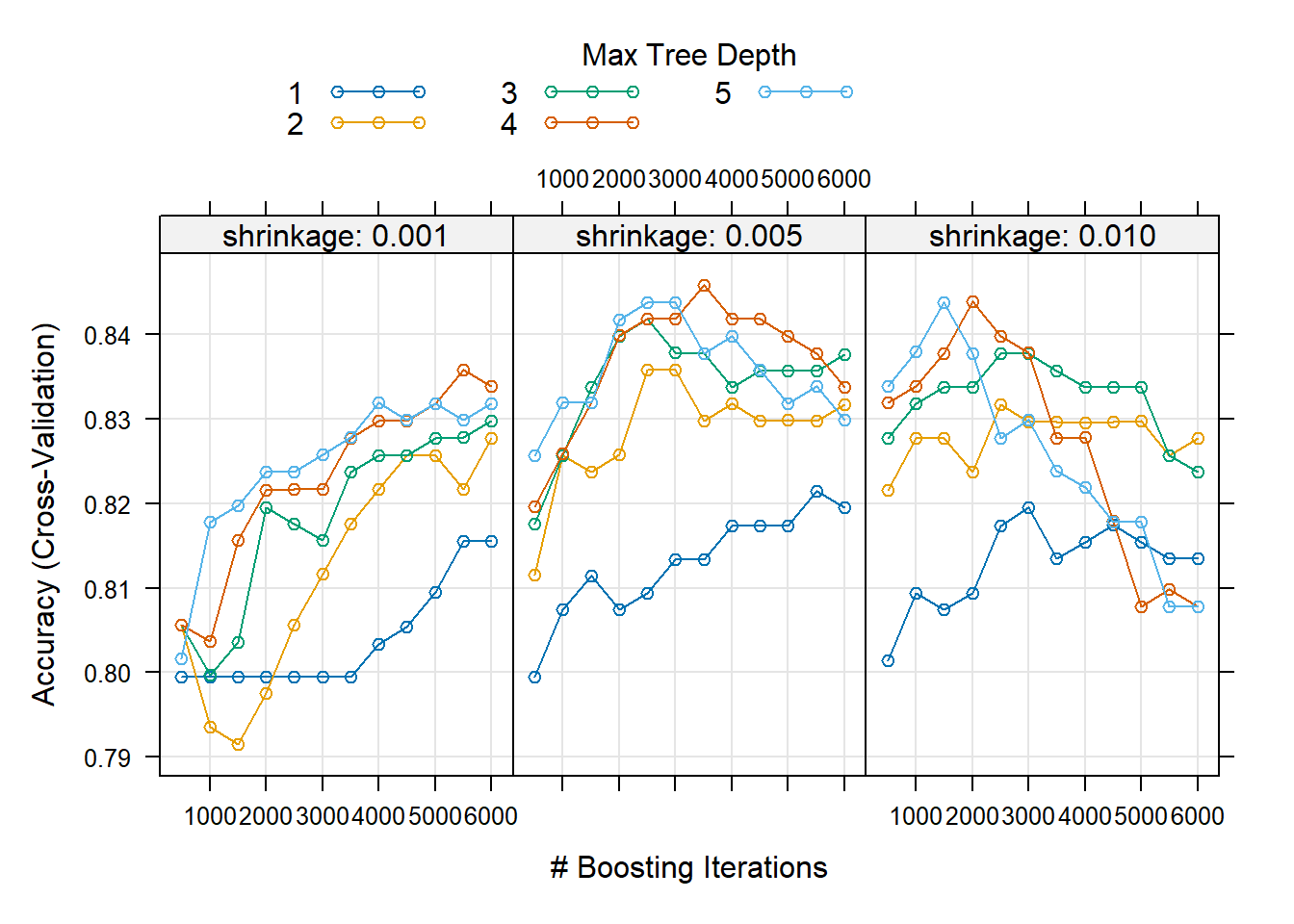

In Figure 6.27 we see that both splitting rules yield the highest accuracy when \(m=4\) and minimum node size is 5, with the Gini index split being superior at this combination. Note that these models fitted to a relatively small dataset like this one can be susceptible to sampling variation. As a homework exercise, rerun the above procedure multiple times and observe the change in results.

Next, we use the model that did best in OOB performance for prediction.

titanic_rfgrid_pred <- predict(titanic_rf_gridsearch, newdata = titanic[-train,])

titanic_rf_tuned_mis <- mean(y_titanic_test != titanic_rfgrid_pred)Tuning the random forest’s hyperparameters brought the misclassification rate down from 22.33% to 21.4%.

Finally, let’s consider the variable importance plots. This time we only stored the permutation-based variable importance, hence we can retrain the best model and keep track of the impurity importance, should we want to view that as well.

titanic_rf_besthp <- titanic_rf_gridsearch$bestTune

titanic_rf_impurity <- ranger(

Survived ~ .,

data = titanic[train, ],

num.trees = 1000,

mtry = titanic_rf_besthp$mtry,

min.node.size = titanic_rf_besthp$min.node.size,

splitrule = titanic_rf_besthp$splitrule,

importance = 'impurity',

seed = 123

)

trf_per_p <- vip(titanic_rf_gridsearch) +

labs(

title = 'Permutation Variable Importance',

x = 'Increase in Prediction Error',

y = NULL

) +

theme_minimal()

trf_imp_p <- vip(titanic_rf_impurity) +

labs(

title = 'Impurity Variable Importance',

x = 'Decrease in Splitting Criterion',

y = NULL

) +

theme_minimal()

trf_per_p + trf_imp_p

Figure 6.28: Variable importance plots for the tuned random forest fitted to the Titanic dataset.

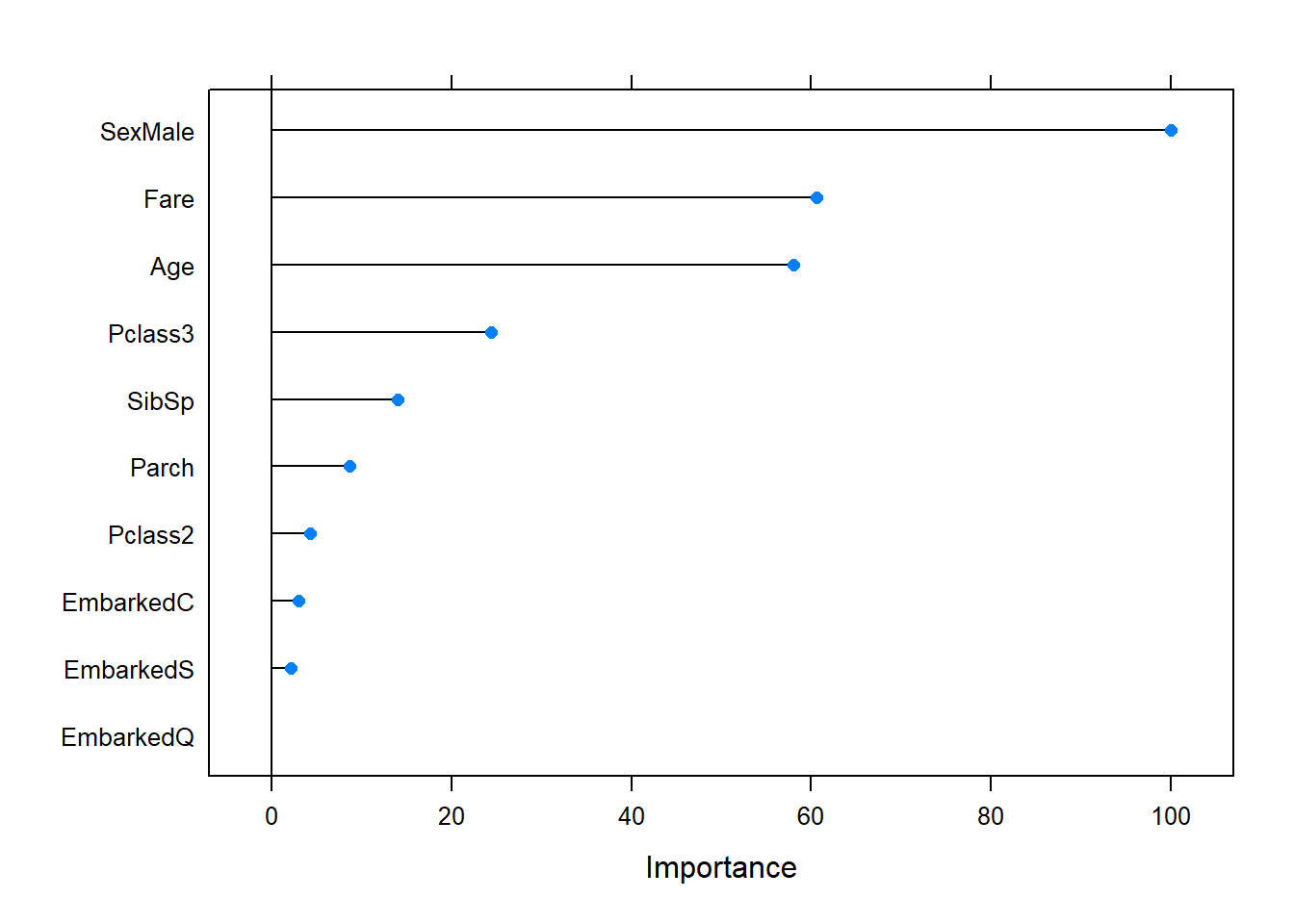

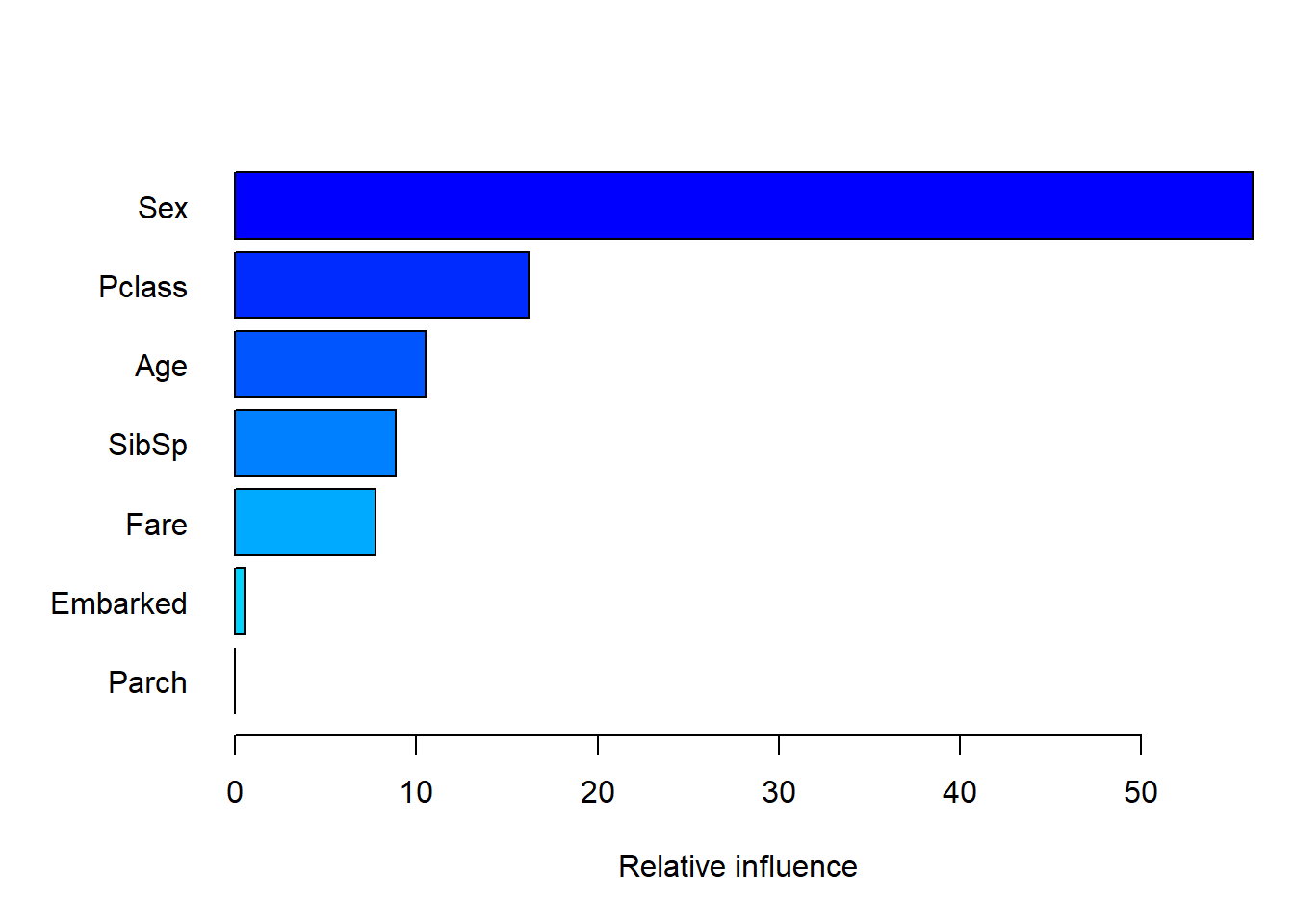

Passenger sex is the most important factor according to both importance measures. Although passenger age yielded the second largest average decrease in Gini index during training, it is noticeably less important in prediction, where performance is measured according to classification accuracy. Fare also features prominently. Whether or not they were 3rd class passengers also had a notable impact on prediction accuracy (refer back to Figure 6.10, where we used the entire dataset).

Although there are many modern extensions to random forests, those will be left for future exploration. Our final topic in this section is another, different form of tree ensembling, namely boosting.

6.4 Gradient boosting

Boosting describes a general purpose family of algorithms that ensemble many weak learners into strong learners by letting the base models sequentially learn from the mistakes made by the previous ones, in contrast to bagging which grow all trees independently. The weak learner can be any classification or regression algorithm, but it is most common to use a decision tree, specifically one with few splits.

There are several boosting variations, the more popular ones being AdaBoost and so-called stochastic gradient boosting (it has been shown that this boosting can be interpreted as a form of gradient descent in function space). Our application will entail the latter, which is a more generic and flexible algorithm. Boosting can be applied to both regression and classification trees – which we will do – although our exploration of the algorithm will focus only on the regression case.

The main idea of boosting is to let the algorithm gradually learn from its mistakes by starting with a base prediction, for example the mean of the target variable. A regression tree with a small number of splits \((d)\), is fitted to the residuals of this base prediction. The (scaled) residuals of this tree are then treated as the response variable used to grow the next tree with \(d\) splits. The (scaled) residuals of the new tree are then used to grow another tree with \(d\) splits, and so on…

This yields a sequence of \(B\) trees, each one accounting for some of the variation in \(y\) that was not explained by the previous trees, gradually bringing the residuals down to zero. Therefore, the model eventually overfits as the number of trees increases, and we make use of cross-validation (CV) to determine at which point this occurs.

The initial trees will capture the strongest patterns in the data and will contribute the most to RSS reduction, whilst subsequent trees will lead to smaller improvements. We limit the rate of learning firstly by using trees with few splits, and secondly via a shrinkage parameter \(\lambda\) that down-weights the contribution of each tree. In general, methods that learn slowly tend to perform well, although this slow learning approach requires many more trees than a random forest.

The steps are laid out in the following algorithm:

Algorithm 1 Gradient Tree Boosting (as implemented in R)

Let \(\hat{y}^{(b)}\) be the predictions after fitting \(b\) trees

Let \(\hat{r}^{(b)}\) be the predicted values (of the residuals) of tree \(b\)

Let \(r^{(b)}\) be the residuals after fitting \(b\) trees

Set \(\hat{y}^{(0)} = \bar{y}\) such that \(r^{(0)} = y - \bar{y}\)

For \(b = 1, \ldots, B\):

- Fit a regression tree with \(d\) splits to \((X, r^{(b-1)})\)

- Using the predictions \(\hat{r}^{(b)}\) of the current tree, update the predictions \[\hat{y}^{(b)} = \hat{y}^{(b-1)} + \lambda\hat{r}^{(b)}\]

- Updated the residuals using the current predictions \[r^{(b)} = r^{(b-1)} - \lambda \hat{r}^{(b)}\]

- Calculate the model’s final predictions \[ \hat{y} = y - r^{(B)} = \bar{y} + \lambda \sum_{b=1}^{B} \hat{r}^{(b)} \]

This algorithm works remarkably well on a variety of problems despite (perhaps because of) its simplicity. In the code below we initiate the algorithm from scratch and apply it to a dummy data set.

library(rpart)

set.seed(4026)

n <- 100

x1 <- round(runif(n, 0, 10), 0)

x2 <- round(runif(n, 0, 10), 0)

y <- round(10 + 3*x1 + x2 + rnorm(n, 0, 10))

dat <- data.frame(cbind(y, x1, x2))

# Initiate algorithm "by hand"

gb.manual <- function(lambda, d, ntrees){

train_mse <<- c() #To keep track of training error

resids <<- c() #To keep track of residuals

rhats <<- c() #To keep track of tree predictions

yhat_b <- mean(y) #First initialisation of prediction -> step 1

r_b <- y - yhat_b #First initialisation of residuals -> step 1

for(b in 1:ntrees){

ctrl <- rpart.control(maxdepth = 1, cp = 0.001)

t <- rpart(r_b ~ x1 + x2,

control = ctrl) #Fit tree to residuals -> step 2a

rhat_b <- predict(t, newdata = dat) #Predicted values of tree b -> step 2b

yhat_b <- yhat_b + lambda*rhat_b #Updated prediction -> step 2b

r_b <- y - yhat_b #Updated residuals -> step 2c

# r_b <- r_b - lambda*rhat_b #Could also write it like this, same thing

# Save all the training mses, residuals, and tree predictions

train_mse <<- c(train_mse, mean((y - yhat_b)^2)) #Double arrow saves object outside function

resids <<- cbind(resids, r_b)

rhats <<- cbind(rhats, rhat_b)

}

return(mean(y) + lambda*apply(rhats, 1, sum)) #Output final predictions -> step 3

# Could also return y - resids[, ntrees]

# Or just yhat_b

}

#Run algorithm

yhat_manual <- gb.manual(lambda = 0.01, d = 1, ntrees = 1000)

#Final model training error

(gbm_manual_train_mse <- mean((y - yhat_manual)^2)) # Or just train_mse[ntrees]## [1] 75.20785In order to validate this procedure, let us compare the results with those obtained from using the gbm package.

library(gbm) #No longer under development. Need to update to gbm3.

gbm_lib <- gbm(y ~ ., data = dat,

distribution = 'gaussian', #Applies squared error loss

n.trees = 1000,

interaction.depth = 1,

shrinkage = 0.01,

bag.fraction = 1) #Subsamples observations by default (0.5)

yhat_gbm <- gbm_lib$fit

(mse_gbm <- mean((y - yhat_gbm)^2))## [1] 75.20785We see that the training MSEs match exactly. As a final sanity check, let’s compare each tree’s training error between the manual implementation and the package’s.

## [1] TRUEIn the above algorithm description and example we see that there are three main hyperparameters that must be specified beforehand:

- The number of trees – \(B\)

Unlike bagging and random forests, boosting can lead to overfitting if \(B\) is too large. We use cross-validation to select \(B\).

- The shrinkage parameter or learning rate – \(\lambda\)

Typical values are 0.01 or 0.001 (the default in gbm). Smaller values require more trees.

- The maximum number of splits in each tree – \(d\)

Also called the interaction depth of the boosted model, since \(d\) splits can involve at most \(d\) variables. Depending on the size of the problem, \(d=1\) can work well when fitting many trees.

Although these are the main hyperparameters, one can also further control the tree depth (useful when larger trees are preferred), as well as introduce randomisation by randomly subsampling the training set, somewhat reminiscent of the bagging process.

To illustrate the application, let us return to the California housing example.

6.4.1 Example 6 – California housing (continued)

Since this is our final analysis of this dataset, we will apply some feature engineering, a process of adapting/transforming/combining the existing information into new features to improve model performance.

Instead of using the total number of bedrooms, bathrooms, and people per neighbourhood, let’s use the number of households to convert these into per-house rates. We will also apply a 70/30 train/test split, here showing how a caret function can be used to do so.

library(dplyr)

# Create calif feature engineered

calif_fe <- calif %>% mutate(AveRooms = Rooms/Households,

AveBedrms = Bedrooms/Households,

AveOccup = Population/Households) %>%

select(-Rooms, -Bedrooms, -Households)

# Using caret for train/test split:

set.seed(4026)

train_index <- createDataPartition(y = calif_fe$HousePrice, p = 0.8, list = FALSE)

calif_fe_train <- calif_fe[train_index,]

calif_fe_test <- calif_fe[-train_index,]As some benchmark for comparison – and to see whether the engineered features are useful – we will first fit a single regression tree.

# Slightly larger tree

calif_fe_tree <- tree(HousePrice ~ ., data = calif_fe_train,

control = tree.control(nobs=nrow(calif),

mindev = 0.003))

# Tune

set.seed(1)

calif_fe_cv <- cv.tree(calif_fe_tree)

calif_fe_cv$k[1] <- 0

plot(calif_fe_cv$size, calif_fe_cv$dev, type = 'o',

pch = 16, col = 'navy', lwd = 2,

xlab = 'Number of terminal nodes', ylab = 'CV RSS')

axis(side = 1, at = 1:max(calif_fe_cv$size), labels = 1:max(calif_fe_cv$size))

alpha <- round(calif_fe_cv$k)

axis(3, at = calif_fe_cv$size, lab = alpha)

mtext(expression(alpha), 3, line = 2.5, cex = 1.5)

Figure 6.29: Cross-validated pruning results from a tree fitted to the feature-engineered Cailfornia housing training set.

The CV RSS first reaches a minimum at 12 terminal nodes, hence we will prune it down to that size.

Figure 6.30: Pruning tree fitted to the feature-engineered Cailfornia housing training set.

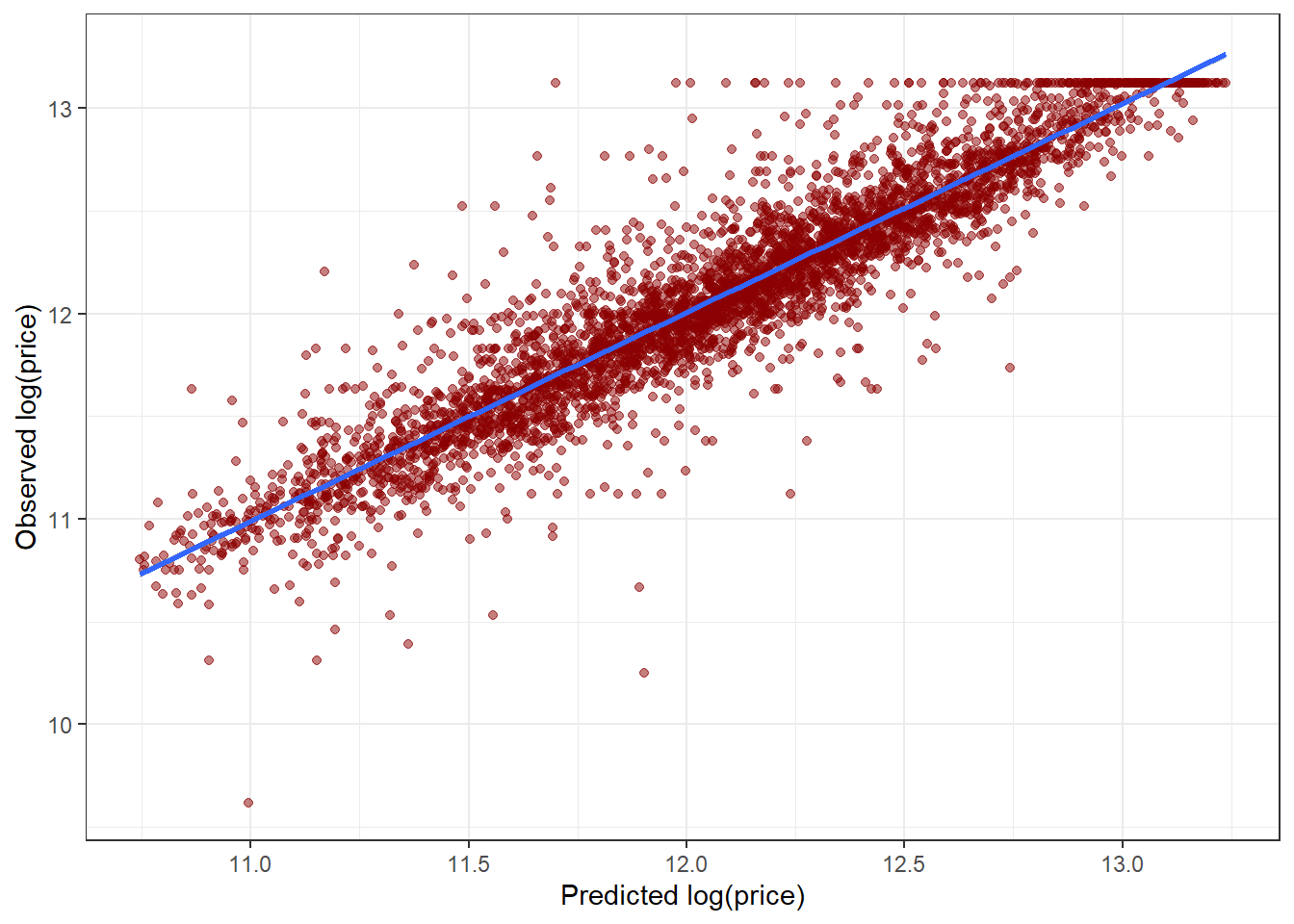

Here we see that the average number of rooms and average occupancy were indeed useful in this model (compare to Figure 6.7, which split almost exclusively on income and location). The CV RMSE is 0.387.

Next, we fit a gradient boosted trees model to the training set via the gbm package, using caret to apply hyperparameter tuning according to 10-fold CV (which can be parallelised). Note that for a problem of this size, the gbm model does take a while to run. Therefore, the code run below has been commented out after running, with the results saved and loaded back in for quick reproducibility.

# set.seed(4026)

# ctrl <- trainControl(method = 'cv', number = 10, verboseIter = T)

#

# calif_gbm_grid <- expand.grid(n.trees = c(1000, 10000, 50000),

# interaction.depth = c(1, 2, 5),

# shrinkage = c(0.01, 0.001),

# n.minobsinnode = 10)

#

# calif_gbm_gridsearch <- train(HousePrice ~ ., data = calif_fe_train,

# method = 'gbm',

# distribution = 'gaussian',

# trControl = ctrl,

# verbose = T,

# tuneGrid = calif_gbm_grid)

# save(calif_gbm_gridsearch, file = 'data/gbm_calif_50k.Rdata')

load('data/gbm_calif_50k.Rdata')Although we only touch on the subject here, the hyperparameter tuning procedure can be an entire topic on its own. One alternative to the grid search applied above – whereby all combinations of fixed sets of hyperparameter values are used – is to apply a random search, which introduces some variation in the hyperparameters. Bergstra & Bengio (2012) initially provided a strong argument for this approach within a neural network context. Further exploration of these topics is left for the reader.

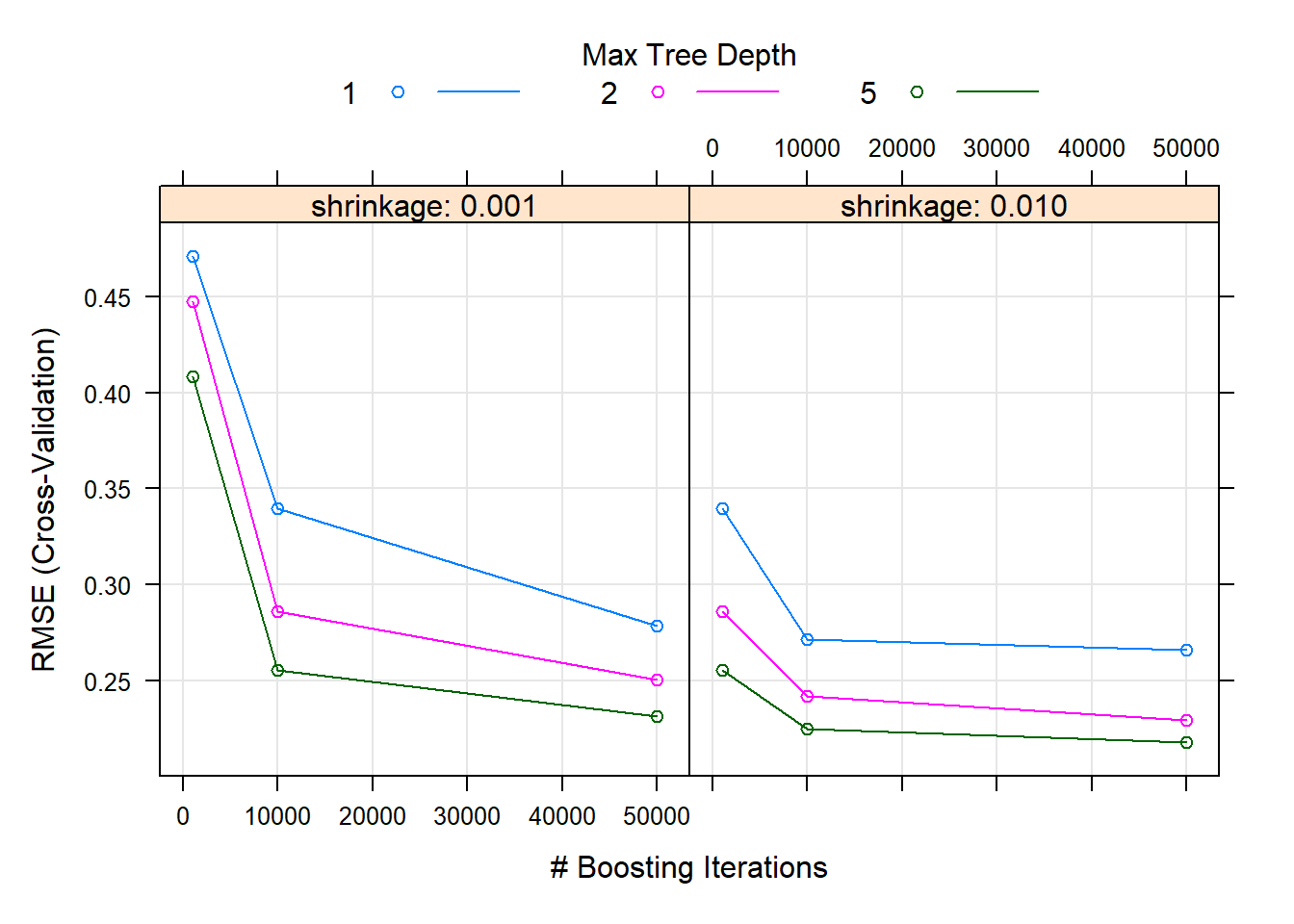

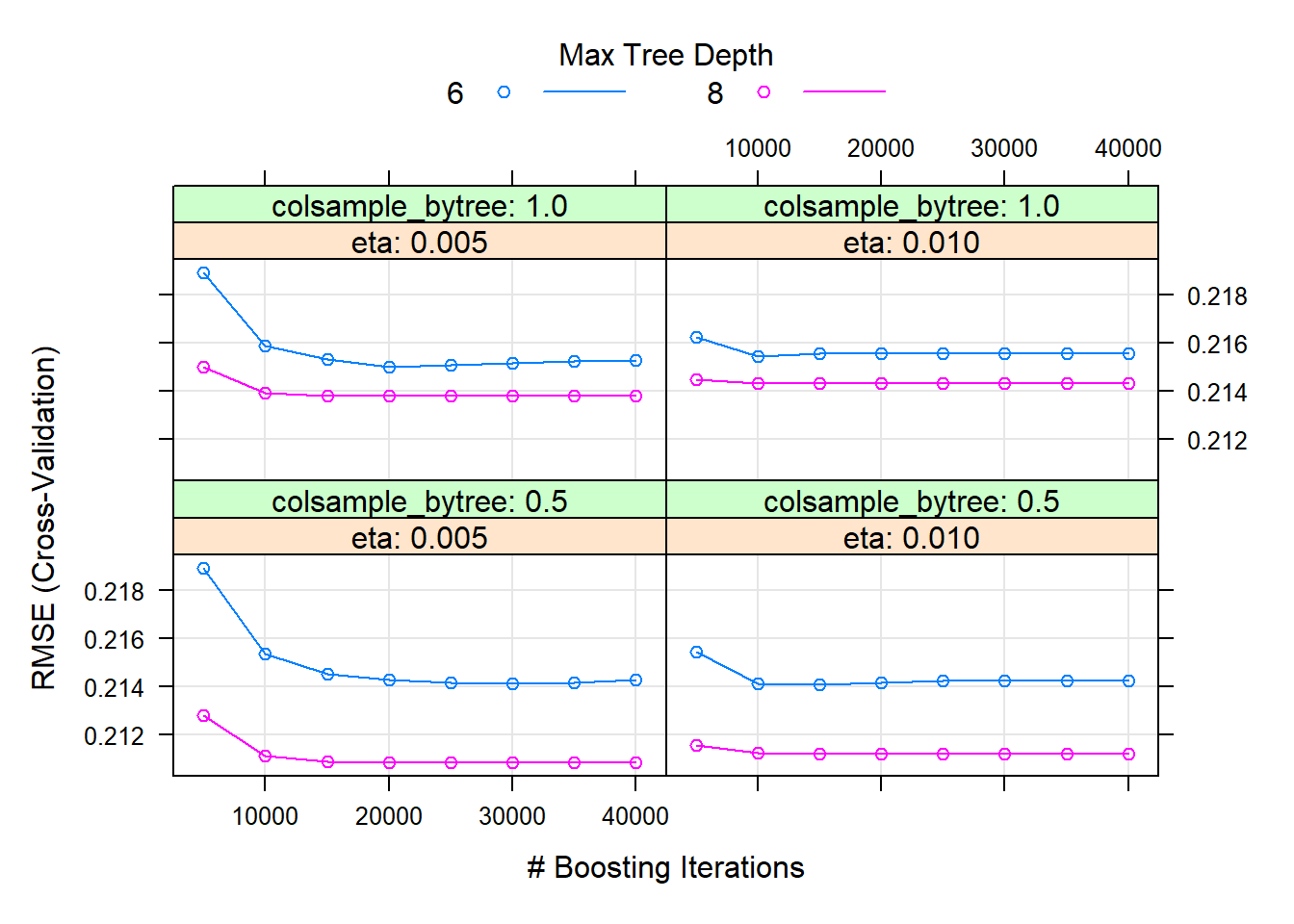

Looking at the CV results in Figure 6.31, we see that higher values of \(d\) in fact yielded better results. As expected, the higher learning rate reduced the CV error quicker for the same number of trees.

Figure 6.31: Hyperparameter combinations results for a gradient boosted trees model fitted to the feature-engineered California housing dataset.

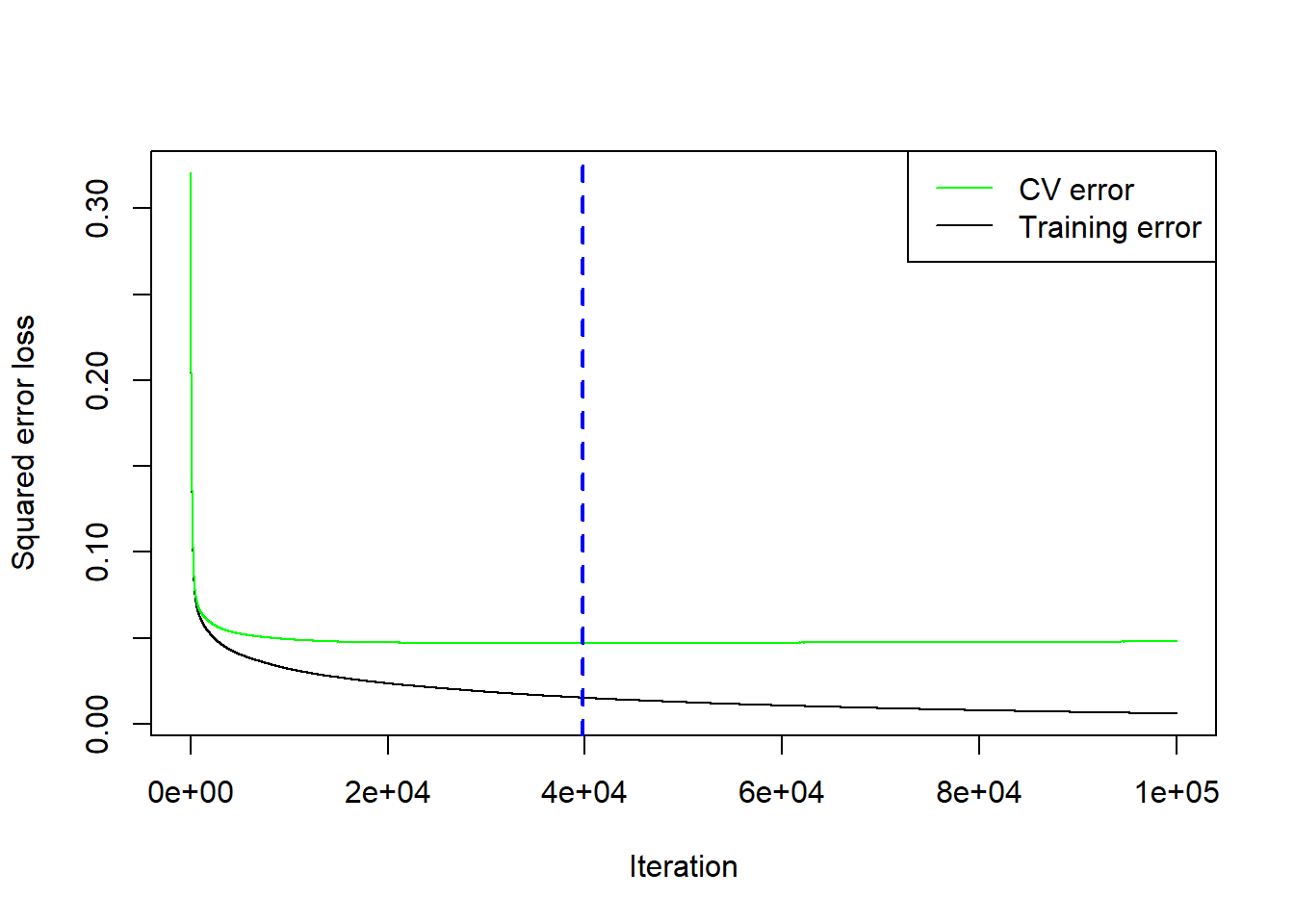

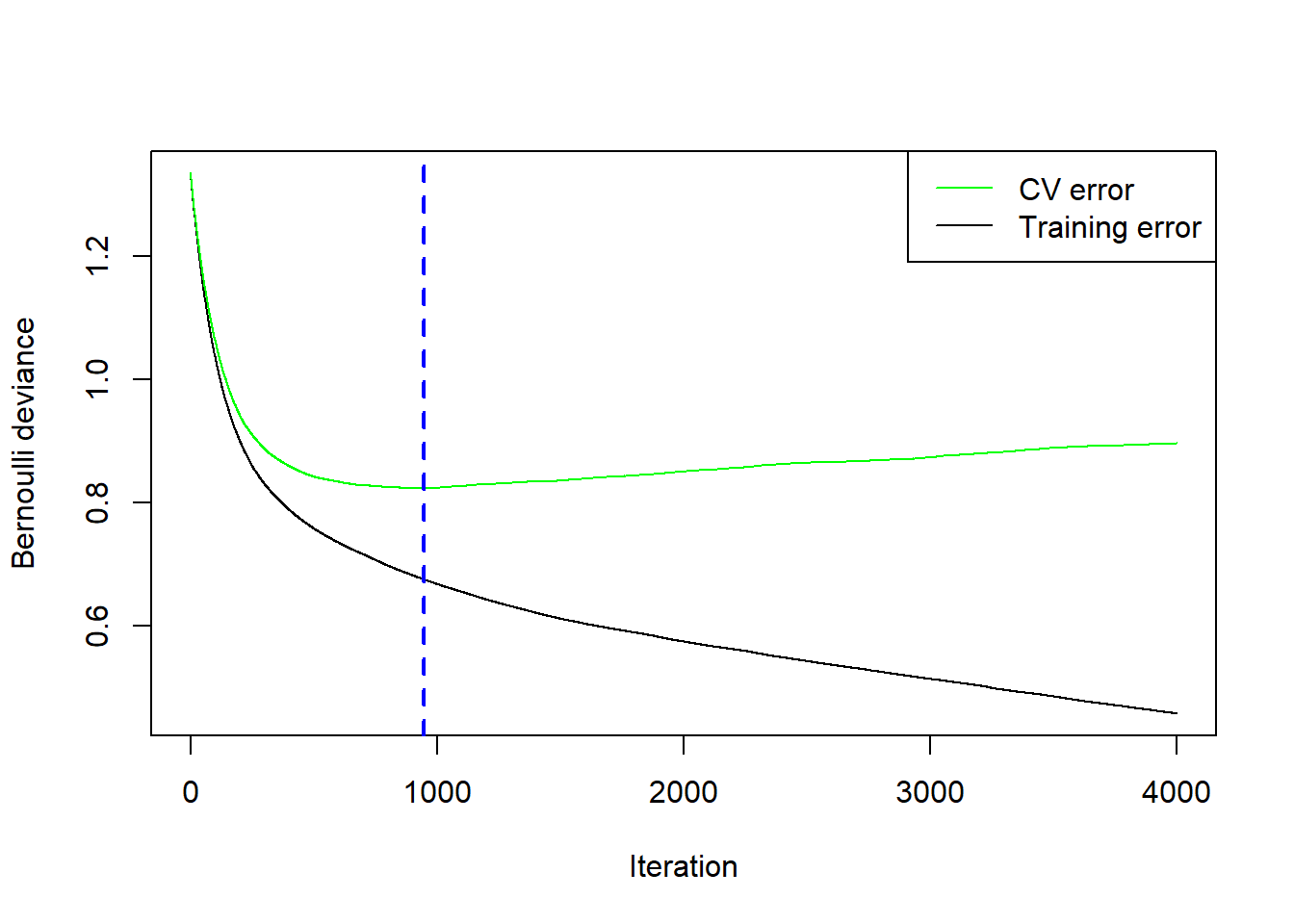

However, it is important to note that for this particular combination of number of trees it is difficult to determine whether the error is still decreasing at 50,000 trees. One approach, as we will see later, is to apply early stopping, where training stops once improvement has ceased according to some specified condition. To explore this model’s behaviour, let’s use a large number of trees together with the best combination of \(\lambda\) and \(d\) from the grid search and see where the CV error reaches a minimum (Figure 6.32).

# calif_fe_gbm <- gbm(HousePrice ~ ., data = calif_fe_train,